Form Nc-30 - Income Tax Withholding Tables And Instructions For Employers - North Carolina - 2017 Page 11

ADVERTISEMENT

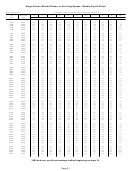

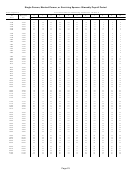

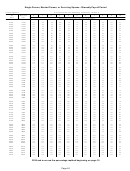

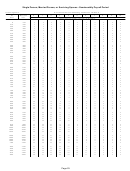

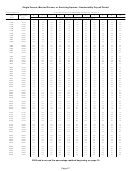

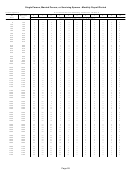

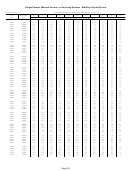

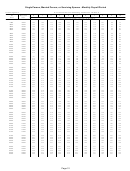

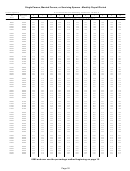

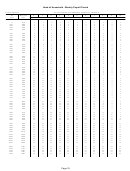

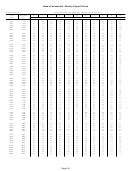

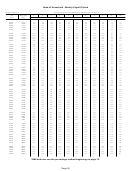

1

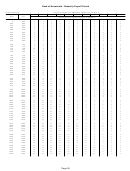

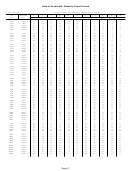

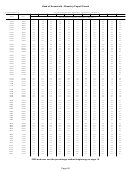

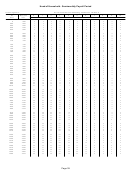

1 2

2 3

3 4

4 5

5 6

6 7

7 8

8 9

9 10

10 11

11 12

12 13

13 14

14 15

15 16

16 17

17 18

18 19

19 20

20 21

21 22

22 23

23 24

24 25

25 26

26 27

27 28

28 29

29 30

30 31

31 32

32 33

33 34

34 35

35 36

36 37

37 38

38 39

39 40

40 41

41 42

42 43

43 44

44 45

45 46

46Penalty. If an employee provides a withholding

Example: Employee is a nonresident alien and is paid

on a monthly basis. Employee earns wages of $500

allowance certificate that contains information which

in February 2017. Employee files a Form NC-4 NRA

has no reasonable basis and results in a lesser amount

claiming zero allowances on line 1 and additional

of tax being withheld than would have been withheld

withholding of $41 on line 2. According to the tax

had the employee furnished reasonable information,

tables, no withholding is due. Without the modification,

the employee is subject to a penalty of 50 percent of

Employer will withhold $41. Using the modification,

the amount not properly withheld.

Employer will withhold $28 ($500 X 5.599%).

If an employee’s withholding allowances should

To prevent overwithholding in the second instance, an

decrease, requiring more tax to be withheld, the

employee who is a student or business apprentice and

employee is required to provide an amended certificate

a resident of India should enter $0 on line 2 of Form

within 10 days after the change. If the allowance

NC-4 NRA.

increases, requiring less tax to be withheld, the

employee may provide an amended certificate any time

Wages that are exempt from U. S. income tax under an

after the change.

income tax treaty are generally exempt from withholding.

Residents of Canada and Mexico who enter or leave

Additional withholding allowances may be

the United States at frequent intervals are not subject

claimed by taxpayers expecting to have allowable

to withholding on their wages if these persons either

itemized deductions exceeding the standard deduction

(1) perform duties in transportation service between the

or allowable adjustments to income.

One additional

United States and Canada or Mexico, or (2) perform

allowance may be claimed for each $2,500 that the

duties connected to the construction, maintenance, or

itemized deductions are expected to exceed the standard

operation of water-way, viaduct, dam, or bridge crossed

deduction and for each $2,500 of adjustments reducing

by, or crossing, the boundary between the United States

income. If an employee will be entitled to a tax credit,

and Canada or the boundary between the United States

he may claim one additional allowance for each $140.

and Mexico. Nonresident aliens who are bona fide

residents of the U.S. Virgin Islands are not subject to

Additional withholding. To increase withholding,

withholding of tax on income earned while temporarily

an employee may claim fewer allowances or may enter

employed in the United States.

into an agreement with his employer and request that an

additional amount be withheld by entering the desired

Submission of certain withholding allowance

amount on line 2 of Form NC-4 or Form NC-4 EZ or

certificates. Although no longer required by the IRS,

Line 3 of Form NC-4 NRA.

North Carolina requires an employer to submit copies

of any certificates (Form NC-4, Form NC-4 EZ, or Form

15� Quarterly Returns and Payments

NC-4 NRA) on which the employee claims more than

An employer who withholds an average of less than

10 withholding allowances or claims exemption from

$250 of North Carolina income tax per month must file

withholding and the employee’s weekly wages would

a quarterly Withholding Return, Form NC-5, and pay

normally exceed an amount equal to the North Carolina

the tax quarterly. The quarterly return and payment

standard deduction for an individual with a filing status

are due by the last day of the month following the end

of single divided by 52. For tax year 2017, the weekly

of the calendar quarter.

wage amount would be $168 (standard deduction for

single individual is $8,750 divided by 52 = $168). Retain

If you temporarily cease to pay wages after you are

the original certificate in your files..

registered, you should file a return for each quarter even

though you have no withholding or wages to report.

When to submit. An employer filing quarterly

Do not report more than one calendar quarter on one

withholding reports is required to submit copies of the

return.

certificates received during the quarter at the time for

filing the quarterly report. An employer filing monthly

16� Monthly Returns and Payments

withholding reports is required to submit copies of the

certificates received during the quarter at the time

An employer who withholds an average of at least

for filing the monthly report for the third month of the

$250 but less than $2,000 of North Carolina income tax

calendar quarter. Copies may be submitted earlier and

per month must file a monthly Withholding Return, Form

for shorter reporting periods.

NC-5, and pay the tax monthly. All monthly returns and

payments are due by the 15th day of the month following

Mail the certificate to: North Carolina Department

the month in which the tax was withheld; except the

of Revenue, Tax Compliance-Withholding Tax, PO

return and payment for the month of December are due

Box 25000, Raleigh, North Carolina 27640-0001�

by January 31.

Page 11

ADVERTISEMENT

0 votes

Related Articles

Related forms

Form As/rp1 - Income Tax Withholding, Sales And Use Tax, Registration Application Instructions

Financial

Form As/rp1 - Income Tax Withholding, Sales And Use Tax, Registration Application Instructions

Financial

Form Nc-br - Business Registration Application For Income Tax Withholding, Sales And Use Tax, And Machinery And Equipment Tax

Life

Form Nc-br - Business Registration Application For Income Tax Withholding, Sales And Use Tax, And Machinery And Equipment Tax

Life

Form De 1p - Employers Depositing Only Personal Income Tax Withholding Registration And Update Form - 2016

Legal

Form De 1p - Employers Depositing Only Personal Income Tax Withholding Registration And Update Form - 2016

Legal

Form Mw507p - Maryland Income Tax Withholding For Annuity, Sick Pay And Retirement Distributions

Financial

Form Mw507p - Maryland Income Tax Withholding For Annuity, Sick Pay And Retirement Distributions

Financial

Related Categories

Parent category: Financial