Form Nc-30 - Income Tax Withholding Tables And Instructions For Employers - North Carolina - 2017 Page 10

ADVERTISEMENT

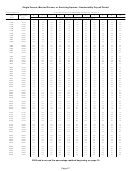

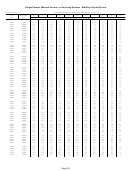

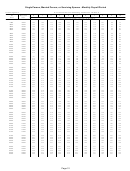

1

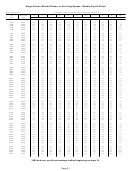

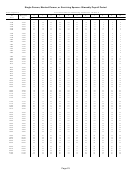

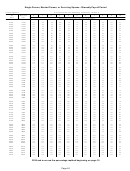

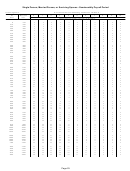

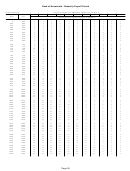

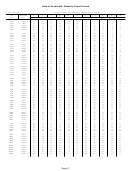

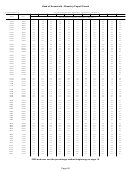

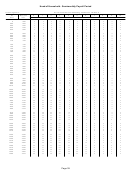

1 2

2 3

3 4

4 5

5 6

6 7

7 8

8 9

9 10

10 11

11 12

12 13

13 14

14 15

15 16

16 17

17 18

18 19

19 20

20 21

21 22

22 23

23 24

24 25

25 26

26 27

27 28

28 29

29 30

30 31

31 32

32 33

33 34

34 35

35 36

36 37

37 38

38 39

39 40

40 41

41 42

42 43

43 44

44 45

45 46

46Vacation pay is subject to withholding as if it were

Nonresident Alien Employee’s Withholding

a regular wage payment. If vacation pay is paid in

Allowance Certificate, Form NC-4 NRA. Because

addition to the regular wages, treat the vacation pay

nonresident aliens are generally not allowed a

as supplemental wages. If vacation pay is for a time

standard deduction, nonresident alien employees must

longer than your usual payroll period, spread it over the

complete and sign a North Carolina Nonresident Alien

pay periods for which you pay it.

Employee’s Withholding Allowance Certificate, Form

NC-4 NRA. You must withhold tax using the “Single”

See Federal Publication 15, Employer’s Tax

filing status regardless of the employee’s actual marital

Guide, for additional information on supplemental wages.

status. If an employee does not give you a completed

NC-4 NRA, you must withhold as single with zero

Tips treated as supplemental wages. Withhold

allowances and also withhold the additional tax as

the income tax on tips from wages or from funds the

directed below.

employee makes available. If an employee receives

regular wages and reports tips, figure income tax as if the

Form NC-4 NRA requires the nonresident alien

tips were supplemental wages. If you have not withheld

employee to enter on line 2 an additional amount of

income tax from the regular wages, add the tips to the

Income tax to be withheld for each pay period to account

regular wages and withhold income tax on the total. If

for the inclusion of the standard deduction in the wage

you withheld income tax from the regular wages, you

bracket tables, percentage, and annualized methods

can withhold on the tips by method (a) or (b).

of computing income tax withheld. The additional tax

to withhold per pay period is identified in the following

14� Employee’s Withholding Allowance

chart and represents the income tax on the standard

Certificate, Form NC-4, Form NC-4

deduction for the single filing status ($8,750) divided

EZ, and Form NC-4 NRA

by the number of payroll periods during the year. For

example, an employee paid monthly is required to enter

Each new employee must complete and sign a

$41 ($8,750 X 5.599% ÷ 12).

North Carolina Employee’s Withholding Allowance

Certificate, Form NC-4, Form NC-4 EZ, or Form NC-4

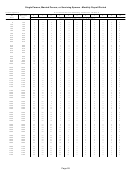

Payroll

Weekly

Biweekly

Semimonthly

Monthly

NRA. If an employee does not give you a completed

Period

Form NC-4, Form NC-4 EZ, or Form NC-4 NRA, you

must withhold tax as if the employee is single with

Additional

$9

$19

$20

$41

zero withholding allowances. A certificate filed by a

Withholding

new employee is effective upon the first payment of

wages thereafter and remains in effect until a new one is

The additional withholding results in overwithholding

furnished unless the employee claimed total exemption

in two instances – (1) employees who earn less than

from withholding during the prior year. Important:

$8,750 per year, and (2) employees who are students or

A military spouse who claims exemption from

business apprentices and residents of India. To prevent

withholding under the Military Spouses Residency

overwithholding in the first instance, an employer should

Relief Act must submit a new Form NC-4 EZ each

limit the additional withholding to the lesser of the

year� The military spouse must attach a copy of

amount reported by the employee on line 2 or 5.599% of

their spousal military identification card and a copy

the wages for that period if the amount of wages for that

of the servicemember’s most recent leave and

period multiplied by the number of payroll periods during

earnings statement� The military spouse must also

the year is $8,750 or less. The following chart lists the

submit a new NC-4 EZ immediately upon determining

wages per period that qualify for the 5.599% limitation.

that the spouse no longer meets the requirements

Wages exceeding the amounts in the chart are subject

for the exemption. State and federal definitions of

to the entire amount of additional withholding.

dependent, single person, married, head of household

and qualifying widow(er) are the same; however, the

Payroll Period

Additional withholding

number of allowances to which an individual is entitled

from line 2 limited to

will differ. Federal Withholding Allowance Certificates

5.599% of the amount

are not acceptable.

of wages if wages do not

exceed:

You are not required to determine whether the total

Weekly

$168

amount of allowances claimed is greater than the total

amount to which the employee is entitled. However,

Biweekly

$336

you should immediately advise the Department if you

Semimonthly

$364

believe that the amount of allowances claimed by an

Monthly

$729

employee is greater than the amount to which such

employee is entitled.

Page 10

ADVERTISEMENT

0 votes

Related Articles

Related forms

Form As/rp1 - Income Tax Withholding, Sales And Use Tax, Registration Application Instructions

Financial

Form As/rp1 - Income Tax Withholding, Sales And Use Tax, Registration Application Instructions

Financial

Form Nc-br - Business Registration Application For Income Tax Withholding, Sales And Use Tax, And Machinery And Equipment Tax

Life

Form Nc-br - Business Registration Application For Income Tax Withholding, Sales And Use Tax, And Machinery And Equipment Tax

Life

Form De 1p - Employers Depositing Only Personal Income Tax Withholding Registration And Update Form - 2016

Legal

Form De 1p - Employers Depositing Only Personal Income Tax Withholding Registration And Update Form - 2016

Legal

Form Mw507p - Maryland Income Tax Withholding For Annuity, Sick Pay And Retirement Distributions

Financial

Form Mw507p - Maryland Income Tax Withholding For Annuity, Sick Pay And Retirement Distributions

Financial

Related Categories

Parent category: Financial