Instructions For Filing: Personal & School District Income Tax - Department Of Taxation State Of Ohio - 2014 Page 17

ADVERTISEMENT

1

1 2

2 3

3 4

4 5

5 6

6 7

7 8

8 9

9 10

10 11

11 12

12 13

13 14

14 15

15 16

16 17

17 18

18 19

19 20

20 21

21 22

22 23

23 24

24 25

25 26

26 27

27 28

28 29

29 30

30 31

31 32

32 33

33 34

34 35

35 36

36 37

37 38

38 39

39 40

40 41

41 42

42 43

43 44

44 45

45 46

46 47

47 48

48 49

49 50

50 51

51 52

52 53

53 54

54 55

55 56

56 57

57 58

58 59

59 60

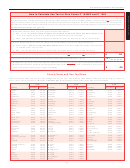

602014 Ohio Forms IT 1040EZ / IT 1040 / Instructions

If your taxable income is less than

If you do not qualify for the joint fi ling credit,

form IT/SD 2210 to determine if a penalty is

$100,000, your tax has been calculated

enter -0- on line 11. If you do qualify for the

due. This form is available on our Web site

for you as shown on Income Tax Table 1,

joint fi ling credit, calculate it this way:

at tax.ohio.gov.

or you can use Income Tax Table 2.

EZ Line 16 – Unpaid Use (Sales) Tax

If your taxable income is $100,000 or

If your Ohio taxable

more, you must use Income Tax Table

income (line 5) is:

Your credit is:

Use line 16 of Ohio form IT 1040EZ to re-

2.

port the amount of unpaid use (sales) tax,

$25,000 or less............. 20% of line 10a

if any, that you may owe from out-of-state

Note: Income Tax Table 1 shows the tax

More than $25,000,

purchase(s) that you made in 2014 (for

amount for $50 increments of income and

but not more than

example, mail order or Internet purchases).

is calculated on the midpoint income for

$50,000 ........................ 15% of line 10a

Complete the worksheet on page 35. A

all of the income in that $50 range. The

detailed explanation of the Ohio use tax is

tax amount listed on Income Tax Table 1

More than $50,000,

on page 34.

may be slightly lower or higher than the

but not more than

tax amount computed by using Income

$75,000 ........................ 10% of line 10a

If you did not make any out-of-state purchas-

Tax Table 2.

es during 2014, enter -0- on line 16. If you did

More than $75,000 ......... 5% of line 10a

EZ Line 9 – Exemption Credit

make any out-of-state purchase during 2014

This credit is limited to a maximum

and if you paid no sales tax on that purchase,

of $650.

For taxable years beginning on or after

then you are required to complete the use

Jan. 1, 2014, the $20 personal and de-

tax worksheet on page 35 to determine the

pendent exemption credit is only available

Example 2: If your Ohio taxable income (line

amount of Ohio use tax you owe (which is

to taxpayers with Ohio taxable income of

the sales tax on that purchase).

5) is $20,000 and the amount on line 10a is

less than $30,000. Ohio taxable income is

$303, then the joint fi ling credit will be $61:

EZ Line 18 – Ohio Income Tax Withheld

defi ned as Ohio adjusted gross income less

$303 – from line 10a

exemptions. If Ohio taxable income is less

Enter the total amount of Ohio income tax

x .20 – from table above

than $30,000, multiply your total number of

withheld. This is normally shown on your tax

personal and dependent exemptions by $20

statement form (W-2, box 17; W-2G, box 15;

Joint fi ling credit = $61 (rounded)

and enter on line 9.

or 1099-R, box 12). See the sample W-2 and

If you qualify for this credit, but you and your

EZ Line 11 – Joint Filing Credit

W-2G on page 14 and the sample 1099-R

spouse do not each have a W-2 form show-

on page 15.

ing $500 or more of income, then you must

To qualify for this credit,

Place legible state copies of your W-2(s),

include with the return a separate statement

you and your spouse must

W-2G(s) or 1099-R(s) after the last page

!

explaining the income that qualifi es for this

each have qualifying Ohio

of Ohio form IT 1040EZ. Do not staple or

credit. You must show that each spouse has

adjusted gross income of

otherwise attach.

