Publication 505 - Tax Withholding And Estimated Tax Page 24

ADVERTISEMENT

1

1 2

2 3

3 4

4 5

5 6

6 7

7 8

8 9

9 10

10 11

11 12

12 13

13 14

14 15

15 16

16 17

17 18

18 19

19 20

20 21

21 22

22 23

23 24

24 25

25 26

26 27

27 28

28 29

29 30

30 31

31 32

32 33

33 34

34 35

35 36

36 37

37 38

38 39

39 40

40 41

41 42

42 43

43 44

44 45

45 46

46 47

47 48

48 49

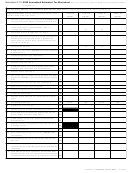

49Filled-in Worksheet 2.6 for Mira

Table 2.5

payments, you must file Form 2210 with your

(Example 2.7)

2002 tax return. See Annualized Income Install-

Single . . . . . . . . . . . . . . . . . . . $137,300

ment Method in chapter 4 for more information.

1. Amended total estimated tax due . . . . .

$4,100

Married filing jointly

2. Multiply line 1 by:

or qualifying widow(er) . . . . . . . . . $206,000

.50 if next payment is due

Married filing separately . . . . . . . . $103,000

Instructions For Worksheet 2.10

June 17, 2002

Head of household . . . . . . . . . . . $171,650

.75 if next payment is due

In that case, use the following worksheet to

September 16, 2002

The top of the worksheet shows the dates for

1.00 if next payment is due

figure the amount to enter on line 10.

each payment period. The periods build; that is,

January 15, 2003 . . . . . . . . . . . . . .

3,075

each period includes all previous periods. After

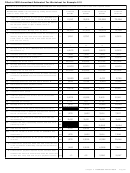

Worksheet 2.8

3. Estimated tax payments for all previous

the end of each payment period, complete the

periods . . . . . . . . . . . . . . . . . . . . .

900

1. Multiply $3,000 by your total expected

worksheet column for the period from the begin-

4. Next required payment: Subtract line 3

exemptions . . . . . . . . . . . . . . . . . .

from line 2 and enter the result (but not

ning of the tax year through the end of that

2. Enter the amount from line 3 of Section

less than zero) here and on your

payment period to figure the payment due for

A . . . . . . . . . . . . . . . . . . . . . . . .

payment-voucher for your next required

that period.

3. Enter the amount shown for your filing

payment . . . . . . . . . . . . . . . . . . . .

$2,175

status from Table 2.5 . . . . . . . . . . . .

If the payment on line 4 is due January 15,

4. Subtract line 3 from line 2 . . . . . . . . .

2003, stop here. Otherwise, go on to line 5.

Line 1. Enter your adjusted gross income for

5. Divide the amount on line 4 by $2,500

each period. This is your gross income, includ-

5. Add lines 3 and 4 . . . . . . . . . . . . . . .

3,075

($1,250 if married filing separately). If the

6. Subtract line 5 from line 1 and enter the

ing your share of partnership or S corporation

result is not a whole number, increase it

result (but not less than zero) . . . . . . .

1,025

income or loss, for the period, minus your adjust-

to the next whole number . . . . . . . . .

7. Each following required payment: If

6. Multiply the number on line 5 by .02.

ments to income for that period. (See Expected

the payment on line 4 is due June 17,

Enter the result as a decimal, but not

Adjusted Gross Income under How To Figure

2002, enter one-half of the amount on

more than 1 . . . . . . . . . . . . . . . . . .

line 6 here and on the payment-vouchers

Estimated Tax, earlier.)

7. Multiply the amount on line 1 by the

for your payments due September 16,

decimal on line 6 . . . . . . . . . . . . . . .

Self-employment income. If you had

2002, and January 15, 2003. If the

8. Subtract line 7 from line 1. Enter the

amount on line 4 is due September 16,

self-employment income, first complete Section

result here and on line 10 of Section A

2002, enter the full amount on line 6 here

B. Use the amounts on line 35c when figuring

and on the payment-voucher for your

the amount of adjusted gross income to enter on

payment due January 15, 2003 . . . . . .

$1,025

Line 12. Use the 2002 Tax Rate Schedules at

line 1.

the end of this chapter or in the instructions to

If Mira’s estimated tax does not change again,

Form 1040 – ES to figure your annualized in-

her required estimated tax payment for the

Line 4. Be sure to consider all deduction limits

come tax. For the special method that must be

fourth payment period will be $1,025.

figured on Schedule A.

used to figure tax on the income of a child under

File Form 2210 to avoid penalty. If your

14 who has more than $1,500 investment in-

Line 6. Multiply line 4 by line 5 and enter the

estimated tax payment for a previous period is

come, see Tax on Investment Income of Child

result on line 6, unless line 3 is more than

less than one-fourth of your amended estimated

Under 14 in Publication 929, Tax Rules for Chil-

$137,300 ($68,650 if married filing separately).

tax, you may be charged a penalty for underpay-

dren and Dependents.

