Form Rev-415 As - Employer Withholding Information Guide Page 21

ADVERTISEMENT

1

1 2

2 3

3 4

4 5

5 6

6 7

7 8

8 9

9 10

10 11

11 12

12 13

13 14

14 15

15 16

16 17

17 18

18 19

19 20

20 21

21 22

22 23

23 24

24All W-2 forms must be submitted to the PA Department of

Revenue by Jan. 31 following the year of compensation, or

30 days from the termination of business, if the business

terminated during the calendar year. An employee whose

employment is terminated before the close of a calendar

year may request, in writing, the employer to furnish him

a W-2 form at an earlier time. If there is no reasonable

expectation on the part of both employer and employee of

further employment during the calendar year, then the

employer shall furnish the W-2 form to the employee on or

before the 30th day after the date of the request, or the 30th

day after the date on which the last payment of wages is

made, whichever is later.

Any employer who willfully furnishes a false or fraudulent W-2

form, willfully fails to furnish a statement in the prescribed

manner or time or fails to show the information required is

liable for a penalty of $50 for each failure.

1099 FILING REQUIREMENTS

Record-Keeping for Over-collections

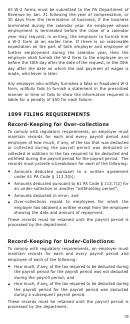

To comply with regulatory requirements, an employer must

maintain records for each and every payroll period and

employee of how much, if any, of the tax that was deducted

or collected during the payroll period was deducted or

collected in addition to the tax required to be deducted and

withheld during the payroll period for the payroll period. The

records must provide a breakdown for each of the following:

•

Amounts deducted pursuant to a written agreement

under 61 PA Code § 113.3(b);

•

Amounts deducted pursuant to 61 PA Code § 113.7(2) for

an under-collection in another “withholding period”;

•

Amounts deducted in error; and

•

Over-collections repaid to employees for which the

employer has obtained a written receipt from the employee

showing the date and amount of repayment.

These records must be retained until the payroll period is

processed by the department.

Record-Keeping for Under-Collections:

To comply with regulatory requirements, an employer must

maintain records for each and every payroll period and

employee of each of the following:

•

How much, if any, of the tax required to be deducted during

the payroll period for the payroll period was not deducted

during the payroll period; and

•

How much, if any, of the tax required to be deducted during

the payroll period for the payroll period was deducted

during a subsequent payroll period.

These records must be retained until the payroll period is

processed by the department.

19

ADVERTISEMENT

0 votes

Related Articles

Related forms

Form Rev-20 As - Employer Withholding For Pennsylvania Taxable Compensation Guide - Directions For Completing Federal Form W-2 Block 16

Financial

Form Rev-20 As - Employer Withholding For Pennsylvania Taxable Compensation Guide - Directions For Completing Federal Form W-2 Block 16

Financial

Form Rev-1716 As - Period Ending And Administrative Due Dates For The Remittance Of Employer Withholding And Filing Of Quarterly Returns And W-2 Forms - 2012

Financial

Form Rev-1716 As - Period Ending And Administrative Due Dates For The Remittance Of Employer Withholding And Filing Of Quarterly Returns And W-2 Forms - 2012

Financial

Form Rev-1716 As - Period Ending And Administrative Due Dates For The Remittance Of Employer Withholding And Filing Of Quarterly Returns And W-2 Forms - 2013

Financial

Form Rev-1716 As - Period Ending And Administrative Due Dates For The Remittance Of Employer Withholding And Filing Of Quarterly Returns And W-2 Forms - 2013

Financial

")

Related Categories

Parent category: Financial