Publication 936 - Home Mortgage Interest Deduction - 2011 Page 9

ADVERTISEMENT

1

1 2

2 3

3 4

4 5

5 6

6 7

7 8

8 9

9 10

10 11

11 12

12 13

13 14

14 15

15 16

16Home Acquisition Debt

Example 1. You bought your main home on

include the painting costs in the cost of the

June 3 for $175,000. You paid for the home with

improvements.

cash you got from the sale of your old home. On

Home acquisition debt is a mortgage you took

Acquiring an interest in a home because of

July 15, you took out a mortgage of $150,000

out after October 13, 1987, to buy, build, or

EPS File Name: 10426g01

Size: Width = 14.0 picas,

a divorce. If you incur debt to acquire the

substantially improve a qualified home (your

secured by your main home. You used the

interest of a spouse or former spouse in a home,

main or second home). It also must be secured

$150,000 to invest in stocks. You can treat the

because of a divorce or legal separation, you

by that home.

mortgage as taken out to buy your home be-

can treat that debt as home acquisition debt.

If the amount of your mortgage is more than

cause you bought the home within 90 days

Part of home not a qualified home. To

the cost of the home plus the cost of any sub-

before you took out the mortgage. The entire

figure your home acquisition debt, you must

stantial improvements, only the debt that is not

mortgage qualifies as home acquisition debt be-

divide the cost of your home and improvements

more than the cost of the home plus improve-

cause it was not more than the home’s cost.

between the part of your home that is a qualified

ments qualifies as home acquisition debt. The

home and any part that is not a qualified home.

additional debt may qualify as home equity debt

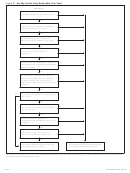

Example 2. On January 31, John began

See

Divided use of your home

under Qualified

(discussed later).

building a home on the lot that he owned. He

Home in Part I.

used $45,000 of his personal funds to build the

Home acquisition debt limit. The total

home. The home was completed on October 31.

amount you can treat as home acquisition debt

Home Equity Debt

On November 21, John took out a $36,000 mort-

at any time on your main home and second

gage that was secured by the home. The mort-

home cannot be more than $1 million ($500,000

If you took out a loan for reasons other than to

gage can be treated as used to build the home

if married filing separately). This limit is reduced

buy, build, or substantially improve your home, it

because it was taken out within 90 days after the

(but not below zero) by the amount of your

may qualify as home equity debt. In addition,

home was completed. The entire mortgage

grandfathered debt (discussed later). Debt over

debt you incurred to buy, build, or substantially

qualifies as home acquisition debt because it

this limit may qualify as home equity debt (also

improve your home, to the extent it is more than

was not more than the expenses incurred within

discussed later).

the home acquisition debt limit (discussed ear-

the period beginning 24 months before the

lier), may qualify as home equity debt.

home was completed. This is illustrated by

Refinanced home acquisition debt. Any se-

Home equity debt is a mortgage you took out

Figure C.

cured debt you use to refinance home acquisi-

after October 13, 1987, that:

Figure C.

tion debt is treated as home acquisition debt.

•

However, the new debt will qualify as home

Does not qualify as home acquisition debt

Home

acquisition debt only up to the amount of the

or as grandfathered debt, and

John

Completed

balance of the old mortgage principal just before

•

Is secured by your qualified home.

the refinancing. Any additional debt not used to

Starts

($45,000 in

$36,000

buy, build, or substantially improve a qualified

Building

Personal

Mortgage

home is not home acquisition debt, but may

Example. You bought your home for cash

Home

Funds Used)

Taken Out

qualify as home equity debt (discussed later).

