Form 706 - United States Estate (And Generation-Skipping Transfer) Tax Return Page 5

Download a blank fillable Form 706 - United States Estate (And Generation-Skipping Transfer) Tax Return in PDF format just by clicking the "DOWNLOAD PDF" button.

Open the file in any PDF-viewing software. Adobe Reader or any alternative for Windows or MacOS are required to access and complete fillable content.

Complete Form 706 - United States Estate (And Generation-Skipping Transfer) Tax Return with your personal data - all interactive fields are highlighted in places where you should type, access drop-down lists or select multiple-choice options.

Some fillable PDF-files have the option of saving the completed form that contains your own data for later use or sending it out straight away.

ADVERTISEMENT

Tax Return Printable pdf") 1

1 2

2 3

3 4

4 5

5 6

6 7

7 8

8 9

9 10

10 11

11 12

12 13

13 14

14 15

15 16

16 17

17 18

18 19

19 20

20 21

21 22

22 23

23 24

24 25

25 26

26 27

27 28

28 29

29 30

30 31

31 32

32 33

33 34

34 35

35 36

36 37

37 38

38 39

39 40

40 41

41 42

42 43

43 44

44 45

45 46

46Form 706 (Rev. 11-01)

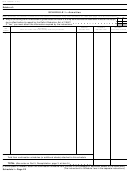

Instructions for Schedule A—Real Estate

If the decedent’s estate is NOT liable for the amount of

the mortgage, report only the value of the equity of

If the total gross estate contains any real estate, you must

redemption (or value of the property less the

complete Schedule A and file it with the return. On

indebtedness) in the value column as part of the gross

Schedule A list real estate the decedent owned or had

estate. Do not enter any amount less than zero. Do not

contracted to purchase. Number each parcel in the

deduct the amount of indebtedness on Schedule K.

left-hand column.

Also list on Schedule A real property the decedent

Describe the real estate in enough detail so that the

contracted to purchase. Report the full value of the

IRS can easily locate it for inspection and valuation. For

property and not the equity in the value column. Deduct

each parcel of real estate, report the area and, if the

the unpaid part of the purchase price on Schedule K.

parcel is improved, describe the improvements. For city or

Report the value of real estate without reducing it for

town property, report the street and number, ward,

homestead or other exemption, or the value of dower,

subdivision, block and lot, etc. For rural property, report

curtesy, or a statutory estate created instead of dower or

the township, range, landmarks, etc.

curtesy.

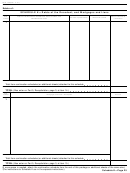

If any item of real estate is subject to a mortgage for

Explain how the reported values were determined and

which the decedent’s estate is liable; that is, if the

attach copies of any appraisals.

indebtedness may be charged against other property of

the estate that is not subject to that mortgage, or if the

decedent was personally liable for that mortgage, you

must report the full value of the property in the value

column. Enter the amount of the mortgage under

“Description” on this schedule. The unpaid amount of the

mortgage may be deducted on Schedule K.

Schedule A Examples

In this example, alternate valuation is not adopted; the date of death is January 1, 2001.

Item

Alternate

Alternate

Value at

Description

number

valuation date

value

date of death

1

House and lot, 1921 William Street NW, Washington, DC (lot 6, square 481). Rent

of $2,700 due at end of each quarter, February 1, May 1, August 1, and November

1. Value based on appraisal, copy of which is attached

$108,000

Rent due on item 1 for quarter ending November 1, 2000, but not collected at date

of death

2,700

Rent accrued on item 1 for November and December 2000

1,800

2

House and lot, 304 Jefferson Street, Alexandria, VA (lot 18, square 40). Rent of $600

payable monthly. Value based on appraisal, copy of which is attached

96,000

Rent due on item 2 for December 2000, but not collected at date of death

600

In this example, alternate valuation is adopted; the date of death is January 1, 2001.

Item

Alternate

Alternate

Value at

Description

number

valuation date

value

date of death

1

House and lot, 1921 William Street NW, Washington, DC (lot 6, square 481). Rent

of $2,700 due at end of each quarter, February 1, May 1, August 1, and

November 1. Value based on appraisal, copy of which is attached. Not disposed of

within 6 months following death

7/1/01

90,000

$108,000

Rent due on item 1 for quarter ending November 1, 2000, but not collected until

February 1, 2001

2/1/01

2,700

2,700

Rent accrued on item 1 for November and December 2000, collected on

February 1, 2001

2/1/01

1,800

1,800

2

House and lot, 304 Jefferson Street, Alexandria, VA (lot 18, square 40). Rent of $600

payable monthly. Value based on appraisal, copy of which is attached. Property

exchanged for farm on May 1, 2001

5/1/01

90,000

96,000

Rent due on item 2 for December 2000, but not collected until February 1, 2001

2/1/01

600

600

Schedule A—Page 5

ADVERTISEMENT

0 votes

Related Articles

Related forms

Tax Return")

Tax Return")

Tax Return")

Tax Return")

Tax Return")

Tax Return")

Tax Return - 2011") Instructions For Form 706 - United States Estate (and Generation-skipping Transfer) Tax Return - 2011

Financial

Instructions For Form 706 - United States Estate (and Generation-skipping Transfer) Tax Return - 2011

Financial

Tax Return - 2008") Instructions For Form 706 - United States Estate (and Generation-skipping Transfer) Tax Return - 2008

Financial

Instructions For Form 706 - United States Estate (and Generation-skipping Transfer) Tax Return - 2008

Financial

Tax Return - 2005")

Tax Return")

Related Categories

Parent category: Financial