Form 43 - Nebraska Public Service Entity Tax Report Page 42

Download a blank fillable Form 43 - Nebraska Public Service Entity Tax Report in PDF format just by clicking the "DOWNLOAD PDF" button.

Open the file in any PDF-viewing software. Adobe Reader or any alternative for Windows or MacOS are required to access and complete fillable content.

Complete Form 43 - Nebraska Public Service Entity Tax Report with your personal data - all interactive fields are highlighted in places where you should type, access drop-down lists or select multiple-choice options.

Some fillable PDF-files have the option of saving the completed form that contains your own data for later use or sending it out straight away.

ADVERTISEMENT

1

1 2

2 3

3 4

4 5

5 6

6 7

7 8

8 9

9 10

10 11

11 12

12 13

13 14

14 15

15 16

16 17

17 18

18 19

19 20

20 21

21 22

22 23

23 24

24 25

25 26

26 27

27 28

28 29

29 30

30 31

31 32

32 33

33 34

34 35

35 36

36 37

37 38

38 39

39 40

40 41

41 42

42 43

43 44

44 45

45 46

46 47

47 48

48 49

49 50

50 51

51 52

52 53

53 54

54 55

55 56

56 57

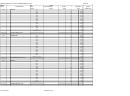

57FORM 43

NEBRASKA SCHEDULE 53 - DETAIL NET BOOK PERSONAL (CONT.)

INSTRUCTIONS:

The purpose of this schedule is to report the net book personal property of all tangible personal property. Detail must be reported by asset by year placed in service.

The suggested MACRS recovery period and depreciation are displayed on this schedule, a space has been provided if your company uses a different recovery period

or depreciation factor, report that information in the approriate columns.

Nebraska Schedule 53 must be filed in an Excel format. Nebraska Schedule 53's that are not completed in this format will not be accepted .

Late filing penalty of $100 per day up to $10,000 will be applied until the Department receives Nebraska Schedule 53 in correct format.

The original cost on this Schedule must conicide with the Nebraska Schedule 54 Percent Tangible Personal Property.

The original cost on this Schedule must conicide with the Nebraska Schedule 51 Detail Plant in Service.

TAXABLE PROPERTY all depreciable tangible personal property, except licensed motor vehicles, livestock, and certain rental equipment

which has a Nebraska net book value greater than zero is taxable. Summarize the property according to the categories indicated by accounts.

YEAR PLACED IN SERVICE is the year the property was acquired.

TOTAL ORIGINAL COST/NEBRASKA ADJUSTED BASIS is the adjusted basis for federal income tax purposes increased by the amount of

the depreciation, amortization, or deduction under section 179, taken on the personal property. Generally, this will be the cost of the item.

RECOVERY PERIOD is the period over which the value of property will be depreciated for Nebraska property tax purposes. The recovery period

is the same as the federal Modified Accelerated Cost Recovery System (MACRS). Reference IRS Publication 534 MACRS table of assets and associated recovery

period in years.

DEPRECIATION FACTOR is the percentage of the Nebraska adjusted basis that is taxable.

NET BOOK TAXABLE VALUE is the taxable value for property tax purposes. It is calculated by multiplying the

total original cost/Nebraska Adjusted Basis by the depreciation factor for the recovery period and year acquired.

96-187-99 Revised 3/2013

Authorized by Section 77-801

ADVERTISEMENT

0 votes

Related Articles

Related forms

Related Categories

Parent category: Financial