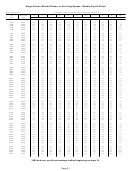

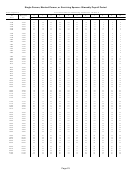

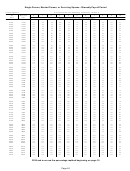

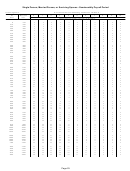

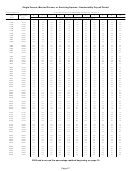

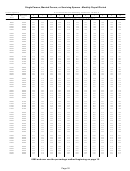

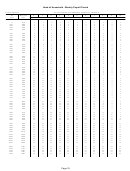

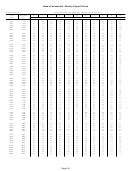

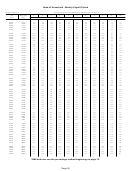

Form Nc-30 - Income Tax Withholding Tables And Instructions For Employers - North Carolina - 2017 Page 5

ADVERTISEMENT

1

1 2

2 3

3 4

4 5

5 6

6 7

7 8

8 9

9 10

10 11

11 12

12 13

13 14

14 15

15 16

16 17

17 18

18 19

19 20

20 21

21 22

22 23

23 24

24 25

25 26

26 27

27 28

28 29

29 30

30 31

31 32

32 33

33 34

34 35

35 36

36 37

37 38

38 39

39 40

40 41

41 42

42 43

43 44

44 45

45 46

46Pension payment – A periodic payment or a nonperiodic

Except for eligible rollovers, a recipient of a pension

distribution, as those terms are

payment who has federal income tax withheld can elect

defined in section 3405 of the Code.

not to have State income tax withheld. Conversely, a

recipient who has State income tax withheld can elect

Withholding Required.

A pension payer

not to have federal income tax withheld.

required to withhold federal tax under section 3405 of

An election not to have tax withheld from a pension

the Code on a pension payment to a North Carolina

payment remains in effect until revoked by the recipient.

resident must also withhold State income tax from the

An election not to have tax withheld is void if the recipient

pension payment. If a payee has provided a North

does not furnish the recipient’s tax identification number

Carolina address to a pension payer, the payee is

to the payer or furnishes an incorrect identification

presumed to be a North Carolina resident and the

number.

In such cases, the payer will withhold on

payer is required to withhold State tax unless the

periodic payments as if the recipient is single claiming

payee elects no withholding. A pension payer that

zero allowances and on nonperiodic distributions at the

either fails to withhold or to remit tax that is withheld

rate of 4 percent.

is liable for the tax.

A nonresident with a North Carolina address should

A pension payer must treat a pension payment paid

also use Form NC-4P to elect not to have State income

to an individual as if it were an employer’s payment of

tax withheld. Completing Form NC-4P and electing not

wages to an employee. If the pension payer has more

to have State tax withheld does not necessarily mean

than one arrangement under which distributions may

that the recipient is a resident of North Carolina.

be made to an individual, each arrangement must be

treated separately.

Exceptions to Withholding. Tax is not required

to be withheld from the following pension payments:

Amount to Withhold. In the case of a periodic

payment, as defined in Code section 3405(e)(2),

(1) A pension payment that is wages.

the payer must withhold as if the recipient were

(2) Any portion of a pension payment that meets both

a single person with zero allowances unless the

of the following conditions:

recipient provides an allowance certificate (Form

a. It is not a distribution or payment from an

NC-4P) reflecting a different filing status or number of

individual retirement plan as defined in section

allowances. Form NC-4P, Withholding Certificate for

7701 of the Code.

Pension or Annuity Payments, is used by a recipient of

b. The pension payer reasonably believes it is not

pension payments who is a North Carolina resident to

taxable to the recipient.

report the correct filing status, number of allowances,

(3) A distribution described in section 404(k)(2) of the

and any additional amount the recipient wants withheld

Code, relating to dividends on corporate securities.

from the pension payment. It may also be used to elect

(4) A pension payment that consists only of securities

not to have State income tax withheld. In lieu of Form

of the recipient’s employer corporation plus cash

NC-4P, payers may use a substitute form if it contains

not in excess of $200 in lieu of securities of the

all the provisions included on Form NC-4P.

employer corporation.

(5) Distributions of retirement benefits received

For a nonperiodic distribution, as defined in Code

from North Carolina State and local government

section 3405(e)(3), four percent (4%) of the distribution

retirement systems and federal retirement systems

must be withheld. A nonperiodic distribution includes an

identified as qualifying retirement systems under

eligible rollover distribution as defined in Code section

the terms of the Bailey/Emory/Patton settlement

3405(c)(3). State law differs from federal law with

that are paid to retirees who were vested in the

respect to eligible rollover distributions. Federal law

retirement systems as of August 12, 1989.

imposes a higher rate of withholding on eligible rollover

distributions than on other nonperiodic distributions.

Notification Procedures for Pension Payers.

State law imposes the same rate of withholding on all

A pension payer is required to provide each recipient

nonperiodic distributions.

with notice of the right not to have State withholding

apply and of the right to revoke the election. The notice

Election Not to Have Income Tax Withheld. A

requirements for North Carolina purposes are the same

recipient may elect not to have income tax withheld from

as the federal notice requirements, which are provided

a pension payment unless the pension payment is an

in section 3405(e)(10) of the Code. Section D of Federal

eligible rollover distribution.

A recipient of a pension

Regulation 35.3405-1 contains sample notices that may

payment that is an eligible rollover distribution does

be modified for State purposes to satisfy the notice

not have the option of electing not to have State tax

and election requirements for periodic payments and

withheld from the distribution.

nonperiodic distributions.

Page 5

ADVERTISEMENT

0 votes

Related Articles

Related forms

Form As/rp1 - Income Tax Withholding, Sales And Use Tax, Registration Application Instructions

Financial

Form As/rp1 - Income Tax Withholding, Sales And Use Tax, Registration Application Instructions

Financial

Form Nc-br - Business Registration Application For Income Tax Withholding, Sales And Use Tax, And Machinery And Equipment Tax

Life

Form Nc-br - Business Registration Application For Income Tax Withholding, Sales And Use Tax, And Machinery And Equipment Tax

Life

Form De 1p - Employers Depositing Only Personal Income Tax Withholding Registration And Update Form - 2016

Legal

Form De 1p - Employers Depositing Only Personal Income Tax Withholding Registration And Update Form - 2016

Legal

Form Mw507p - Maryland Income Tax Withholding For Annuity, Sick Pay And Retirement Distributions

Financial

Form Mw507p - Maryland Income Tax Withholding For Annuity, Sick Pay And Retirement Distributions

Financial

Related Categories

Parent category: Financial