Publication 505 - Tax Withholding And Estimated Tax Page 13

ADVERTISEMENT

1

1 2

2 3

3 4

4 5

5 6

6 7

7 8

8 9

9 10

10 11

11 12

12 13

13 14

14 15

15 16

16 17

17 18

18 19

19 20

20 21

21 22

22 23

23 24

24 25

25 26

26 27

27 28

28 29

29 30

30 31

31 32

32 33

33 34

34 35

35 36

36 37

37 38

38 39

39 40

40 41

41 42

42 43

43 44

44 45

45 46

46 47

47 48

48 49

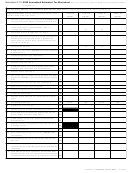

49Figure A. Exemption From Withholding on Form W-4

Note: Do not use this chart if you are 65 or older or blind, or if you will itemize your deductions or claim exemptions for dependents

or tax credits. Instead, see the discussions in this chapter under Exemption From Withholding.

Start Here

For 2001, did you have a

No

You CANNOT claim

right to a refund of ALL

exemption from

federal income tax withheld

withholding.

because you had NO tax

liability?

Yes

Yes

Will your 2002 total income be more than the amount

shown below for your filing status?

Single

$ 7,700

For 2002, will

No

Head of household

9,900

someone (such as

Married filing separately for

your parent) be able

BOTH 2001 and 2002

6,925

to claim you as a

Other married status (include BOTH

dependent?

spouses’ income whether filing

separately or jointly)

13,850

Qualifying widow(er)

10,850

Yes

No

No

Will your 2002 income

be more than $750?

Yes

Yes

Will your 2002 income

You CANNOT claim

You CAN claim

include more than $250

exemption from

exemption from

of unearned income

withholding.

withholding.

(interest, dividends, etc.)?

No

No

Yes

Will your 2002 total income be:

$4,700 or less if single, or

$3,925 or less if married?

Your employer can choose not to withhold

Special rule. Your employer can choose to

Taxable Fringe

treat a benefit provided during November or

income tax on the value of your personal use of

December as paid in the next year. Your em-

a car, truck, or other highway motor vehicle

Benefits

ployer must notify you if this rule is used.

provided by your employer. Your employer must

notify you if this choice is made.

Example 1.6. Your employer considers the

The value of certain noncash fringe benefits you

value of benefits paid from November 1, 2000,

When benefits are considered paid. Your

receive from your employer is considered part of

through October 31, 2001, as paid to you in

your pay. Your employer generally must with-

employer can choose to treat a fringe benefit as

2001. To determine the total value of benefits

hold income tax on these benefits from your

paid by the pay period, by the quarter, or on

paid to you in 2002, your employer will add the

regular pay for the period the benefits are paid or

some other basis as long as the benefit is con-

value of any benefits paid in November and

considered paid.

sidered paid at least once a year. Your employer

December of 2001 to the value of any benefits

can treat the benefit as being paid on one or

For information on fringe benefits, see Fringe

paid in January through October of 2002.

Benefits under Employee Compensation in Pub-

more dates during the year, even if you get the

lication 525.

entire benefit at one time.

Chapter 1 Tax Withholding for 2002

Page 13

ADVERTISEMENT

0 votes

Related Articles

Related forms

Plans) For Employees Of Public Schools And Certain Tax-exempt Organizations") Publication 571 - Tax-sheltered Annuity Plans (403(b) Plans) For Employees Of Public Schools And Certain Tax-exempt Organizations

Financial

Publication 571 - Tax-sheltered Annuity Plans (403(b) Plans) For Employees Of Public Schools And Certain Tax-exempt Organizations

Financial

Publication 1045 - Tax Professionals - Program Application And Product Order Blanks - 2000

Financial

Publication 1045 - Tax Professionals - Program Application And Product Order Blanks - 2000

Financial

Related Categories

Parent category: Financial