Form Mo-1040 - Booklet Missouri Individual Income Tax Long Form - 2011 Page 34

ADVERTISEMENT

1

1 2

2 3

3 4

4 5

5 6

6 7

7 8

8 9

9 10

10 11

11 12

12 13

13 14

14 15

15 16

16 17

17 18

18 19

19 20

20 21

21 22

22 23

23 24

24 25

25 26

26 27

27 28

28 29

29 30

30 31

31 32

32 33

33 34

34 35

35 36

36 37

37 38

38 39

39 40

40 41

41 42

42 43

43 44

44Form MO-2210

Page 4

Line-by-Line Instructions

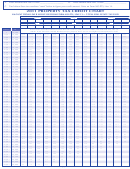

Complete Lines 15 through 19d for each installment period, then complete Lines 25 through 29.

14. Enter the required annual payment, as computed on Part

25. If you have an underpayment for the installment period

I, Line 6.

and none of the exceptions on Lines 20 through 24

apply, enter on Line 25 the amount of the underpay-

15. Divide the required annual payment (Line 14) by the

ment on Line 19d. If you do not have an underpay-

number of required installments. If the estimated tax

ment, or if an exception applies, leave this blank and

was the result of a change in income or exemptions

skip the remaining lines of the column.

during the year, you may require fewer installments.

Other wise, divide the required annual payment by four

26. Enter the date a payment was made on the install-

and place the amount in each column. (See instructions

ment, the due date of the following installment, or April

for farmers.)

15, 2012, whichever is earlier. If more than one late

payment was made to cover the installment, attach

16. Enter the amount of tax paid during the installment

a separate computation for each payment during the

period. (The tax withheld throughout the year may be

installment period.

considered as paid in four equal parts on the due date of

the installment, unless a different date is established.)

27a. Enter the number of days from the due date of the

installment to the date entered on Line 26.

17. Enter the amount, if any, of overpayment reported on

Line 19c from the previous installment period.

27b. Enter the number of days from January 1, 2012 (or a

later date, if the installment date was after January 1)

18. Enter the sum of Line 16 and Line 17.

until either the date of the payment or April 15, 2012,

whichever is earlier.

19. If the amount on Line 15 is greater than the amount on

Line 18, enter the difference here. You have underpaid

28a. Multiply the amount on Line 25 by the number of

for the installment period. If not, skip this line and go to

days on Line 27a. Divide this amount by 365 days

Line 19a.

and multiply the product by three percent. This is the

penalty accruing on the underpayment during 2011.

19a. If the amount on Line 18 is greater than the amount on

Line 15, enter the difference here. You have overpaid

28b. Multiply the amount on Line 25 by the number of

for the installment period.

days on Line 27b. Divide this amount by 366 days

and multiply the product by three percent. This is the

19b. Enter the amount of the underpayment (if any) from Line

penalty accruing on the underpayment during 2012.

19d of the previous column.

28c. Add the amounts on Lines 28a and 28b.

19c. and 19d.

If you filled in Line 19 of this column, add the amount on

29. Add the sum of the amounts on Line 28c in the final

Line 19b to the amount on Line 19 and enter that total on

column, if applicable.

Line 19d. If you filled in Line 19a of this column, and the

amount on Line 19a is greater than any amount on Line

19b, enter the difference on Line 19c. You are overpaid.

If the amount on Line 19b is greater than the amount on

Line 19a, enter the difference on Line 19d. You are

underpaid. See page 3 for instructions for Lines 20

through 24.

Federal Privacy Notice

The Federal Privacy Act requires the Missouri Department of Revenue (Department) to inform taxpayers of the Department’s legal authority for requesting identifying informa-

tion, including social security numbers, and to explain why the information is needed and how the information will be used.

Chapter 143 of the Missouri Revised Statutes authorizes the Department to request information necessary to carry out the tax laws of the state of Missouri. Federal law 42

U.S.C. Section 405 (c)(2)(C) authorizes the states to require taxpayers to provide social security numbers.

The Department uses your social security number to identify you and process your tax returns and other documents, to determine and collect the correct amount of tax, to

ensure you are complying with the tax laws, and to exchange tax information with the Internal Revenue Service, other states, and the Multistate Tax Commission (Chapters 32

and 143, RSMo). In addition, statutorily provided non-tax uses are: (1) to provide information to the Department of Higher Education with respect to applicants for financial

assistance under Chapter 173, RSMo and (2) to offset refunds against amounts due to a state agency by a person or entity (Chapter 143, RSMo). Information furnished to other

agencies or persons shall be used solely for the purpose of administering tax laws or the specific laws administered by the person having the statutory right to obtain it [as

indicated above]. In addition, information may be disclosed to the public regarding the name of a tax credit recipient and the amount issued to such recipient (Chapter 135,

RSMo). (For the Department’s authority to prescribe forms and to require furnishing of social security numbers, see Chapters 135, 143, and 144, RSMo.)

You are required to provide your social security number on your tax return. Failure to provide your social security number or providing a false social security number may

result in criminal action against you.

MO 860-1101 (12-2011)

34

ADVERTISEMENT

0 votes

Related Articles

Related forms

- Short Form - 2011") Form Mo-1040a - Missouri Individual Income Tax Return Single/married (income From One Spouse) - Short Form - 2011

Financial

Form Mo-1040a - Missouri Individual Income Tax Return Single/married (income From One Spouse) - Short Form - 2011

Financial

Form Mo-1040p - Missouri Individual Income Tax Return And Property Tax Credit Claim/pension Exemption - Short Form - 2011

Financial

Form Mo-1040p - Missouri Individual Income Tax Return And Property Tax Credit Claim/pension Exemption - Short Form - 2011

Financial

Form Mo-1120 - Missouri Corporation Income Tax Return For 2011/missouri Corporation Franchise Tax Return For 2012

Financial

Form Mo-1120 - Missouri Corporation Income Tax Return For 2011/missouri Corporation Franchise Tax Return For 2012

Financial

- 2005")

Form Mo-1040p - Missouri Individual Income Tax Return And Property Tax Credit Claim/pension Exemption - Short Form - 2006

Financial

Form Mo-1040p - Missouri Individual Income Tax Return And Property Tax Credit Claim/pension Exemption - Short Form - 2006

Financial

2012")

Related Categories

Parent category: Financial