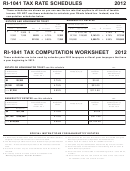

Form Ri-1041 - Rhode Island Fiduciary Income Tax Return - 2012 Page 6

ADVERTISEMENT

1

1 2

2 3

3 4

4 5

5 6

6 7

7 8

8 9

9 10

102012 RI-1041 FIDUCIARY INCOME TAX RETURN

GENERAL INSTRUCTIONS

WHO MUST FILE

SIGNATURE

NOTE: If no payment is required to be made

with the Rhode Island extension form and the fidu-

The fiduciary of a RESIDENT estate or trust must

The Rhode Island Fiduciary Income Tax Return

ciary is filing a federal extension form for the same

file a return on Form RI-1041 if the estate or trust:

must be signed. An unsigned return cannot be

period of time, the fiduciary does not need to

(1) is required to file a federal income tax return

processed. Any paid preparer who prepares a tax-

submit the Rhode Island form. Attach a copy of

for the taxable year or

payer's return must also sign as "preparer". If a firm

the Federal Form 7004 to the Rhode Island

(2) had any Rhode Island taxable income for the

or corporation prepares the return, it should be

Fiduciary Income Tax Return at the time it is submit-

taxable year.

signed in the name of the firm or corporation.

ted.

The fiduciary of a NONRESIDENT estate or trust

must file a return on Form RI-1041 if the estate or

WHOLE DOLLAR AMOUNTS

WHERE TO GET FORMS

trust had income or gain derived from Rhode Island

The money items may be shown as whole dollar

sources.

Additional forms and instructions may be obtained

amounts. Any amount under 50 cents may be elim-

from:

inated and any amount that is 50 cents or more

DEFINITIONS

The website:

must be increased to the next highest dollar.

The Division of Taxation: (401) 574-8970

A RESIDENT ESTATE is the estate of a dece-

dent who at his death was a resident individual in

ACCOUNTING PERIODS AND METHODS

INTEREST

this state.

The accounting period for which Form RI-1041 is

Any tax not paid when due, including failure to

A RESIDENT TRUST means, to the extent that

filed and the method of accounting used are the

pay adequate estimated tax, is subject to interest at

one or more beneficiaries are residents in Rhode

same as for federal income tax purposes. If the tax-

the rate of 18.00% (.1800).

Island:

able year or the method of accounting is changed

Interest on refunds of tax overpayments will be

(A) A trust created by will of a decedent who at

for federal income tax purposes, such change

paid if the refund is not paid within 90 days of the

his death was a resident individual in this state, or

applies similarly to the Rhode Island fiduciary

due date or the date the completed return was filed,

(B) A revocable trust which becomes irrevocable

return.

whichever is later. The interest rate for tax overpay-

upon the occurrence of any event (including death)

ments is 3.25% (.0325).

which terminates a person's power to revoke, but

REPORT OF CHANGE IN FEDERAL

only after the event, and only if the person having

TAXABLE INCOME

PENALTIES

the power to revoke was a Rhode Island resident

If the amount of the federal taxable income is

The law provides for penalties in the following

individual at the time of such event, or

changed or corrected by the Federal Government,

circumstances:

(C) An irrevocable trust created by or consisting

the fiduciary must report to the Rhode Island

•Failure to file an income tax return.

of property contributed by a person who is a resi-

Division of Taxation such change or correction with-

•Failure to pay any tax due on or before the

dent individual in this state at the time the trust was

in 90 days after the final determination of such

due date.

created or the property contributed (a) while such

change or correction.

Any fiduciary filing an

•Preparing or filing a fraudulent income tax

person is alive and a resident individual in this

amended federal income tax return must also file

return.

state, and (b) after such person's death if such per-

within 90 days thereafter an amended Rhode Island

son died a resident individual of this state.

return.

OTHER QUESTIONS

WHAT SCHEDULES TO COMPLETE

If you have any questions regarding completion

WHEN AND WHERE TO FILE

of your return, further assistance may be obtained

All estates and trusts must complete schedule I.

The due date is April 15, 2013 for returns filed for

by calling the Personal Income Tax Section at (401)

If the trust has a nonresident beneficiary, follow the

the calendar year 2012 and the 15th day of the

574-8829 and selecting option #3.

instructions for a nonresident estate or trust.

fourth month following the close of the taxable year

RESIDENT ESTATES AND TRUSTS: Complete

for returns filed for a year ending other than

PAYMENT BY CREDIT CARD

schedule I and enter 1.0000 on page 1, line 9. If the

December 31.

To Pay by Credit Card. You may use your

estate or trust is claiming credit for income taxes

American Express® Card, Discover® Card, Visa®

paid to another state, complete schedule I and

Mail your return to:

Card or MasterCard® card. To pay by credit card,

Schedule III. Enter 1.0000 on page 1, line 9.

Rhode Island Division of Taxation

call toll free or access by Internet the service

NONRESIDENT ESTATES AND TRUSTS: If all

One Capitol Hill

provider listed on this page and follow the instruc-

the income of the estate or trust is derived solely

Providence, RI 02908-5806

tions of the provider. A convenience fee will be

from Rhode Island sources, complete Schedule I

charged by the service provider based on the

and enter 1.0000 on page 1, line 9. If the estate or

EXTENSION OF TIME

amount you are paying. You will be told what the

trust has taxable income both within and without

Any extension of time granted for filing a Rhode

fee is during the transaction and you will have the

Rhode Island, complete Schedules I and II.

Island Fiduciary Income Tax Return shall not oper-

option to either continue or cancel the transaction.

ate to extend the time for the payment of any tax

You can also find out what the fee will be by calling

PERIODS TO BE COVERED

due on such return.

the provider’s toll-free automated customer service

The fiduciary taxable year for Form RI-1041 shall

In General -

number or visiting the provider’s Web Site shown

be the same as the federal taxable year.

(1) A fiduciary that is required to file a Rhode

below. If you paid by credit card, enter on page 1

Island Fiduciary Income Tax Return shall be

of Form RI-1041 in the upper left corner the confir-

PAYMENTS OR REFUNDS

allowed an automatic six month extension of time to

mation number you were given at the end of the

PAYMENTS: Any tax due must be paid in full with

file such return.

transaction and the amount of your tax payment

the return. Make check or money order payable to

(2) An application must be prepared in duplicate

(not including the convenience fee).

the Rhode Island Division of Taxation. An amount

on form RI-8736.

You may also use this method for making 2013

due of less than one dollar ($1) need not be paid.

(3) The original of the application must be filed

Rhode Island estimated income tax payments.

REFUNDS: If an overpayment of income tax is

on or before the date prescribed for the filing of the

shown on the return, a refund will be issued unless

return of the fiduciary with the Rhode Island

OFFICIAL PAYMENTS CORPORATION

indicated on the return that such overpayment is to

Division of Taxation.

Telephone payments:

be credited to the fiduciary's estimated tax liability

(4) Such application for extension must show

1-800-2PAY-TAX (1-800-272-9829)

for 2013. No other application for refund is neces-

the full amount properly estimated as tax for such

On line payments:

sary. Please note that no refund can be issued

fiduciary for such taxable year, and such application

unless the return is properly signed. Refunds of

must be accompanied by the full remittance of the

Customer Service:

less than $1.00 will not be paid unless specifically

amount properly estimated as tax which is unpaid

1-877-754-4413

requested.

as of the date prescribed for the filing of the return.

Page I-1

ADVERTISEMENT

0 votes

Related Articles

Related forms

Related Categories

Parent category: Financial