Form 2 - Montana Individual Income Tax Return - 2008 Page 7

Download a blank fillable Form 2 - Montana Individual Income Tax Return - 2008 in PDF format just by clicking the "DOWNLOAD PDF" button.

Open the file in any PDF-viewing software. Adobe Reader or any alternative for Windows or MacOS are required to access and complete fillable content.

Complete Form 2 - Montana Individual Income Tax Return - 2008 with your personal data - all interactive fields are highlighted in places where you should type, access drop-down lists or select multiple-choice options.

Some fillable PDF-files have the option of saving the completed form that contains your own data for later use or sending it out straight away.

ADVERTISEMENT

1

1 2

2 3

3 4

4 5

5 6

6 7

7 8

8 9

9Clear Form

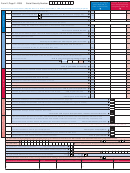

Form 2, Page 7 - 2008

Social Security Number:

Column A (for single,

Column B (for spouse

Schedule V - Montana Tax Credits

joint, separate, or

when fi ling separately

Enter on the corresponding line your Montana tax credits.

head of household)

using fi ling status 3a)

File Schedule V with your Montana Form 2.

Nonrefundable credits that are single-year credits and HAVE NO carryover provision

1 Credit for an income tax liability paid to another state or country from

Form 2, Schedules VI, line 10 or VII, line 10.

1

1

2 College contribution credit. Attach Form CC.

2

2

3 Qualifi ed endowment credit. Attach Form QEC.

3

3

4 Energy conservation installation credit. Attach Form ENRG-C.

4

4

5 Alternative fuel credit. Attach Form AFCR.

5

5

6 Rural physician’s credit.

6

6

7 Health insurance for uninsured Montanans credit. Attach Form HI.

7

7

8 Elderly care credit. Attach Form ECC.

8

8

9 Recycle credit. Attach Form RCYL.

9

9

10 Oilseed crushing and biodiesel/biolubricant production facility credit. Attach Form OSC.

10

10

11 Biodiesel blending and storage credit. Attach Form BBSC.

11

11

Nonrefundable credits that HAVE a carryover provision

12 Contractor’s gross receipts tax credit.

12

12

13 Geothermal systems credit. Attach Form ENRG-A.

13

13

14 Alternative energy systems credit. Attach Form ENRG-B.

14

14

15 Alternative energy production credit. Attach Form AEPC.

15

15

16 Dependent care assistance credit. Attach Form DCAC.

16

16

17 Historic property preservation credit. Attach federal Form 3468.

17

17

18 Infrastructure users fee credit.

18

18

19 Empowerment zone credit.

19

19

20 Increasing research activities credit. Attach Form RSCH.

20

20

21 Mineral exploration incentive credit. Attach Form MINE-CRED.

21

21

22 Film employment production credit. Attach Form FPC. Report your credit on

this line if you have made the one-time four year carry forward election.

22

22

23 Adoption credit. Attach federal Form 8839.

23

23

24 Add lines 1 through 23 and enter result here and on Form 2, line 51.

24

24

This is your total nonrefundable credits.

Refundable credits

25 Elderly homeowner/renter credit. Attach Form 2EC.

25

25

26 Film employment production credit. Attach Form FPC.

26

26

27 Film qualifi ed expenditure credit. Attach Form FPC.

27

27

28 Insure Montana small business health insurance credit. Business FEIN:

28

28

29 Temporary Emergency Lodging credit. Attach Form TELC.

29

29

30 Add lines 25 through 29 and enter result here and on Form 2, line 58.

30

30

This is your total refundable credits.

Montana Tax Credits

Nonrefundable carryover credits.

We have listed the 27 Montana tax credits available to you under

Your nonrefundable carryover credits can be used to offset your

three categories. With the exception of the capital gains tax credit,

2008 resident, nonresident, or part-year resident tax after capital

which is required to be applied before any other credit, you are not

gains credit and cannot reduce your tax liability below zero. Your

required to apply any of these 27 tax credits against your income

excess credits that were not applied against your 2008 income

tax liability in any particular order.

tax liability can be carried over and used to offset future year tax

liabilities.

Nonrefundable single-year credits.

Refundable credits.

Your nonrefundable single-year credits can only be used to offset

your 2008 resident, nonresident, or part-year resident tax after

Your refundable credits are applied against your income tax liability

capital gains credit and cannot reduce your tax liability below zero.

with any unused credit refunded to you.

The unused portion that exceeded your 2008 income tax liability

cannot be used in future years.

ADVERTISEMENT

0 votes

Related Articles

Related forms

Related Categories

Parent category: Financial