Publication 505 - Tax Withholding And Estimated Tax Page 11

ADVERTISEMENT

1

1 2

2 3

3 4

4 5

5 6

6 7

7 8

8 9

9 10

10 11

11 12

12 13

13 14

14 15

15 16

16 17

17 18

18 19

19 20

20 21

21 22

22 23

23 24

24 25

25 26

26 27

27 28

28 29

29 30

30 31

31 32

32 33

33 34

34 35

35 36

36 37

37 38

38 39

39 40

40 41

41 42

42 43

43 44

44 45

45 46

46 47

47 48

48 49

49•

You will owe additional amounts with your

The IRS may ask you for information show-

Example 1.4. You are a high school student

return, such as self-employment tax.

ing how you figured either the number of al-

and expect to earn $2,500 from a summer job.

lowances you claimed or your eligibility for

•

You do not expect to have any other income

Your withholding is based on obsolete

exemption from withholding. If you choose, you

during the year, and your parents will be able to

Form W – 4 information for a substantial

can give this information to your employer to

claim an exemption for you on their tax return.

part of the year.

send to the IRS along with your Form W – 4.

You worked last summer and had $375 federal

•

Your earnings are more than $125,000 if

If the IRS determines that you cannot take all

income tax withheld from your pay. The entire

you are single or $175,000 if you are mar-

the allowances claimed on your Form W – 4, or

$375 was refunded when you filed your 2001

ried.

that you are not exempt as claimed, it will inform

return. Using Figure A, you find that you can

both you and your employer and will specify the

claim exemption from withholding.

To make sure you are getting the right amount

maximum number of allowances you can claim.

of tax withheld, get Publication 919. It will help

The IRS also may ask you to fill out a new Form

Example 1.5. The facts are the same as in

you compare the total tax to be withheld during

W – 4. However, your employer cannot figure

Example 1.4, except that you have a savings

the year with the tax you can expect to figure on

your withholding on the basis of more al-

account and expect to have $320 interest in-

your return. It also will help you determine how

lowances than the maximum number deter-

come during the year. Using Figure A, you find

much, if any, additional withholding is needed

mined by the IRS.

that you cannot claim exemption from withhold-

each payday to avoid owing tax when you file

If you believe you are exempt or can claim

ing because your unearned income will be more

your return. If you do not have enough tax with-

more withholding allowances than determined

than $250 and your total income will be more

held, you may have to make estimated tax pay-

by the IRS, you can complete a new Form W – 4,

than $750.

ments. See chapter 2 for information about

stating on the form, or in a written statement, any

estimated tax.

You may have to file a tax return, even

circumstances that have changed or any other

!

if you are exempt from withholding.

reasons for your claim. You can send it directly

Rules Your Employer

See Publication 501, Exemptions,

CAUTION

to the IRS or give it to your employer to send to

Standard Deduction, and Filing Information, to

Must Follow

the IRS. Your employer must continue to figure

see whether you must file a return.

your withholding on the basis of the number of

It may be helpful for you to know some of the

allowances previously determined by the IRS

Age 65 or older or blind. If you are 65

withholding rules your employer must follow.

until the IRS advises your employer to withhold

or older or blind, use one of the follow-

These rules can affect how to fill out your Form

on the basis of the new Form W – 4.

ing worksheets to help you decide

W – 4 and how to handle problems that may

There is a penalty for supplying false infor-

whether you can claim exemption from withhold-

arise.

mation on Form W – 4. See Penalties, later.

ing. Do not use either worksheet if you will item-

New Form W – 4. When you start a new job,

ize deductions or claim exemptions for

Social security (FICA) tax. Generally, each

your employer should give you a Form W – 4 to

dependents or claim tax credits on your 2002

employer for whom you work during the tax year

fill out. Your employer will use the information

return — instead, see Itemizing deductions or

must withhold social security tax up to the an-

you give on the form to figure your withholding

claiming exemptions or credits, following the

nual limit.

beginning with your first payday.

worksheets.

