Instructions For Form M2 - Minnesota Income Tax For Estates And Trusts (Fiduciary) - 2017 Page 10

ADVERTISEMENT

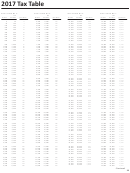

- 2017 Printable pdf") 1

1 2

2 3

3 4

4 5

5 6

6 7

7 8

8 9

9 10

10 11

11 12

12 13

13 14

14Federal Adjustments for Businesses

Minnesota defines net income for fiduciary

specialized small business investment

Tax Cuts and Jobs Act (Pub. L. 115-97)

income tax according to the Internal Revenue

companies.

• Section 13201 – Increase in federal bonus

Code, as amended through December 16,

• Section 13314 – Certain self-created

depreciation for certain assets. If you

2016. Since that date, federal tax laws

property not treated as a capital asset under

claimed federal bonus depreciation on line

have been enacted that contain a number of

IRC 1221.

14 or 25 of federal Form 4562 for assets

provisions affecting the amount of income for

placed in service after September 27,

• Section 13402 – Rehabilitation credit

tax year 2017. Because Minnesota has not yet

2017, you may need to make an income

limited to certified historic structures.

adopted these federal changes, adjustments

adjustment on your Minnesota return.

• Section 13501 – Treatment of gain or loss

must be made to correctly determine your

• If you claimed federal bonus depreciation

of foreign persons from sale or exchange of

Minnesota tax when filing your 2017 Form

in excess of 50% of your basis in the

interests in partnerships engaged in trade or

M2, Income Tax Return for Estates and Trusts.

asset, add the amount of federal bonus

business within the United States.

How to Report the Federal

depreciation you claimed that exceeds 50%

• Section 13502 – Modification to definition

Adjustments

of your basis in the asset.

of substantial built-in loss in the case of

• If you claimed bonus depreciation on used

transfer of partnership interest.

If any of the federal provisions that are

property, or on qualified film, television or

included in federal Disaster Tax Relief and

• Section 13521 – Clarification of tax basis of

live theatrical productions, add the federal

Airport and Airway Extension Act of 2017

life insurance contracts under IRC 1016.

bonus depreciation you claimed for these

(Pub. L. 115-63), and Tax Cuts and Jobs Act

• Section 13522 – Exception to transfer for

items.

(Pub. L. 115-97) affect the amount of taxable

valuable consideration rules under IRC 101.

• Determine the amount of depreciation

income reported on your 2017 federal Form

• Section 13532 – Repeal of advance

you would have been allowed had you

1041, U.S. Income Tax Return for Estates

refunding bonds.

not claimed the excess bonus depreciation

and Trusts, you must make an adjustment

• Section 13543 – Modification of treatment

described in this section. Use the

to income on your 2017 Minnesota form.

of S corporation conversions to C

appropriate recovery period and method

To determine the amount of the adjustment,

corporations.

for each asset under the Internal Revenue

recompute your federal taxable income

Code as amended through December 16,

• Section 13801 – Production period for beer,

without regard to provisions included in

2016. Subtract the amount of depreciation

wine, and distilled spirits.

those Acts and report the difference as an

you calculate for the assets.

adjustment to income.

• Section 13821 – Modification of tax

• Section 13202 - Modification to depreciation

treatment of Alaska Native Corporations

To report the differences for Minnesota tax

limitations on luxury automobiles and

and settlement trusts.

purposes, you must do all of the following:

personal use property.

• Section 13823 – Designation of Opportunity

• attach a schedule to your Form M2 that lists

• Section 13203 - Modification of treatment of

Zones and special rules for capital gains

the federal provisions affecting your taxable

certain farm property.

invested.

income by the act title and section number

• Section 13204 - Changes in applicable

• Section 14101 – Deduction for foreign-

• show how you calculated each adjustment

recovery period for real property.

source portion of dividends received by

amount

domestic corporations from specified

• include the net of all adjustments on your

• Section 13207 – Expensing of certain costs

10-percent owned foreign corporation.

Form M2, line 31, if the net amount is a

of replanting citrus plants lost by reason of

positive number, and on Form M2, line

casualty under IRC 263A.

• Section 14102 – Special rules relating

38, if the net amount is a negative number.

to sales or transfers involving specified

• Section 13303 – Like-kind exchange

Enter code 11 in the box that corresponds

10-percent owned foreign corporations.

treatment limited to real property under IRC

with the line used for the adjustment

• Section 14103 – Mandatory inclusion of

1031.

Provisions that may require

deferred foreign income under IRC 965.

• Section 13304 – Limitation on deduction by

an income adjustment

• Section 14201 – Current year inclusion of

employers of expenses for fringe benefits

global intangible low-taxed income (GILTI)

under IRC 274.

The following provisions may require

by United States shareholders.

• Section 13307 – Denial of deduction

an income adjustment for Minnesota

• Section 14211 – Elimination of inclusion of

for settlements subject to nondisclosure

tax purposes. This list includes the most

foreign base company oil related income.

agreements paid in connection with sexual

commonly used adjustments; you must make

harassment or sexual abuse.

adjustments as needed for all provisions

• Section 14212 – Repeal of inclusion based

included in the listed Acts:

on withdrawal of previously excluded

• Section 13308 – Repeal of deduction for

subpart F income from qualified investment.

local lobbying expenses.

Disaster Tax Relief and Airport and

• Section 14213 – Modification of stock

Airway Extension Act of 2017 (Pub. L.

• Section 13310 – Prohibition on cash, gift

attribution rules for determining status as a

cards, and other nontangible personal

115-63)

controlled foreign corporation.

property as employee achievement awards.

Section 504(a) – Suspended limitations

• Section 14214 – Modification of definition

under IRC 170(b) on charitable contributions

• Section 13312 – Certain contributions

of United States shareholder.

associated with qualified hurricane relief made

by governmental entities not treated as

during the period beginning on August 23,

contributions to capital.

• Section 14215 – Elimination of requirement

2017, and ending on December 31, 2017.

that corporation must be controlled for 30

• Section 13313 – Repeal of rollover of

days before subpart F inclusions apply.

of publicly traded securities gain into

10

ADVERTISEMENT

0 votes

Related Articles

Related forms

- 2016")

- 2015")

- 2014")

- Net Investment Income Tax -individuals, Estates, And Trusts - (2015)")

Related Categories

Parent category: Financial