Form Wv/it-104 - West Virginia Employee'S Withholding Exemption Certificate Page 16

ADVERTISEMENT

1

1 2

2 3

3 4

4 5

5 6

6 7

7 8

8 9

9 10

10 11

11 12

12 13

13 14

14 15

15 16

16 17

17 18

18 19

19 20

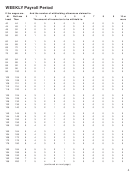

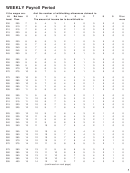

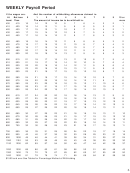

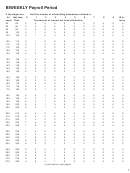

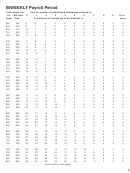

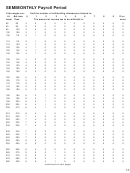

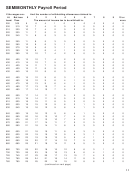

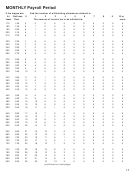

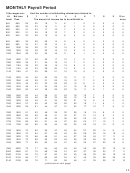

20USING THE PERCENTAGE METHOD TO FIGURE THE WITHHOLDING

The amount of tax to be withheld by the employer may be determined by the percentage method as follows:

(1) Subtract the personal exemptions credit as set forth in the table below. (The maximum personal exemp-

tion credit is $2,000.00 per year for each exemption.)

(2) Determine the amount of tax to be withheld from the appropriate percentage tables on the following pages.

PERSONAL EXEMPTION TABLE

WEEKLY ............................................... $

38.46

BIWEEKLY ........................................... $

76.92

SEMIMONTHLY .................................... $

83.33

MONTHLY ............................................ $

166.67

ANNUAL ................................................ $ 2,000.00

DAILY .................................................... $

7.66

(Note: Maximum allowable exemption credit is $2,000.00 annually per exemption.)

EXAMPLE: Employee Smith, who is married and his spouse works, earns $1,250.00 semimonthly and

claims two (2) exemptions. Using the percentage chart for TWO EARNER/TWO OR MORE

JOBS the following steps were taken to determine the state income tax to be withheld.

Step No. 1

Total Wage Payment ........................................................ $1,250.00

Less Personal Exemptions Per Table

above (2 exemptions—$83.33 x 2) ...................................

166.66

Total Wage Payment Less Personal Exemptions ...................................... $1,083.34

Step No. 2

Tax From Table 3 Entry covering $1,083.34

(Over $1,000 but not over $1,500) ....................................... 39.38

Plus 6% of excess over $1,000..... ....................................... .. 5.00

Total Tax to be withheld .............................................................................

$ 44.38

Round to the nearest dollar

$ 44.00

16

ADVERTISEMENT

0 votes

Related Articles

Related forms

Related Categories

Parent category: Financial