CAUTION

$500 or more of qualifying income included

at least $500 after you have

You cannot claim on the Ohio return any

in Ohio adjusted gross income (line 3) in

fi gured your line 2 adjustments.

taxes withheld for another state, a city or

order to take the joint fi ling credit.

a school district.

If you are a married couple fi ling a joint Ohio

If you are a direct or indirect investor in a

EZ Line 13 – Earned Income Credit

income tax return, you may qualify for a joint

pass-through entity, you cannot claim on

fi ling credit. You can take this credit only if

this line taxes withheld on your behalf by

For taxable years beginning on or after Jan.

each spouse has qualifying Ohio adjusted

a pass-through entity. For proper report-

1, 2014, a nonbusiness, nonrefundable

gross income of $500 or more. Qualifying

ing of taxes withheld on your behalf by

earned income credit is available for taxpay-

Ohio adjusted gross income does not in-

a pass-through entity, use Ohio form IT

ers who were eligible for the federal earned

clude income from Social Security benefi ts,

1040 and see line 72b on page 33.

income tax credit (EITC) on their federal tax

most railroad retirement benefi ts, uniformed

returns. The Ohio earned income credit is

EZ Line 20 – Donations

services retirement income, interest, dividend

equal to 10% of the taxpayer's federal EITC.

and capital gain distributions, royalties, rents,

A donation will reduce the

capital gains, and state or local income tax

However, if the taxpayer's Ohio taxable

STOP

amount of the refund that you

refunds. This credit is limited to a maximum

income (Ohio adjusted gross income less

are due. If you decide to donate,

of $650 (see the following examples).

exemptions) exceeds $20,000 on either an

this decision is fi nal. If you do not want

individual or joint tax return, then the credit is

Example 1: Bob and Sue fi le a joint return.

to donate, leave lines 20a-e blank. If you

limited to 50% of the tax otherwise due after

Sue earned $200,000 from her current em-

do not have an overpayment on line 19

deducting all other credits that precede the

ployment. Bob's only source of income is

but you want to donate, you may do

credit except for the joint fi ling credit. See

$500 from his state and municipal income

so by writing a check and mailing it di-

the worksheet on page 20.

tax refunds included in federal adjusted

rectly to the fund. See page 36 for more

gross income. This $500 is deducted on

information.

EZ Line 15 – Interest Penalty

line 2 and is not included in Bob and Sue's

EZ Line 23 – Interest and Penalty Due

Ohio adjusted gross income. Therefore,

If line 14 minus the withholding shown on

they do not qualify for Ohio's joint fi ling

line 18 is $500 or less, enter -0- on line 15.

Except for certain military servicemembers

credit. However, if Bob had another source

If line 14 minus the withholding shown on

(see "Income Taxes and the Military" on

of qualifying income of $500 or more not

line 18 is greater than $500, you may owe

page 12), interest is due from April 16, 2015

deducted on line 2, he and Sue would

an interest penalty. You must complete Ohio

until the date the tax is paid.

qualify for the credit.

- 17 -

ADVERTISEMENT

0 votes

Related Articles

Related forms

Instructions For Filing: Personal & School District Income Tax & Telefile - Department Of Taxation State Of Ohio - 2012

Financial

Instructions For Filing: Personal & School District Income Tax & Telefile - Department Of Taxation State Of Ohio - 2012

Financial

Instructions For Filing The School District Estate Income Tax Return - Ohio School District Income Tax

Financial

Instructions For Filing The School District Estate Income Tax Return - Ohio School District Income Tax

Financial

Instructions For Form It-2210 - Interest Penalty On Underpayment Of Ohio Or School District Income Tax

Financial

Instructions For Form It-2210 - Interest Penalty On Underpayment Of Ohio Or School District Income Tax

Financial

Instructions For Form It-2105 - Estimated Income Tax Payment Voucher For Individuals - New York State Department Of Taxation And Finance - 1999

Financial

Instructions For Form It-2105 - Estimated Income Tax Payment Voucher For Individuals - New York State Department Of Taxation And Finance - 1999

Financial

Instructions For Form It-220 - Minimum Income Tax - New York State Department Of Taxation And Finance - 2004

Financial

Instructions For Form It-220 - Minimum Income Tax - New York State Department Of Taxation And Finance - 2004

Financial

Related Categories

Parent category: Financial