If you later fill out a new Form W – 4, your

Exemption From Withholding

employer can put it into effect as soon as possi-

Worksheet 1.3

Exemption From Withholding Worksheet

ble. The deadline for putting it into effect is the

for 65 or Older or Blind

If you claim exemption from withholding, your

start of the first payroll period ending 30 or more

employer will not withhold federal income tax

days after you turn it in.

Use this worksheet only if, for 2001, you had a right to a refund

from your wages. The exemption applies only to

of all federal income tax withheld because you had no tax

No Form W – 4. If you do not give your em-

liability.

income tax, not to social security or Medicare

ployer a completed Form W – 4, your employer

Caution. This worksheet does not apply if you can be claimed

tax.

as a dependent. See Worksheet 1.4 instead.

must withhold at the highest rate — as if you

You can claim exemption from withholding

were single and claimed no allowances.

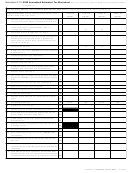

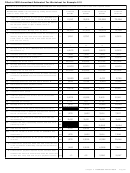

1. Check the boxes below that apply to you.

for 2002 only if both the following situations

apply.

65 or older

Blind

Repaying withheld tax. If you find you are

having too much tax withheld because you did

1) For 2001 you had a right to a refund of all

2. Check the boxes below that apply to your spouse if

not claim all the withholding allowances you are

federal income tax withheld because you

you will claim your spouse’s exemption on your 2002

entitled to, you should give your employer a new

return.

had no tax liability.

Form W – 4. Your employer cannot repay any of

65 or older

Blind

the tax previously withheld.

2) For 2002 you expect a refund of all federal

However, if your employer has withheld

income tax withheld because you expect

more than the correct amount of tax for the Form

3. Add the number of boxes you checked in

to have no tax liability.

1 and 2 above. Enter the result . . . . . . .

W – 4 you have in effect, you do not have to fill

Use Figure A, later in this chapter, to help

out a new Form W – 4 to have your withholding

you decide whether you can claim exemption

You can claim exemption from withholding if:

lowered to the correct amount. Your employer

from withholding. Do not use Figure A if you:

can repay the amount that was incorrectly with-

Your filing

and the

and your

status is:

number

2002

held. If you are not repaid, your Form W – 2 will

•

Are 65 or older,

on line 3

total

reflect the full amount actually withheld.

•

above is:

income

Are blind,

will be

Sending your Form W – 4 to the IRS. Your

•

no more

Will itemize deductions on your 2002 re-

employer will usually keep your Form W – 4 and

than:

turn.

use it to figure your withholding. Under normal

•

circumstances, it will not be sent to the IRS.

Will claim an exemption for a dependent

Single

1

$ 8,850

However, your employer must send a copy of

2

10,000

on your 2002 return.

your Form W – 4 to the IRS for verification in both

•

Will claim any tax credits on your 2002

of the following situations.

Head of

1

$11,050

return.

household

2

12,200

1) You claim more than 10 withholding al-

These situations are discussed later.

lowances.

Married filing

1

$ 7,825

separately for

2

8,725

2) You claim exemption from withholding and

Student. If you are a student, you are not

both 2001

3

9,625

your wages are expected to usually be

automatically exempt. If you work only part time

and 2002

4

10,525

more than $200 a week. See Exemption

or during the summer, you may qualify for ex-

From Withholding, later.

emption from withholding.

Other married

1

$14,750*

Chapter 1 Tax Withholding for 2002

Page 11

ADVERTISEMENT

0 votes

Related Articles

Related forms

Plans) For Employees Of Public Schools And Certain Tax-exempt Organizations") Publication 571 - Tax-sheltered Annuity Plans (403(b) Plans) For Employees Of Public Schools And Certain Tax-exempt Organizations

Financial

Publication 571 - Tax-sheltered Annuity Plans (403(b) Plans) For Employees Of Public Schools And Certain Tax-exempt Organizations

Financial

Publication 1045 - Tax Professionals - Program Application And Product Order Blanks - 2000

Financial

Publication 1045 - Tax Professionals - Program Application And Product Order Blanks - 2000

Financial

Related Categories

Parent category: Financial