Form Nc-30 - Income Tax Withholding Tables And Instructions For Employers - North Carolina - 2017 Page 8

ADVERTISEMENT

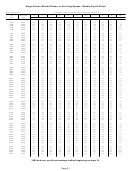

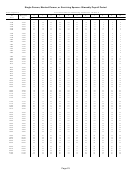

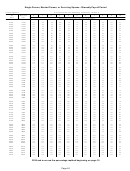

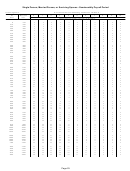

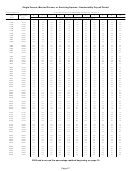

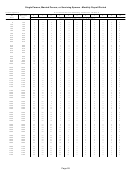

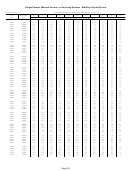

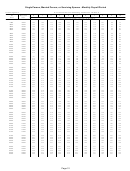

1

1 2

2 3

3 4

4 5

5 6

6 7

7 8

8 9

9 10

10 11

11 12

12 13

13 14

14 15

15 16

16 17

17 18

18 19

19 20

20 21

21 22

22 23

23 24

24 25

25 26

26 27

27 28

28 29

29 30

30 31

31 32

32 33

33 34

34 35

35 36

36 37

37 38

38 39

39 40

40 41

41 42

42 43

43 44

44 45

45 46

46calendar year. Federal Form 1099-MISC may be filed

withheld from a payment that is not compensation, or

if it is in excess of the amount required to be withheld.

in lieu of Form NC-1099-ITIN if it reflects the amount

of North Carolina income tax withheld. Form NC-1099-

ITIN must be given to the contractor by January 31

8� Withholding on Contractors

following the calendar year in which the compensation

Identified by an Individual Taxpayer

was paid. If the services are completed before the end

Identification Number (ITIN)

of the calendar year and the contractor requests the

The following definitions are applicable with respect

form, it is due within 30 days after the last payment of

to withholding on contractors identified by an ITIN:

compensation to the contractor.

(a) Compensation. Consideration a payer pays to

The Annual Withholding Reconciliation (Form

an ITIN holder who is a contractor and not an employee

NC-3) that reconciles the amount withheld from

for services performed in North Carolina.

each contractor must be filed with the Department

on or before January 31 following the year in which

(b) ITIN contractor. An ITIN holder who performs

the compensation was paid. Payers who report only

services in North Carolina for compensation other than

ITIN compensation withholding must file the annual

wages.

reconciliation report and include the withholding

statements. Payers who are subject to both wage

(c) ITIN holder. A person whose taxpayer

withholding and withholding from ITIN compensation

identification number is an Individual Taxpayer

must file one annual reconciliation report that includes

Identification Number (ITIN). An ITIN is issued by the

the two types of withholding statements.

IRS to a person who is required to have a taxpayer

identification number but does not have and is not

Amounts withheld in error. If you withhold an

eligible to obtain a social security number.

amount in error and the amount is refunded to the

contractor before the end of the calendar year and

(d) Payer. A person who, in the course of a trade or

before you give the NC-1099-ITIN to the contractor,

business, pays compensation to an ITIN holder who is a

do not report the refunded amount on the NC-1099-

contractor and not an employee for services performed

ITIN or the annual reconciliation statement. If the

in North Carolina.

amount withheld in error has already been paid to the

Department, reduce your next withholding payment

Withholding requirement. If, in the course of your

accordingly. Amounts are considered withheld in error if

trade or business, you pay compensation of more than

they are withheld from a person who is not a contractor,

$1,500 during the calendar year to an ITIN contractor,

if it is withheld from a payment that is not compensation,

you must withhold North Carolina income tax at the rate

or if it is in excess of the amount required to be withheld.

of 4 percent of the compensation paid to the contractor.

However, withholding is not required on compensation

9� Payee’s Identification Number

paid to an ITIN holder who is temporarily admitted to the

United States to perform agricultural labor or services

An individual employee or nonresident contractor

under an H-2A visa and who is not subject to federal

is identified by the individual’s social security number.

income tax withholding under section 1441 of the Code.

A contractor that is not an individual (corporation,

partnership, limited liability company) is identified by its

How and when to pay the tax withheld. If you

federal identification number. Show the payee’s social

pay compensation to an ITIN contractor and you do

security number, federal identification number and the

not already have a withholding account identification

name and address on Forms W-2 and NC-1099PS and

number, you must complete Form NC-BR. You must

use it in any correspondence pertaining to a particular

report and pay the tax withheld on a quarterly, monthly,

employee or contractor. ITIN contractors are identified

or semiweekly basis depending on the average amount

by their ITIN numbers. An ITIN number is issued by

withheld during the month. (See numbers 15, 16, and

the IRS to a person who is required to have a taxpayer

17 for determining the basis on which to file.) If you

identification number but does not have and is not

withhold from ITIN contractor compensation and wages,

eligible to obtain a social security number. Show the

you must report the withholding from ITIN contractor

payee’s ITIN number on Form NC-1099-ITIN.

compensation with the wage withholding.

10� Withholding from Wages

Form NC-1099-ITIN and annual reconciliation

requirement. If you withhold tax from an ITIN

The term wages generally has the same meaning

contractor, you must give the contractor Form NC-

as in Section 3401 of the Internal Revenue Code except

1099-ITIN, Compensation Paid to an ITIN Contractor,

that it does not include the amount an employer pays an

showing the amount of compensation paid and the

employee for reimbursement of ordinary and necessary

amount of North Carolina income tax withheld during the

business expenses of the employee. North Carolina

Page 8

ADVERTISEMENT

0 votes

Related Articles

Related forms

Form As/rp1 - Income Tax Withholding, Sales And Use Tax, Registration Application Instructions

Financial

Form As/rp1 - Income Tax Withholding, Sales And Use Tax, Registration Application Instructions

Financial

Form Nc-br - Business Registration Application For Income Tax Withholding, Sales And Use Tax, And Machinery And Equipment Tax

Life

Form Nc-br - Business Registration Application For Income Tax Withholding, Sales And Use Tax, And Machinery And Equipment Tax

Life

Form De 1p - Employers Depositing Only Personal Income Tax Withholding Registration And Update Form - 2016

Legal

Form De 1p - Employers Depositing Only Personal Income Tax Withholding Registration And Update Form - 2016

Legal

Form Mw507p - Maryland Income Tax Withholding For Annuity, Sick Pay And Retirement Distributions

Financial

Form Mw507p - Maryland Income Tax Withholding For Annuity, Sick Pay And Retirement Distributions

Financial

Related Categories

Parent category: Financial