10 years ago. You did not have a mortgage on

your home until last year, when you took out a

Mortgage that qualifies later. A mortgage

$20,000 loan, secured by your home, to pay for

Jan. 31

Oct. 31

Nov. 21

that does not qualify as home acquisition debt

your daughter’s college tuition and your father’s

because it does not meet all the requirements

medical bills. This loan is home equity debt.

may qualify at a later time. For example, a debt

Home equity debt limit. There is a limit on the

that you use to buy your home may not qualify

amount of debt that can be treated as home

as home acquisition debt because it is not se-

9 Months

22 Days

equity debt. The total home equity debt on your

cured by the home. However, if the debt is later

(Within 24 Months)

(Within 90 Days)

main home and second home is limited to the

secured by the home, it may qualify as home

smaller of:

acquisition debt after that time. Similarly, a debt

Date of the mortgage. The date you take

that you use to buy property may not qualify

•

$100,000 ($50,000 if married filing sepa-

out your mortgage is the day the loan proceeds

because the property is not a qualified home.

rately), or

are disbursed. This is generally the closing date.

However, if the property later becomes a quali-

•

You can treat the day you apply in writing for

The total of each home’s fair market value

fied home, the debt may qualify after that time.

your mortgage as the date you take it out. How-

(FMV) reduced (but not below zero) by the

Mortgage treated as used to buy, build, or

ever, this applies only if you receive the loan

amount of its home acquisition debt and

improve home. A mortgage secured by a

proceeds within a reasonable time (such as

grandfathered debt. Determine the FMV

qualified home may be treated as home acquisi-

within 30 days) after your application is ap-

and the outstanding home acquisition and

tion debt, even if you do not actually use the

proved. If a timely application you make is re-

grandfathered debt for each home on the

proceeds to buy, build, or substantially improve

jected, a reasonable additional time will be

date that the last debt was secured by the

the home. This applies in the following situa-

allowed to make a new application.

home.

tions.

Cost of home or improvements. To deter-

1. You buy your home within 90 days before

Example. You own one home that you

mine your cost, include amounts paid to acquire

or after the date you take out the mort-

bought in 2000. Its FMV now is $110,000, and

any interest in a qualified home or to substan-

gage. The home acquisition debt is limited

the current balance on your original mortgage

tially improve the home.

to the home’s cost, plus the cost of any

(home acquisition debt) is $95,000. Bank M of-

The cost of building or substantially improv-

substantial improvements within the limit

fers you a home mortgage loan of 125% of the

ing a qualified home includes the costs to ac-

described below in (2) or (3). (See Exam-

FMV of the home less any outstanding mort-

ple 1 below.)

quire real property and building materials, fees

gages or other liens. To consolidate some of

for architects and design plans, and required

your other debts, you take out a $42,500 home

2. You build or improve your home and take

mortgage loan [(125% × $110,000) − $95,000]

building permits.

out the mortgage before the work is com-

with Bank M.

Substantial improvement. An improve-

pleted. The home acquisition debt is lim-

Your home equity debt is limited to $15,000.

ited to the amount of the expenses

ment is substantial if it:

This is the smaller of:

incurred within 24 months before the date

•

Adds to the value of your home,

•

of the mortgage.

$100,000, the maximum limit, or

•

Prolongs your home’s useful life, or

•

3. You build or improve your home and take

$15,000, the amount that the FMV of

•

out the mortgage within 90 days after the

Adapts your home to new uses.

$110,000 exceeds the amount of home

work is completed. The home acquisition

acquisition debt of $95,000.

debt is limited to the amount of the ex-

Repairs that maintain your home in good con-

penses incurred within the period begin-

dition, such as repainting your home, are not

Debt higher than limit.

Interest on

substantial improvements. However, if you paint

ning 24 months before the work is

amounts over the home equity debt limit (such

as the interest on $27,500 [$42,500 − $15,000]

completed and ending on the date of the

your home as part of a renovation that substan-

mortgage. (See Example 2 below.)

tially improves your qualified home, you can

in the preceding example) generally is treated

Publication 936 (2011)

Page 9

ADVERTISEMENT

0 votes

Related Articles

Related forms

Related Categories

Parent category: Financial