Form 706 - United States Estate (And Generation-Skipping Transfer) Tax Return Page 18

Download a blank fillable Form 706 - United States Estate (And Generation-Skipping Transfer) Tax Return in PDF format just by clicking the "DOWNLOAD PDF" button.

Open the file in any PDF-viewing software. Adobe Reader or any alternative for Windows or MacOS are required to access and complete fillable content.

Complete Form 706 - United States Estate (And Generation-Skipping Transfer) Tax Return with your personal data - all interactive fields are highlighted in places where you should type, access drop-down lists or select multiple-choice options.

Some fillable PDF-files have the option of saving the completed form that contains your own data for later use or sending it out straight away.

ADVERTISEMENT

Tax Return Printable pdf") 1

1 2

2 3

3 4

4 5

5 6

6 7

7 8

8 9

9 10

10 11

11 12

12 13

13 14

14 15

15 16

16 17

17 18

18 19

19 20

20 21

21 22

22 23

23 24

24 25

25 26

26 27

27 28

28 29

29 30

30 31

31 32

32 33

33 34

34 35

35 36

36 37

37 38

38 39

39 40

40 41

41 42

42 43

43 44

44 45

45 46

46Form 706 (Rev. 11-01)

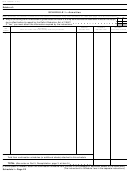

Instructions for Schedule E—Jointly Owned

Part 2—Other joint interests. All joint interests that

were not entered in Part 1 must be entered in Part 2.

Property

For each item of property, enter the appropriate

If you are required to file Form 706, you must complete

letter A, B, C, etc., from line 2a to indicate the name

Schedule E and file it with the return if the decedent

and address of the surviving co-tenant.

owned any joint property at the time of death, whether

Under “Description,” describe the property as

or not the decedent’s interest is includible in the gross

estate.

required in the instructions for Schedules A, B, C, and

F for the type of property involved.

Enter on this schedule all property of whatever kind

or character, whether real estate, personal property, or

In the “Percentage includible” column, enter the

bank accounts, in which the decedent held at the time

percentage of the total value of the property that you

intend to include in the gross estate.

of death an interest either as a joint tenant with right to

survivorship or as a tenant by the entirety.

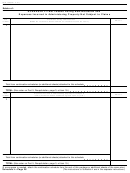

Generally, you must include the full value of the

jointly owned property in the gross estate. However,

Do not list on this schedule property that the

the full value should not be included if you can show

decedent held as a tenant in common, but report the

that a part of the property originally belonged to the

value of the interest on Schedule A if real estate, or on

other tenant or tenants and was never received or

the appropriate schedule if personal property. Similarly,

acquired by the other tenant or tenants from the

community property held by the decedent and spouse

decedent for less than adequate and full consideration

should be reported on the appropriate Schedules A

through I. The decedent’s interest in a partnership

in money or money’s worth, or unless you can show

should not be entered on this schedule unless the

that any part of the property was acquired with

partnership interest itself is jointly owned. Solely

consideration originally belonging to the surviving joint

tenant or tenants. In this case, you may exclude from

owned partnership interests should be reported on

the value of the property an amount proportionate to

Schedule F, “Other Miscellaneous Property.”

the consideration furnished by the other tenant or

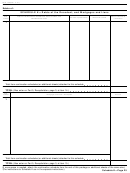

Part 1—Qualified joint interests held by decedent

tenants. Relinquishing or promising to relinquish dower,

and spouse. Under section 2040(b)(2), a joint interest

curtesy, or statutory estate created instead of dower or

is a qualified joint interest if the decedent and the

curtesy, or other marital rights in the decedent’s

surviving spouse held the interest as:

property or estate is not consideration in money or

● Tenants by the entirety, or

money’s worth. See the Schedule A instructions for the

● Joint tenants with right of survivorship if the

value to show for real property that is subject to a

decedent and the decedent’s spouse are the only

mortgage.

joint tenants.

If the property was acquired by the decedent and

Interests that meet either of the two requirements

another person or persons by gift, bequest, devise, or

above should be entered in Part 1. Joint interests that

inheritance as joint tenants, and their interests are not

do not meet either of the two requirements above

otherwise specified by law, include only that part of the

should be entered in Part 2.

value of the property that is figured by dividing the full

value of the property by the number of joint tenants.

Under “Description,” describe the property as

required in the instructions for Schedules A, B, C, and

If you believe that less than the full value of the

F for the type of property involved. For example, jointly

entire property is includible in the gross estate for tax

held stocks and bonds should be described using the

purposes, you must establish the right to include the

rules given in the instructions to Schedule B.

smaller value by attaching proof of the extent, origin,

and nature of the decedent’s interest and the

Under “Alternate value” and “Value at date of

interest(s) of the decedent’s co-tenant or co-tenants.

death,” enter the full value of the property.

In the “Includible alternate value” and “Includible

Note: You cannot claim the special treatment under

value at date of death” columns, you should enter only

section 2040(b) for property held jointly by a decedent

the values that you believe are includible in the gross

and a surviving spouse who is not a U.S. citizen. You

estate.

must report these joint interests on Part 2 of

Schedule E, not Part 1.

Schedule E—Page 18

ADVERTISEMENT

0 votes

Related Articles

Related forms

Tax Return")

Tax Return")

Tax Return")

Tax Return")

Tax Return")

Tax Return")

Tax Return - 2011") Instructions For Form 706 - United States Estate (and Generation-skipping Transfer) Tax Return - 2011

Financial

Instructions For Form 706 - United States Estate (and Generation-skipping Transfer) Tax Return - 2011

Financial

Tax Return - 2008") Instructions For Form 706 - United States Estate (and Generation-skipping Transfer) Tax Return - 2008

Financial

Instructions For Form 706 - United States Estate (and Generation-skipping Transfer) Tax Return - 2008

Financial

Tax Return - 2005")

Tax Return")

Related Categories

Parent category: Financial