Form Wv/bcs-1 - Business Investment And Jobs Expansion Credit And Corporate Headquarters Relocation Credit (Super Credits) - Page 6

ADVERTISEMENT

- Printable pdf") 1

1 2

2 3

3 4

4 5

5 6

6 7

7 8

8 9

9 10

10 11

11 12

12 13

13 14

14 15

15 16

16 17

17 18

18 19

19 20

20 21

21 22

22 23

23 24

24 25

25 26

26 27

27 28

28 29

29 30

30applicable to all Super Credits except the Corporate Headquarters Relocation Credit.)

A job is attributable to the qualified investment if:

1.

The employee’s service is performed or his base of operations is at the new or expanded facility; and

2.

The position did not exist prior to the making of the investment in the new or expanded facility; and

3.

The position exists only because of the investment in the new or expanded facility.

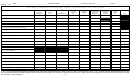

CALCULATION OF FULL-TIME EQUIVALENT EMPLOYEES

The hours of qualified part-time employees are aggregated to determine the number of equivalent full-time

employees for the purpose of determining the applicable new jobs percentage. However, they may not be

aggregated for the purpose of determining when a job is attributable to the qualified investment.

Part-time employment qualifies if the employee works at least 20 hours per week for at least 6 months or 520 hours

per year (26 weeks @ 20 hours per week). Full-time employment is 140 hours per month or 1,680 hours per year

(140 hours times 12 months). However for investments in place prior to March 10, 1990 full-time employment is 120

hours per month or 1,440 hours per year (120 hours times 12 months).

Qualified

Full-Time

Net Full-Time

Employees

Equivalent

Equivalent

200 @ < 520 hrs

1,680

Do Not Qualify *

50 @

750 hrs

1,680

=

22.32

20 @ 1,500 hrs

1,680

=

17.86

6 @ 1,700 hrs

1,680**

=

6.00

4 @ 2,080 hrs

1,680***

=

4.00

Total Net Full-Time Equivalent Employees

=

50.18

*

Must work for at least 6 months at 20 or more hours per week to qualify

**

These employees work at least 20 hours per week for at least 6 months during the year.

***

.

Hours beyond 1,680 (1,440 for projects in place prior to 1990) may not be counted as additional employees

REQUIRED EMPLOYMENT RECORDS

The taxpayer must maintain records to establish the following:

1.

Total full-time equivalent employment in place during the year immediately preceding the year qualified

investment was first placed into service or use.

2.

Total full-time equivalent employment in place during each year of the project.

Such records must be retained for a period of three years after the last year for which the credit is claimed.

REDETERMINATION, FORFEITURE, AND RECAPTURE OF CREDIT

If during any taxable year, property used as a qualified investment for any of these credits is disposed of prior

to the end of its useful life or ceases to be used in an eligible business, the unused portion of the credit attributable

to that investment is forfeited for the taxable year and all ensuing years. Forfeiture also applies if the taxpayer ceases

operation of a business facility for which credit was allowed before expiration of the useful life of the qualified

investment property. The failure to create or maintain the necessary number of new jobs for credit entitlement also

results in credit forfeiture.

REDETERMINATION IS REQUIRED FOR:

1.

Failure to create the minimum number of new jobs within the required two to three year period: The

entire credit is forfeited. Any Credit claimed during the first three years must be paid back (recaptured) with

interest and a ten percent penalty.

6

ADVERTISEMENT

0 votes

Related Articles

Related forms

Form Wv/bcs-1 - West Virginia Business Investment And Jobs Expansion Tax Credit Or Corporate Headquarters Relocation Credit

Financial

Form Wv/bcs-1 - West Virginia Business Investment And Jobs Expansion Tax Credit Or Corporate Headquarters Relocation Credit

Financial

Form Wv/bcs-1 - West Virginia Business Investment And Jobs Expansion Tax Credit Or Corporate Headquarters Relocation Credit

Financial

Form Wv/bcs-1 - West Virginia Business Investment And Jobs Expansion Tax Credit Or Corporate Headquarters Relocation Credit

Financial

Form Wv/ngret-1 - Schedule For Application Of Tax Credit From "natural Gas Jobs Retention Act"

Financial

Form Wv/ngret-1 - Schedule For Application Of Tax Credit From "natural Gas Jobs Retention Act"

Financial

Form Wv/ngret-1 - Schedule For Application Of Tax Credit From "natural Gas Jobs Retention Act"

Financial

Form Wv/ngret-1 - Schedule For Application Of Tax Credit From "natural Gas Jobs Retention Act"

Financial

Sch. Bcs-pit - Business Investment And Jobs Expansion Credit Claims Against Personal Income Tax

Financial

Sch. Bcs-pit - Business Investment And Jobs Expansion Credit Claims Against Personal Income Tax

Financial

Schedule Bcs-pit - Business Investment And Jobs Expansion Credit Claims Against Personal Income Tax

Financial

Schedule Bcs-pit - Business Investment And Jobs Expansion Credit Claims Against Personal Income Tax

Financial

Related Categories

Parent category: Financial