Publication 971 - Innocent Spouse Relief - Internal Revenue Service Page 17

ADVERTISEMENT

1

1 2

2 3

3 4

4 5

5 6

6 7

7 8

8 9

9 10

10 11

11 12

12 13

13 14

14 15

15 16

16 17

17 18

18 19

19 20

20 21

21 22

22 23

23 24

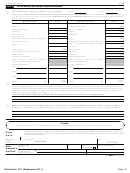

24Figure B. Do You Qualify for Separation of Liability Relief?

Start Here

You do not qualify for separation of

liability relief but you may qualify for

No

Did you file a joint return for the year you want

relief from liability arising from

relief?

community property law. See

Community Property Laws earlier.

Yes

Will you file Form 8857 no later than 2 years

You do not qualify for separation of

No

after the first IRS attempt to collect the tax

liability relief but you may qualify for

*

from you that occurs after July 22, 1998

?

equitable relief. See Figure C later.

Yes

No

Does your joint return have an understated tax?

Yes

Are you still married to the spouse with whom

you filed the joint return? (If that spouse is

No

deceased, answer “No.”)

Yes

Yes

Are you legally separated from the spouse with

whom you filed the joint return?

No

Yes

Were you a member of the same household as

the spouse with whom you filed the joint return

at any time during the 12-month period ending

on the date you file Form 8857?

No

You do not qualify for separation of liability

relief; go to Figure C.

You may qualify for separation of liability relief.

*

Collection activities that may start the 2-year period are described earlier under How To Request Relief.

Publication 971 (September 2011)

Page 17

ADVERTISEMENT

0 votes

Related Articles

Related forms

Form Publication 784 - Department Of Treasury Internal Revenue Service - Certificate Of Subordination Of Federal Tax Lien

Financial

Form Publication 784 - Department Of Treasury Internal Revenue Service - Certificate Of Subordination Of Federal Tax Lien

Financial

- Innocent Spouse Relief")

For Individuals, Estates, And Trusts - Internal Revenue Service - 2006") Publication 536 - Net Operating Losses (nols) For Individuals, Estates, And Trusts - Internal Revenue Service - 2006

Financial

Publication 536 - Net Operating Losses (nols) For Individuals, Estates, And Trusts - Internal Revenue Service - 2006

Financial

- Internal Revenue Service - 2012")

Publication 957 - Reporting Back Pay And Special Wage Payments To The Social Security Administration - Internal Revenue Service

Financial

Publication 957 - Reporting Back Pay And Special Wage Payments To The Social Security Administration - Internal Revenue Service

Financial

Reporting Information - Internal Revenue Service")

Related Categories

Parent category: Financial