Publication 947 - Practice Before The Irs And Power Of Attorney Page 10

ADVERTISEMENT

1

1 2

2 3

3 4

4 5

5 6

6 7

7 8

8 9

9 10

10 11

11 12

12 13

13 14

14 15

15 16

16 17

17 18

18 19

19A power of attorney held by a student will be recorded

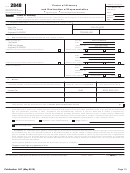

Mr. Smith’s CAF number, his telephone number, and his

on the CAF system for 130 days from the receipt date. If

fax number. Mr. Smith’s address, telephone number, and

you are authorizing a student to represent you after that

fax number have not changed since the IRS issued his

time, you will need to submit a current and valid Form

CAF number, so Stan and Mary do not check the boxes in

2848.

the second column.

Line 3—Tax Matters. On their separate Forms 2848,

When Is a Power of Attorney Not

Stan and Mary each enters “income” for the type of tax,

Required?

“1040” for the form number, and “2009, 2010, and 2011”

for the tax years.

A power of attorney is not required when the third party is

not dealing with the IRS as your representative. The follow-

Line 4—Specific use not recorded on Centralized Au-

ing situations do not require a power of attorney.

thorization File (CAF). On their separate Forms 2848,

Stan and Mary make no entry on this line because they do

•

Providing information to the IRS.

not want to restrict the use of their powers of attorney to a

•

Authorizing the disclosure of tax return information

specific use that is not recorded on the CAF. See Prepara-

through Form 8821, Tax Information Authorization,

tion of Form — Helpful Hints, earlier.

or other written or oral disclosure consent.

Line 5—Acts authorized. Mary wants to sign any agree-

•

Allowing the IRS to discuss return information with a

ment that reflects changes to her and Stan’s joint 2009,

third party via the checkbox provided on a tax return

2010, and 2011 income tax liability, so she writes “Tax-

or other document.

payer must sign any agreement form” on line 5 of her Form

•

2848. Stan does not wish to restrict the authority of Jim

Allowing a tax matters partner or person (TMP) to

Smith in this regard, so he leaves line 5 of his Form 2848

perform acts for the partnership.

blank. If either Mary or Stan had chosen, they could have

•

Allowing the IRS to discuss return information with a

listed other restrictions on line 5 of their separate Forms

fiduciary.

2848.

Line 6—Retention/revocation of prior power(s) of at-

How Do I Fill Out Form 2848?

torney. Stan and Mary are each filing their first powers of

attorney, so they make no entry on this line. However, if

they had filed prior powers of attorney, the filing of this

The following example illustrates how to complete Form

current power would revoke any earlier ones for the same

2848. The two completed forms for this example are

tax matter(s) unless they checked the box on line 6 and

shown on the next pages.

attached a copy of the prior power of attorney that they

wanted to remain in effect.

Example. Stan and Mary Doe have been notified that

If Mary later decides that she can handle the examina-

their joint tax returns (Forms 1040) for 2009, 2010, and

tion on her own, she can revoke her power of attorney even

2011 are being examined. They have decided to appoint

though Stan does not revoke his power of attorney. (See

Jim Smith, an enrolled agent, to represent them in this

Revocation of Power of Attorney/Withdrawal of Represen-

matter and any future matters concerning these returns.

tative, earlier, for the special rules that apply.)

Jim, who has prepared returns at the same location for

years, already has a Centralized Authorization File (CAF)

Line 7—Signature of taxpayer. Stan and Mary each

number assigned to him. Mary does not want Jim to sign

signs and dates his or her Form 2848. If a taxpayer does

any agreements on her behalf, but Stan is willing to have

not sign, the IRS cannot accept the form.

Jim do so. They want copies of all notices and written

communications sent to Jim. This is the first time Stan and

Part II—Declaration of Representative. Jim Smith must

Mary have given power of attorney to anyone. They should

complete this part of Form 2848. If he does not sign this

each complete a Form 2848 as follows.

part, the IRS cannot accept the form.

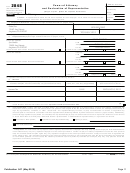

Line 1—Taxpayer information. Stan and Mary must

each file a separate Form 2848. On his separate Form

What Happens to the Power of

2848, Stan enters his name, street address, and social

Attorney When Filed?

security number in the spaces provided. Mary does like-

wise on her separate Form 2848.

A power of attorney will be recognized after it is received,

Line 2—Representative(s). On their separate Forms

reviewed, and determined by the IRS to contain the re-

2848, Stan and Mary each enters the name and current

quired information. However, until a power of attorney is

address of their chosen representative, Jim Smith. Both

entered on the CAF system, IRS personnel may be una-

Stan and Mary want Jim Smith to receive notices and

ware of the authority of the person you have named to

communications concerning the matters identified in line 3,

represent you. Therefore, during this interim period, IRS

so on their separate Forms 2848, Stan and Mary each

personnel may request that you or your representative

checks the box in the first column of line 2. They also enter

bring a copy to any meeting with the IRS.

Page 10

Publication 947 (May 2012)

ADVERTISEMENT

0 votes

Related Articles

Related forms

Form 150-800-005 Draft - Tax Information Authorization And Power Of Attorney For Representation - Oregon Department Of Revenue

Financial

Form 150-800-005 Draft - Tax Information Authorization And Power Of Attorney For Representation - Oregon Department Of Revenue

Financial

Tax Information Authorization And Power Of Attorney For Representation - Oregon Department Of Revenue

Financial

Tax Information Authorization And Power Of Attorney For Representation - Oregon Department Of Revenue

Financial

Related Categories

Parent category: Financial