Publication 54 - Tax Guide For U.s. Citizens And Resident Aliens Abord - 2011 Page 13

ADVERTISEMENT

1

1 2

2 3

3 4

4 5

5 6

6 7

7 8

8 9

9 10

10 11

11 12

12 13

13 14

14 15

15 16

16 17

17 18

18 19

19 20

20 21

21 22

22 23

23 24

24 25

25 26

26 27

27 28

28 29

29 30

30 31

31 32

32 33

33 34

34 35

35 36

36 37

37 38

38 39

39 40

40 41

41 42

42 43

43 44

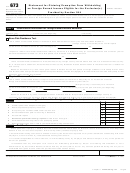

44Figure 4–A. Can I Claim Either Exclusion or the Deduction?

Start Here

Yes

Yes

No

No

Do you have foreign

Is your tax home in a

Are you a U.S. resident

Are you a U.S. citizen?

earned income?

foreign country?

alien?

No

No

Yes

Yes

Were you a bona fide

Are you a citizen or

resident of a foreign

national of a country

Yes

country or countries

with which the United

for an uninterrupted

States has an income

period that includes an

tax treaty in effect?

entire tax year?

No

Yes

No

You CAN claim the

foreign earned income

exclusion and the

foreign housing

exclusion or the foreign

*

housing deduction.

Were you physically

present in a foreign

Yes

country or countries for

at least 330 full days

during any period of 12

consecutive months?

No

You CANNOT claim the foreign earned income exclusion, the

foreign housing exclusion, or the foreign housing deduction.

*

Foreign housing exclusion applies only to employees. Foreign housing deduction applies only to the self-employed.

Temporary or

your expectation changes. Once your expecta-

those areas listed or described in the previous

Indefinite Assignment

sentence.

tion changes, it is indefinite.

The location of your tax home often depends on

Foreign Country

American Samoa,

whether your assignment is temporary or indefi-

nite. If you are temporarily absent from your tax

Guam, and the

To meet the bona fide residence test or the

home in the United States on business, you may

Commonwealth of the

be able to deduct your away-from-home ex-

physical presence test, you must live in or be

Northern Mariana Islands

penses (for travel, meals, and lodging), but you

present in a foreign country. A foreign country

would not qualify for the foreign earned income

includes any territory under the sovereignty of a

Residence or presence in a U.S. possession

exclusion. If your new work assignment is for an

government other than that of the United States.

does not qualify you for the foreign earned in-

indefinite period, your new place of employment

come exclusion. You may, however, qualify for

The term “foreign country” includes the coun-

becomes your tax home and you would not be

an exclusion of your possession income on your

try’s airspace and territorial waters, but not inter-

able to deduct any of the related expenses that

U.S. return.

national waters and the airspace above them. It

you have in the general area of this new work

also includes the seabed and subsoil of those

assignment. If your new tax home is in a foreign

American Samoa. There is a possession ex-

submarine areas adjacent to the country’s terri-

country and you meet the other requirements,

clusion available to individuals who are bona

torial waters over which it has exclusive rights

your earnings may qualify for the foreign earned

fide residents of American Samoa for the entire

under international law to explore and exploit the

income exclusion.

tax year. Gross income from sources within

natural resources.

If you expect your employment away from

American Samoa may be eligible for this exclu-

home in a single location to last, and it does last,

The term “foreign country” does not include

sion. Income that is effectively connected with

for 1 year or less, it is temporary unless facts

Antarctica or U.S. possessions such as Puerto

the conduct of a trade or business within Ameri-

and circumstances indicate otherwise.

Rico, Guam, the Commonwealth of the Northern

can Samoa also may be eligible for this exclu-

Mariana Islands, the U.S. Virgin Islands, and

If you expect it to last for more than 1 year, it

sion. Use Form 4563, Exclusion of Income for

is indefinite.

Johnston Island. For purposes of the foreign

Bona Fide Residents of American Samoa, to

earned income exclusion, the foreign housing

figure the exclusion.

If you expect it to last for 1 year or less, but at

exclusion, and the foreign housing deduction,

some later date you expect it to last longer than

the terms “foreign,” “abroad,” and “overseas”

Guam and the Commonwealth of the North-

1 year, it is temporary (in the absence of facts

refer to areas outside the United States and

ern Mariana Islands. An exclusion will be

and circumstances indicating otherwise) until

Chapter 4 Foreign Earned Income and Housing: Exclusion – Deduction

Page 13

ADVERTISEMENT

0 votes

Related Articles

Related forms

Publication 500 - Tax Guide For Wisconsin Political Organizations And Candidates - Department Of Revenue

Financial

Publication 500 - Tax Guide For Wisconsin Political Organizations And Candidates - Department Of Revenue

Financial

- Health And Human Services Agency") Form Dhcs 0001 - California U.s. Citizens And Nationals Applying For Medi-cal Must Show Proof Of Citizenship And Identity (korean) - Health And Human Services Agency

Legal

Form Dhcs 0001 - California U.s. Citizens And Nationals Applying For Medi-cal Must Show Proof Of Citizenship And Identity (korean) - Health And Human Services Agency

Legal

- Health And Human Services Agency")

- Health And Human Services Agency")

Related Categories

Parent category: Financial