Publication 501 - Exemptions, Standard Deduction, And Filing Information - 2001 Page 10

ADVERTISEMENT

1

1 2

2 3

3 4

4 5

5 6

6 7

7 8

8 9

9 10

10 11

11 12

12 13

13 14

14 15

15 16

16 17

17 18

18 19

19 20

20 21

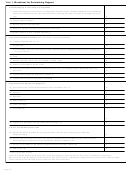

21Figure A. Can You Claim an Exemption for a Dependent?

Start Here

No

Was the person either a member of your household for the entire tax

year or related to you? (See Member of Household or Relationship Test.)

Yes

No

Was the person a U.S. citizen or resident, or a resident of Canada or

1

Mexico, for any part of the tax year?

Yes

Yes

2

Did the person file a joint return for the year?

No

You cannot

You can

claim an

Did you provide more than half the person’s total support for the

No

claim an

exemption

year? (If you are a divorced or separated parent of the person, see

exemption

3

for this

Support Test for Child of Divorced or Separated Parents.)

for this

person.

person.

Yes

No

Did the person have gross income of $2,900 or more during the tax

4

year?

Yes

No

Was the person your child?

Yes

Yes

Was your child under 19 at the end of the year?

No

Was your child under 24 at the end of the year and a full-time

No

Yes

student for some part of each of five months during the year? (See

Student under age 24.)

1

If the person was your legally adopted child and lived in your home as a member of your household for the entire tax year, answer “yes” to this question.

2

If neither the person nor the person’s spouse is required to file a return, but they file a joint return only to claim a refund of tax withheld, answer “no” to this

question.

3

Answer “yes” to this question if you meet the multiple support requirements under Multiple Support Agreement.

4

Gross income for this purpose does not include income received by a permanently disabled individual at a sheltered workshop. (See Disabled dependents.)

•

Your brother, sister, half brother, half sis-

Adoption. Even if your adoption of a child is

how the child became a member of the house-

ter, stepbrother, or stepsister.

not yet final, the child is considered to be your

hold.

child if he or she was placed with you for legal

•

Your parent, grandparent, or other direct

Cousin. You can claim an exemption for your

adoption by an authorized placement agency.

ancestor, but not foster parent.

cousin only if he or she lives with you as a

Also, the child must have been a member of

•

member of your household for the entire year. A

Your stepfather or stepmother.

your household. An authorized placement

cousin is a descendant of a brother or sister of

•

agency includes any person authorized by state

A brother or sister of your father or

your father or mother.

law to place children for legal adoption. If the

mother.

child was not placed with you by an authorized

Joint return. If you file a joint return, you do

•

A son or daughter of your brother or sister.

placement agency, the child will meet this test

not need to show that a person is related to both

•

only if he or she was a member of your house-

you and your spouse. You also do not need to

Your father-in-law, mother-in-law,

hold for your entire tax year.

show that a person is related to the spouse who

son-in-law, daughter-in-law,

provides support.

brother-in-law, or sister-in-law.

Foster child. A foster child must live with you

For example, your spouse’s uncle who re-

Any of these relationships that were established

as a member of your household for the entire

ceives more than half of his support from you

by marriage are not ended by death or divorce.

year to qualify as your dependent. For this test, a

may be your dependent, even though he does

foster child is one who is in your care that you

not live with you. However, if you and your

care for as your own child. It does not matter

spouse file separate returns, your spouse’s

Page 10

ADVERTISEMENT

0 votes

Related Articles

Related forms

Ftm Publication 1068 - Exempt Organizations - Requirements For Filing Returns And Paying Filing Fees

Financial

Ftm Publication 1068 - Exempt Organizations - Requirements For Filing Returns And Paying Filing Fees

Financial

Worksheet V And Vi - Standard Deduction And Qualified Mortgage Insurance Premiums Deduction

Financial

Worksheet V And Vi - Standard Deduction And Qualified Mortgage Insurance Premiums Deduction

Financial

Publication 517 - Social Security And Other Information For Members Of The Clergy And Religious Workers - 2003

Financial

Publication 517 - Social Security And Other Information For Members Of The Clergy And Religious Workers - 2003

Financial

Related Categories

Parent category: Financial