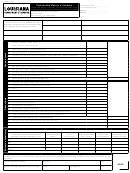

Form It-565 - Partnership Return Of Income With Instructions And Form It-565b Apportionment Of Income Schedule Page 2

ADVERTISEMENT

1

1 2

2 3

3 4

4 5

5 6

6 7

7 8

8 9

9 10

10 11

11Page 1

IT-565i (1/14)

Louisiana Department of Revenue

Instructions for Completing Form IT-565

P. O. Box 3440

Partnership Return of Income

Baton Rouge, LA 70821-3440

Partnerships not required to file a return

accounting period established on the first return must remain as the

A partnership return is not required if all partners are natural persons

accounting period for subsequent years under Louisiana Income Tax

who are residents of Louisiana (R.S. 47:201).

Law, unless permission to make a change is received from the Secretary

of Revenue.

Partnerships that must file a return

A change by any partnership from one taxable year to another, or

Any partnership doing business in Louisiana or deriving any income

the adoption by a new partnership for an initial taxable year, must

from sources therein, regardless of the amount and regardless of the

meet the provisions of R.S. 47:206(B)(1). A change by a principal

residence of the partners, must file a Partnership Return of Income,

partner from one taxable year to another must meet the provisions of

Form IT-565 if any partner is a nonresident of Louisiana or if any

R.S. 47:206(B)(2). A principal partner is one who has an interest of five

partner is not a natural person. If the partnership has income that is

percent or more in the partnership profits or capital.

derived from sources partly within and partly outside of Louisiana,

an Apportionment of Income Schedule, Form IT-565B must be filed

Accrued or received income

with Form IT-565. Louisiana Revised Statute (R.S.) 47:220.3 defines

If records are kept on an accrual basis, report all income accrued, even

the term “partnership” to include syndicates, groups, pools, joint ven-

though it has not been actually received or entered in the records, and

tures, or other unincorporated organizations, through or by means of

report all expenses incurred, not just expenses paid. If records do not

which any business, financial operation, or venture is carried on, and

show income accrued and expenses incurred, report all income received

that are not trusts, estates, or corporations within the meaning of the

or constructively received, such as bank interest credited to your account

Louisiana Income Tax Law.

and expenses paid.

Income tax returns of partners

Penalties

Each partner that is a natural person must include on his individual in-

The penalty for willfully making a false or fraudulent return or for

come tax return the amount of the distributive share of the net income of

willful failure to make and file the return on time shall not be more

the partnership, whether or not such share was distributed or withdrawn

than $1,000, or imprisonment for not more than one year, or both,

by the partner. This distributive share of the partnership’s net income

and shall include the costs of prosecution.

or losses must be reported to conform to the partnership’s accounting

period, regardless of a fiscal year or calendar year taxable period. If the

Income items exempt from tax

partnership’s tax year does not coincide with the partners’ tax year, in-

The following are some types of income that are exempt from Louisiana

clude the income or losses in the tax year in which the partnership’s tax

income tax and should not be included in gross income:

year ended. The Louisiana resident return, Form IT-540 must be used

(a) Amounts received under a life insurance contract paid by reason

to report partnership income for resident individuals.

of the death of the insured and paid at the death of the insured.

A nonresident member of a partnership who does not have a valid agree-

For treatment of amounts paid at a date later than death, R.S.

ment on file with LDR must be included in a Composite Partnership

47:43(D).

Return (Form R-6922). Nonresident partners who have a valid agree-

(b) That portion of an annuity that represents a return of the taxpay-

ment or who have other income derived from Louisiana sources, must

er’s investment, R.S. 47:44.

include all income derived from Louisiana sources on Form IT-540B.

Individuals should use the information reported on the federal

(c) Gifts (not received as a consideration for services rendered) and

partnership return instead of the amounts shown in the partners’

money and property acquired by bequest, devise, or inheritance.

allocation schedule. Corporations should refer to Louisiana Revised

However, the income derived from such property is taxable.

Statute (R.S.)-47:287.93(A)(5).

(d) Interest on obligations of the United States Government and/or

its instrumentalities.

When and where the return must be filed

Returns for a calendar year must be filed with the Department of

(e) Interest on obligations of the State of Louisiana and its political

Revenue, P O Box 3440, Baton Rouge, LA 70821-3440, on or before

or municipal subdivisions to the extent as is now exempt by law.

May 15 of the year following the close of the calendar year. Returns for

fiscal years must be filed on or before the 15th day of the fifth month

List in Schedule K all items of income reported on your Federal return

after the close of the fiscal period.

that are exempt from Louisiana tax.

Period to be covered by return

Information at the source

The return must be filed for a calendar year, or for a fiscal year of 12

Any person, firm, partnership, trust, corporation, or organization

months, ending on the last day of any month other than December,

making payments totaling $1,000 or more during any calendar year for

or for an annual period of 52/53 weeks if records are kept on that

lease bonuses, delay rentals, and/or royalties respecting mineral leases

basis. For fiscal years or annual periods of 52/53 week filings, clearly

affecting lands located in Louisiana and rentals paid for real property

indicate the beginning and ending dates at the top of the return. The

located in Louisiana to a nonresident individual or a firm, partnership,

ADVERTISEMENT

0 votes

Related Articles

Related forms

Related Categories

Parent category: Financial