Form Nys-50 - Employer'S Guide To Unemployment Insurance, Wage Reporting, And Withholding Tax Page 40

ADVERTISEMENT

1

1 2

2 3

3 4

4 5

5 6

6 7

7 8

8 9

9 10

10 11

11 12

12 13

13 14

14 15

15 16

16 17

17 18

18 19

19 20

20 21

21 22

22 23

23 24

24 25

25 26

26 27

27 28

28 29

29 30

30 31

31 32

32 33

33 34

34 35

35 36

36 37

37 38

38 39

39 40

40 41

41 42

42 43

43 44

44 45

45 46

46 47

47 48

48 49

49 50

50 51

51 52

52Page 40 of 52 NYS-50 (1/14)

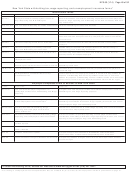

Unemployment insurance, wage reporting, and

withholding tax requirements for certain items of income

(continued)

Unemployment insurance and

Income item

Withholding tax requirement

wage reporting requirement

Fees

1. Speaker’s

No, unless for services as an employee.

No

2. Notary public

No

No

3. Jury or witness

No

No

4. Election official

No, unless for services as an employee.

No

Fishing-related activities

Yes

Yes, if subject to federal income tax withholding

because it is paid in cash.

No, if exempt from federal income tax

withholding because the income is derived by

Native Americans exercising fishing rights.

Fringe benefits (that are not allowed as a

deduction from the employee’s federal gross

income)

Yes, unless the employer elects not to withhold

1. Cars provided (personal use)

Yes

federal income tax and (1) gives the employee

advance written notice of the election, and

(2) includes the taxable amount of the benefit

as income on the employee’s wage and tax

statement.

Yes

Yes

2. Flights on aircraft furnished by employer

Yes

Yes

3. Free or discounted commercial flights

Yes

Yes

4. Discounts on property or services

Yes

Yes

5. Memberships in social clubs/country clubs

Yes

Yes

6. Tickets to entertainment or sports events

Yes

Yes

7. Outplacement services

Yes

Yes

8. Supper money

Yes

Yes

9. Reimbursement of employment agency fee

Yes (the reasonable value of any meals, rent,

Yes

10. Meals and lodging

and lodging provided by employers)

Gambling winnings

No

Yes, if the winnings are from the NYS Lottery,

are paid to an individual, and the proceeds from

such wager exceed $5,000.

No, if the winnings are from a wagering

transaction in a pari-mutuel pool for horse races,

regardless of the proceeds realized from such

wager.

Group-term life insurance

No

No

Household help

No, unless voluntary agreement to withhold

Yes

1. Employee compensation

New York State, New York City, or Yonkers tax

between employer and employee is in effect.

See New York State Tax Department bulletin

TB-MU-350, Hiring Household Help, for more

information.

2. Social security tax payments

No

No

(employer’s payment of employee’s share)

Income in respect of a decedent (regardless

No

Yes

of whether paid in year of death or year after

death)

Insurance proceeds (life insurance, endowment

No

No

contracts)

Interest and dividends

No

Yes, if for services.

Interest-free and below-market-interest-rate

No

Yes

loans (paid by employer)

No, regardless of whether the contributions to

IRA contributions

No, unless a salary reduction plan.

the plan are deductible or nondeductible from

the employee’s federal adjusted gross income.

ADVERTISEMENT

0 votes

Related Articles

Related forms

Tax Return - 2014")

Tax Return - 2011")

Related Categories

Parent category: Financial