Form Fi-161 - Vermont Fiduciary Return Of Income - 2012 Page 7

ADVERTISEMENT

1

1 2

2 3

3 4

4 5

5 6

6 7

7 8

8return with the Internal Revenue Service if VT income is

Line 4b: Capital Gains Exclusion See Schedule FI-162 and

affected.

instructions to calculate the capital gains exclusion for 2012. Also,

see Technical Bulletin 60 on our website under “Publications”.

FORM FOR AMENDING VT FIDUCIARY TAX RETURN

Schedule FI-162 is not included here. It may be downloaded at

•

Check the Amended box in the upper right-hand corner on

in the “Forms” section, or mailed to you by

the applicable tax year(s) Form FI-161.

calling (802) 828-2515.

NET OPERATING LOSSES No VT refund is available for a

Line 4c: Adjustment for Bonus Depreciation on Prior Year

carryback. The VT carryback or carryforward election for a net

Property Enter the difference between the depreciation calculated

operating loss must be the same as elected for Federal purposes.

by standard MACRS methods and the depreciation calculated at

the Federal level. For information on calculating the amount that

LINE-BY-LINE INSTRUCTIONS

can be subtracted, see Technical Bulletin 44.

Line 1: Enter the taxable income amount from Federal Form

Line 5: Subtract Line 4d from Line 3.

1041, Line 22. For Qualified Settlement Funds, enter the amount

Line 6: Using Schedule B compute the tax on the VT taxable

from Federal Form 1120-SF.

income. Enter the tax from Line 23 or Line 25.

Line 2a: Enter the calculation of Non-VT State & Local

Line 7: Most taxpayers should enter 100% on this line. However,

Obligations from Schedule A, Line 18. For nonresident taxpayers,

a nonresident or part-year resident estate or trust should first

use Schedule E, Line 58 to adjust for Non-VT State and Local

complete Schedule E and then Schedule C to determine the income

Obligations.

adjustment.

Line 2b: Federal Bonus Depreciation VT does not recognize

the bonus depreciation allowed under Federal law for 2012. The

Line 9: Credit for Income Tax Paid to Other State or Canadian

Province (FOR FULL-YEAR AND SOME PART-YEAR

depreciation must be recalculated without the bonus depreciation

RESIDENT ESTATES & TRUSTS) Complete Schedule D and

using standard MACRS method. Enter the difference between

enter the amount here.

the depreciation calculated by standard MACRS methods and

the depreciation calculated using the Federal bonus depreciation

Line 11a: From 1099, Statements of VT Income Tax Withheld,

for assets placed in service in 2012. Go to

Estimated and/or Extension Payments. Enter the amount of VT

“Publications” to see Technical Bulletin 44 for information on

income tax withheld. Attach the copy of the 1099 or other payment

calculating the amount to add back to taxable income.

statement(s) to verify the amount. Estimated payments are not

required to be made for trusts and estates. However, if you chose

Line 2c: State and Local Income Taxes Enter the amount of

to make “estimated” payments, enter the amount paid and/or the

state and local income taxes above $5,000 which are included on

amount paid with the Extension of Time to File on this line as well.

Federal Form 1041, Line 11.

Line 11b: From Form RW-171, VT Real Estate Withholding.

Line 4a: Interest Income from U.S. Obligations

Interest

If VT real estate was sold during 2012 and the buyer withheld VT

income from U.S. government obligations (such as U.S. Treasury

Bonds, Bills, and Notes) is exempt from VT tax under the laws of

income tax from the sales price, enter the amount withheld shown

on Form RW-171, Vermont Withholding Tax Return for Transfer

the United States. Enter the amount of interest income from U.S.

of Real Property, Schedule A, Line 12 here.

Obligations on this line.

For installment sales, the balance of the gain must be reported

Interest income is exempt when received directly from the U.S.

to VT on future returns or elect to pay VT 6% tax on the entire

Treasury or from a trust, partnership, or mutual fund that invests

gain in the year of the sale. If you choose the 6% tax, include a

in direct obligations of the U.S. government.

letter with the return asking for the “6% Tax Elect Out for VT

Income from the sale of U.S. government obligations is taxable

Purposes” and attach a copy of the Federal Form 6252.

in VT. Income from repurchase agreements, securities of

FNMA, FHMC or GNMA or other investments that are not direct

Line 11c: From Form WH-435, Estimated Payment Made on

obligations of the U.S. government are also taxable. See Technical

Behalf of a Trust or Estate by a Business Entity for Nonresident

Partner, Member or Shareholder (NONRESIDENTS ONLY)

Bulletin 24 for more information.

Enter the estimated income tax payments made on behalf of the

Supporting Documentation Required No attachment to return

Trust or Estate by a partnership, limited liability company, or

required. However, obtain statements for the taxpayer’s records

S corporation toward the 2012 VT Fiduciary income tax. The

in the event the Department requests such documentation.

entity would have made these payments on Form WH-435. Call

Acceptable statements need to show the sources of U.S. government

(802) 828-5723 if more information is needed on Form WH-435

interest income and the percentage from each source. Summary

payments. See Technical Bulletins 5 & 6.

information from a K-1, or just a statement “U.S. government

securities” without further identification is not acceptable.

SCHEDULE A

NOTE: If U.S. interest is distributed on Line 18 of the Federal

INTEREST AND DIVIDEND INCOME FROM NON-VT STATE

1041, the deduction is lost.

AND LOCAL OBLIGATIONS ARE TAXABLE IN VT. A VT

obligation is one from the State of VT or VT municipality.

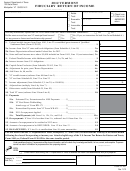

VT 2012 Tax Rate Schedule

Line 16: Enter the total interest and dividend income received

If Taxable

of the

from all state and local obligations exempted from Federal tax.

Income

But

the VT

amount

You may not reduce interest and dividend income by investment

is Over

Not Over

Tax is

over

expenses if those expenses are not used to reduce income on your

$0

$2,400

3.55%

$0

federal return.

$2,400

$5,600

$85.00 + 6.80%

$2,400

Line 17: Enter the interest and dividend income from VT

obligations. This may have been paid directly or through a

$5,600

$8,500

$303.00 + 7.80%

$5,600

mutual fund or other legal entity that invests in VT state and

$8,500

$11,650

$529.00 + 8.80%

$8,500

local obligations. If the income is received from a mutual fund

$11,650

---

$806.00 + 8.95%

$11,650

ADVERTISEMENT

0 votes

Related Articles

Related forms

Related Categories

Parent category: Financial