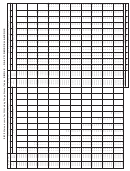

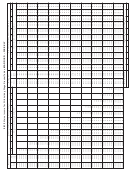

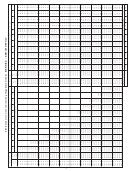

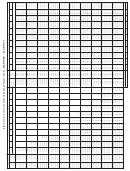

Withholding Tables For Individual Income Tax - Maine Revenue Services - 2013 Page 2

ADVERTISEMENT

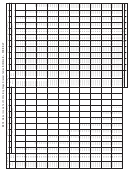

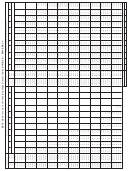

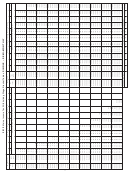

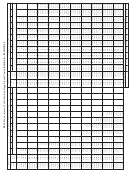

1

1 2

2 3

3 4

4 5

5 6

6 7

7 8

8 9

9 10

10 11

11 12

12 13

13 14

14 15

15 16

16 17

17 18

18 19

19 20

20authorization is initiated through a telephone call to the MRS electronic

Use EZ Pay

withdrawal payment system (207-624-7777). This telephone payment

system allows taxpayers to arrange for debit payments with effective

dates up to 15 days in the future. The amount you enter will be

deducted from your account within three business days from the date

you authorize the transfer.

ELECTRONIC PAYMENT OPTIONS

Penalty for Insuffi cient Funds. The penalty for insuffi cient funds

Maine Revenue Services (“MRS”) offers a convenient 24-hour electronic

applies to electronic funds transfers. The penalty is $20 or 1% of the

payment option called EZ Pay. You can access EZ Pay on our web site

payment amount, whichever is greater.

at /netfi le/ezpay.htm. Almost any type of tax

payment can be made, including withholding and unemployment taxes.

Penalty for Failure to Pay by Electronic Funds Transfer. Any person

To avoid having to make payments earlier than necessary, payments

required to pay by electronic funds transfer who fails to do so is liable

may be scheduled in advance and will automatically be withdrawn on

for a penalty equal to the lesser of 5% of the tax due or $5,000.

the payment date you select.

For a copy of Rule 102 or an EFT application, go to

To use EZ Pay, simply register online at the time you want to make

revenue/eft. You can send an email to efunds.transfer@maine.gov or

your fi rst payment. Once registered, the system will ask you to select

send a fax to (207) 287-6975; call (207) 624-5625; or write to:

the tax type you want to pay. If you are making a semiweekly payment,

EFT Unit

select “900ME Withholding Semiweekly Payment.” If you are paying a

Maine Revenue Services

tax balance due with your quarterly combined return, select “941/C1-

PO Box 1060

ME Combined Withholding/Unemployment Payment.” If you are paying

Augusta, ME 04332-1060.

a balance due from a bill or notice that you received from MRS, select

“Bill Payment.” If you make semiweekly payments electronically, do not

PAYROLL PROCESSING COMPANIES

send paper copies of Form 900ME to MRS.

MRS accepts both ACH credit method and ACH Teledebit payments

Payroll processors must register annually with, and be licensed by

for combined income tax withholding and unemployment contributions

the Bureau of Consumer Credit Protection. For more information on

quarterly returns. Both ACH payment methods require registration

the licensing requirements, contact the Superintendent, Bureau of

Consumer Credit Protection by phone (207) 624-8527, by fax (207)

applications to participate. Payroll processing companies must remit

electronically for all clients, even if clients are not mandated to pay

582-7699 or by writing: 35 State House Station, Augusta, ME 04333.

electronically. A payroll processing company may request a waiver

PASS-THROUGH ENTITIES

from this requirement for good cause. MRS also encourages voluntary

participation in the EZ Pay program by those not required to pay

In

addition

to

employee

withholding,

pass-through

entities

electronically. There are no payment minimums.

(partnerships, S corporations, LLCs) with nonresident members

(partners, shareholders, etc.) must withhold income taxes from those

ACH Credit. A taxpayer may make payments using this method by

nonresident members on Maine-source distributive income. Estimate

authorizing their bank to withdraw the tax payment from the taxpayer’s

payments must be remitted to the state quarterly. Certain exemptions

deposit account and transfer it to the state’s account.

You must

apply. Pass-through entities must withhold income taxes at the highest

have previously established a relationship with a bank that provides

Maine rate -- do not use this booklet to calculate withholding for

this service (generally larger commercial banks) and you must have

nonresident members. For more information, see Form 941P at

previously registered with the MRS EFT Unit as a credit method

/forms.

payer.

ACH Teledebit. A taxpayer may make payments using this method

by authorizing MRS to electronically transfer tax payments from

the taxpayer’s deposit account to the MRS deposit account. The

Dos and Don’ts for Clients of Payroll Processors in Maine:

Using the services of a payroll processor can be a convenient and economical way for an employer or non-wage fi ler to fi le and pay withholding taxes.

However, employers or non-wage fi lers face certain risks associated with the use of a processor, including possible lack of compliance and the risk

of loss of funds that are under the control of the processor. Ultimately, it is the employer or non-wage fi ler that bears the responsibility for meeting its

payroll tax obligations. If you are an employer or non-wage fi ler that uses the services of a payroll processor, you should take the following

precautions:

Educate yourself to understand your fi ling requirements and the risks associated with using a payroll processor.

Verify with the

Bureau of Consumer Credit Protection by phone (207) 624-8527, by fax (207) 582-7699 or by writing: 35 State House

Station, Augusta, ME 04333

that the processor is licensed and has provided proof of liability insurance to protect client funds, including

coverage for crimes such as fraud and theft. If the processor has access to your company’s funds, verify with the state that the processor has

also posted a surety bond.

Obtain verifi cation from the payroll processor and its insurer that the processor’s liability insurance will remain in effect for a specifi ed period of

time.

Read your contract with your processor carefully.

Ensure that the agreement/contract and any power of attorney that your processor has with you specifi cally requires that all notices sent by the

IRS and state tax agencies be sent directly to you.

Never hesitate to contact tax authorities directly when you feel it necessary.

Check with the appropriate tax agency periodically to ensure that returns and payments are fi led in a timely manner.

Insist on verifi cation from your processor that any problem for which the employer has received a tax agency notice has been resolved.

Never assume that everything is fi ne solely because you have not received notice of any problems.

Never sign a tax return before it is completed.

Require that the processor provide copies of returns, not just summaries, at the time of fi ling.

If you are using a nationwide payroll service, be sure you are assigned a direct contact person and telephone

number.

2

ADVERTISEMENT

0 votes

Related Articles

Related forms

1040s-me Resident Short Form - Maine Individual Income Tax - Maine Revenue Services - 2009

Financial

1040s-me Resident Short Form - Maine Individual Income Tax - Maine Revenue Services - 2009

Financial

Form 941af-me - Nonresident Member Affidavit And Agreement To Comply With Maine Income Tax - Maine Revenue Services - 2004

Financial

Form 941af-me - Nonresident Member Affidavit And Agreement To Comply With Maine Income Tax - Maine Revenue Services - 2004

Financial

- 2013")

Tax Calculation Schedule For Individual Income Tax - Nebraska Department Of Revenue - 2014

Financial

Tax Calculation Schedule For Individual Income Tax - Nebraska Department Of Revenue - 2014

Financial

Related Categories

Parent category: Financial