Estate Tax Form 2 - Ohio Estate Tax Return For All Resident Filings For Dates Of Death Page 13

Download a blank fillable Estate Tax Form 2 - Ohio Estate Tax Return For All Resident Filings For Dates Of Death in PDF format just by clicking the "DOWNLOAD PDF" button.

Open the file in any PDF-viewing software. Adobe Reader or any alternative for Windows or MacOS are required to access and complete fillable content.

Complete Estate Tax Form 2 - Ohio Estate Tax Return For All Resident Filings For Dates Of Death with your personal data - all interactive fields are highlighted in places where you should type, access drop-down lists or select multiple-choice options.

Some fillable PDF-files have the option of saving the completed form that contains your own data for later use or sending it out straight away.

ADVERTISEMENT

1

1 2

2 3

3 4

4 5

5 6

6 7

7 8

8 9

9 10

10 11

11 12

12 13

13 14

14 15

15 16

16 17

17 18

18 19

19 20

20 21

21 22

22 23

23Estate of:

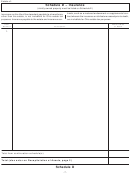

Schedule G – Transfers During Decedent’s Life

1. Transfers in Contemplation of Death (O.R.C. Section

3. Transfers with Reversionary Interest Retained (O.R.C.

5731.05). Any transfer in excess of $10,000 per year per

Section 5731.07). The value of the gross estate shall in-

donee made by the decedent within three years of death for

clude the value of any transfer of property or interest therein

less than adequate consideration is presumed to be in con-

made by the decedent for less than adequate consider-

templation of death and is includible in the Ohio gross es-

ation where (a) the possession or enjoyment can be ob-

tate, unless proof to the contrary can be provided. Interests

tained by the other person only by surviving the decedent

that do not qualify as present interests for the federal gift

and (b) the decedent retained a reversionary interest by

tax $10,000 exclusion will not qualify for the Ohio $10,000

express terms of the instrument which had a value as of

exclusion. Transfers made between spouses should not be

the date of death in excess of 5% of the value of property

included in the gross estate, but should be listed for infor-

transferred.

mational purposes only.

4. Transfers Subject to Change (O.R.C. Section 5731.08).

2. Transfers with Retained Enjoyment (O.R.C. Section

Any property or interest therein transferred by the dece-

5731.06). The value of the gross estate shall include the

dent without adequate consideration where the enjoyment

value of any property or interest herein that the decedent

on the date of death was subject to any change through the

transferred for less than adequate consideration and in which

exercise of a power by the decedent alone or in conjunc-

the decedent retained (a) the income or right to possession

tion with any person to alter, amend, revoke or terminate is

and enjoyment until the decedent’s death or (b) the right,

includible in the value of the gross estate.

either alone or in conjunction with any person, to designate

the person(s) who shall enjoy the property or income there-

from.

Item

Alternate

Alternate

Value at Date

Number

Description

Valuation Date

Value

of Death

1.

Total from continuation schedule(s)

Total (also enter on Recapitulation of Assets, page 2)

Schedule G

- 11 -

ADVERTISEMENT

0 votes

Related Articles

Related forms

Estate Tax Form 2 - Ohio Estate Tax Return For All Resident Filings For Dates Of Death On Or After January 1, 2002

Financial

Estate Tax Form 2 - Ohio Estate Tax Return For All Resident Filings For Dates Of Death On Or After January 1, 2002

Financial

Estate Tax Form 2 - Ohio Estate Tax Return For All Resident Filings For Dates Of Death Jan. 1, 2002 - Dec. 31, 2012

Financial

Estate Tax Form 2 - Ohio Estate Tax Return For All Resident Filings For Dates Of Death Jan. 1, 2002 - Dec. 31, 2012

Financial

Estate Tax Form 2 - Ohio Estate Tax Return For All Resident Filings For Dates Of Death On Or After January 1, 2002

Financial

Estate Tax Form 2 - Ohio Estate Tax Return For All Resident Filings For Dates Of Death On Or After January 1, 2002

Financial

Form Et 22 - Certificate Of Estate Tax Payment And Real Property Disclosure For Dates Of Death

Financial

Form Et 22 - Certificate Of Estate Tax Payment And Real Property Disclosure For Dates Of Death

Financial

Estate Tax Form 22 - Certificate Of Estate Tax Payment And Real Property Disclosure For Dates Of Death On Or After November 8, 1990

Financial

Estate Tax Form 22 - Certificate Of Estate Tax Payment And Real Property Disclosure For Dates Of Death On Or After November 8, 1990

Financial

") Form 22 - Certificate Of Estate Tax Payment And Real Property Disclosure For Dates Of Death On Or After November 8, 1990 (section 5731.21 O.r.c.)

Financial

Form 22 - Certificate Of Estate Tax Payment And Real Property Disclosure For Dates Of Death On Or After November 8, 1990 (section 5731.21 O.r.c.)

Financial

") Form Et 22 - Certifi Cate Of Estate Tax Payment And Real Property Disclosure For Dates Of Death On Or After Nov. 8, 1990 - Dec. 31, 2012 (section 5731.21 O.r.c.)

Financial

Form Et 22 - Certifi Cate Of Estate Tax Payment And Real Property Disclosure For Dates Of Death On Or After Nov. 8, 1990 - Dec. 31, 2012 (section 5731.21 O.r.c.)

Financial

Related Categories

Parent category: Financial