In that case, use the following worksheet to

ment of estimated tax for that period when you

Capital gains tax computation. The regu-

figure the amount to enter on line 6. Complete

file your tax return. To avoid the penalty, you

lar income tax rates for individuals do not apply

this worksheet for each period.

must file Form 2210 with your 2002 tax return.

to a net capital gain. Instead, your net capital

You must also show that the total of your with-

Worksheet 2.7

gain is taxed at a lower maximum rate.

holding and estimated tax payment for the pe-

The term “net capital gain” means the

1. Enter the amount from line 4 of Section

riod was at least as much as your annualized

A . . . . . . . . . . . . . . . . . . . . . . . .

amount by which your net long-term capital gain

income installment. See chapter 4 for more in-

2. Enter the amount included in line 1 for

for the year is more than your net short-term

formation.

medical and dental expenses,

capital loss.

investment interest, casualty or theft

The maximum rate may be 8%, 10%, 20%,

Annualized Income

losses, and gambling losses . . . . . . .

25%, or 28%, or a combination of those rates.

3. Subtract line 2 from line 1 . . . . . . . .

Installment Method

4. Enter the number from line 5 of Section

Use the following worksheet to figure

A . . . . . . . . . . . . . . . . . . . . . . . .

If you do not receive your income evenly

the amount to enter on line 12 if the

5. Multiply the amount on line 1 by the

throughout the year (for example, your income

number on line 4 . . . . . . . . . . . . . .

amount on line 1 includes capital gain.

Note. If the amount on line 3 is zero,

from a repair shop you operate is much larger in

stop here and enter the amount from

the summer than it is during the rest of the year),

Worksheet 2.9

line

your required estimated tax payment for one or

5 on line 6 of Section A.

more periods may be less than the amount fig-

1. Enter the amount from line 11 of your

6. Multiply the amount on line 3 by the

ured using the regular installment method.

2002 Annualized Estimated Tax

number on line 4 . . . . . . . . . . . . . .

Worksheet . . . . . . . . . . . . . . . . . . .

To see whether you can pay less for any

7. Multiply the amount on line 6 by .80 . .

2. Enter the net capital gain expected for

period, complete the blank 2002 Annualized Es-

8. Enter the amount from line 3 of

2002 . . . . . . . . . . . . . . . . . . . . . .

Section A . . . . . . . . . . . . . . . . . .

timated Tax Worksheet (Worksheet 2.10) later

3. Combine the net short-term capital loss

9. Enter $137,300 ($68,650 if married

in this chapter. (Note. You must first complete

and 28% rate gain or loss expected for

filing separately) . . . . . . . . . . . . . .

2002. If zero or less, enter 0 . . . . . . . .

the 2002 Estimated Tax Worksheet through line

10. Subtract line 9 from line 8 . . . . . . . .

4. Enter the unrecaptured section 1250

16.) The worksheet annualizes your tax at the

11. Multiply the amount on line 10

gain expected for 2002 . . . . . . . . . . .

end of each period based on a reasonable esti-

by .03 . . . . . . . . . . . . . . . . . . . . .

5. Add lines 3 and 4 . . . . . . . . . . . . . .

12. Enter the smaller of line 7 or line 11 . .

mate of your income, deductions, and other

6. Subtract line 5 from line 2. If zero or

13. Subtract line 12 from line 5. Enter the

items relating to events that occurred since the

less, enter 0 . . . . . . . . . . . . . . . . . .

result here and on line 6 of Section A

beginning of the tax year through the end of the

7. Subtract line 6 from line 1. If zero or

less, enter 0 . . . . . . . . . . . . . . . . . .

period. Use the result you figure on line 26d to

8. Enter the smaller of line 1 or $46,700

make your estimated tax payments and com-

Line 7. See the 2002 Standard Deduction Ta-

($27,950 if single; $23,350 if married

plete your payment-vouchers.

bles at the end of this chapter. Find your stan-

filing separately; $37,450 if head of

See Example 2.10 for an illustration of the

dard deduction in the appropriate table.

household) . . . . . . . . . . . . . . . . . .

9. Enter the smaller of line 7 or line 8 . . .

worksheet.

10. Subtract line 2 from line 1. If zero or

Line 10. Multiply $3,000 by your total ex-

less, enter 0 . . . . . . . . . . . . . . . . . .

pected exemptions, unless line 3 is more than

11. Enter the larger of line 9 or line 10 . . . .

Note. If you use the annualized income in-

the amount shown for your filing status in the

12. Tax on amount on line 11 from the 2002

stallment method to figure your estimated tax

following table.

Tax Rate Schedule . . . . . . . . . . . . .

Page 24

Chapter 2 Estimated Tax for 2002

ADVERTISEMENT

0 votes

Related Articles

Related forms

Plans) For Employees Of Public Schools And Certain Tax-exempt Organizations") Publication 571 - Tax-sheltered Annuity Plans (403(b) Plans) For Employees Of Public Schools And Certain Tax-exempt Organizations

Financial

Publication 571 - Tax-sheltered Annuity Plans (403(b) Plans) For Employees Of Public Schools And Certain Tax-exempt Organizations

Financial

Publication 1045 - Tax Professionals - Program Application And Product Order Blanks - 2000

Financial

Publication 1045 - Tax Professionals - Program Application And Product Order Blanks - 2000

Financial

Related Categories

Parent category: Financial