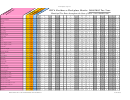

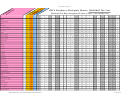

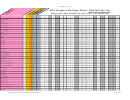

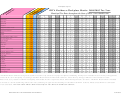

Instructions For Completing Form 11 - Employer'S Municipal Tax Withholding Statement Page 7

ADVERTISEMENT

1

1 2

2 3

3 4

4 5

5 6

6 7

7 8

8 9

9 10

10 11

11 12

12SPECIAL CHANGES

* Macedonia and the Macedonia / Northfield Center Twp. JEDD are new

members as of 10-1-2004.

* Grove City new member as of 7-1-2004

* Sabina new member as of 5-27-2004

* Sherwood new member and new tax as of 7-1-2004

* Wellsville new member as of 2-1-2004

****************************************************************************************************

Changes to the Ohio Revised Code 718.03

The State legislature has amended Ohio Revised Code 718.03 (municipal income tax) to

require that all employers withhold on the same wage base (known as “qualifying wages”)

for municipal income tax purposes. This amendment was contained in House Bill 95

(2003) and is effective January 1, 2004. Beginning on that date, all employers will withhold

municipal income tax as follows:

The tax and withholding base begins with the Medicare wage base (Box 5). Please note the

following guidelines illustrated below:

i.

Supplemental unemployment compensation benefits described in

section 3402(o)(2) of IRC are taxable;

ii.

Add compensation of pre-1986 employees exempt from Medicare

that is not in the Medicare wage base solely because of the

Medicare grandfathering provision.

iii.

IRC section 125 cafeteria plans are not taxable.

The required base may be modified, on a municipality-by-municipality basis, if the

municipality, by resolution or ordinance, exempts from the tax and from withholding (i) stock

options and/or (ii) non-qualified deferred compensation amounts.

ADVERTISEMENT

0 votes

Related Articles

Related forms

Related Categories

Parent category: Financial