Publication 505 - Tax Withholding And Estimated Tax Page 39

ADVERTISEMENT

1

1 2

2 3

3 4

4 5

5 6

6 7

7 8

8 9

9 10

10 11

11 12

12 13

13 14

14 15

15 16

16 17

17 18

18 19

19 20

20 21

21 22

22 23

23 24

24 25

25 26

26 27

27 28

28 29

29 30

30 31

31 32

32 33

33 34

34 35

35 36

36 37

37 38

38 39

39 40

40 41

41 42

42 43

43 44

44 45

45 46

46 47

47 48

48 49

491040, line 40) is $11,000. She does not claim

payment period. Also, you cannot use your ac-

Regular Method for

any credits or pay any other taxes.

tual withholding during each period to figure

For 2001, Ivy had $1,600 income tax with-

your payments for each period. These methods,

Figuring the Penalty

held and paid $6,800 estimated tax. Her total

which may give you a smaller penalty amount,

payments were $8,400. 90% of her 2001 tax is

are explained later under Figuring Your Un-

$9,900. Because she paid less than her 2000

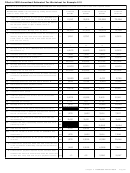

You must use the regular method in Part IV of

derpayment.

tax and less than 90% of her 2001 tax, and does

Form 2210 to figure your penalty for underpay-

not meet an exception, Ivy knows that she owes

ment of estimated tax if any of the following

Completing Part III. Complete Part III follow-

a penalty for underpayment of estimated tax.

apply to you.

ing the line-by-line instructions.

She decides to figure the penalty on Form 2210

•

First, figure your total underpayment for the

You paid one or more estimated tax pay-

and pay it with her $2,600 tax balance when she

year (line 18) by subtracting the total of your

ments on a date other than the due date.

files her tax return.

withholding and estimated tax payments (line

•

Ivy’s required annual payment is $9,900

You paid at least one, but less than four,

17) from your required annual payment (Part II,

($11,000 × 90%) because that is smaller than

installments of estimated tax.

line 14). Then figure the penalty you would owe

her 2000 tax.

•

You paid estimated tax payments in une-

if the underpayment remained unpaid up to April

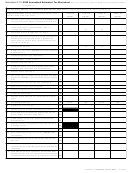

Ivy’s filled-in Form 2210 is shown at the end

qual amounts.

15, 2002. This amount (line 19) is the maximum

of this chapter. Her required annual payment of

•

estimated tax penalty on your underpayment.

$9,900 is shown on line 14.

You use the annualized income install-

Next, figure any part of the maximum penalty

ment method to figure your underpayment

Different 2000 filing status. If you file a sepa-

you do not owe (line 20) because your un-

for each payment period.

rate return for 2001, but you filed a joint return

derpayment was paid before the due date of

•

You use your actual withholding during

with your spouse for 2000, see 2000 joint return

your return. For example, if you filed your 2001

each payment period to figure your pay-

and 2001 separate returns, earlier, to figure the

return and paid the tax balance on April 3, 2002,

ments.

amount to enter as your 2000 tax on line 13 of

you do not owe the penalty for the 12-day period

Form 2210.

from April 4 through April 15. Therefore, you

If you use the regular method, figure your

would figure the amount to enter on line 20 using

underpayment for each payment period in Sec-

12 days.

tion A, then figure your penalty for each payment

period in Section B.

Short Method for

Finally, subtract from the maximum penalty

amount (line 19) any part you do not owe (line

Figuring the Penalty

Figuring Your Underpayment

20). The result (line 21) is the penalty you owe.

Enter that amount on line 71 of Form 1040 or

(Section A of Part IV)

line 46 of Form 1040A. Attach Form 2210 to your

You may be able to use the short method in Part

return only if you checked one of the boxes in

Figure your underpayment of estimated tax for

III of Form 2210 to figure your penalty for un-

Part I.

each payment period in Section A following the

derpayment of estimated tax. If you qualify to

line-by-line instructions. Complete each line for

use this method, it will result in the same penalty

Example 4.5. The facts are the same as in

a payment period column before completing the

amount as the regular method. However, either

Example 4.4. Ivy paid her estimated tax pay-

next column.

the annualized income installment method or

ments in four installments of $1,700 ($6,800 ÷ 4)

the actual withholding method, explained later,

Required installment. Your required pay-

may result in a lower penalty.

each on the dates they were due.

ment for each payment period (line 22) is usually

You can use the short method only if you

Ivy qualifies to use the short method to figure

one-fourth of your required annual payment

meet one of the following requirements.

her estimated tax penalty. Using the annualized

(Part II, line 14). However, if you are using the

income installment method or actual withholding

1) You made no estimated tax payments for

annualized income installment method (de-

will not give her a smaller penalty amount be-

2001 (it does not matter whether you had

scribed later), first complete Schedule AI (Form

cause her income and withholding were distrib-

income tax withholding); or

2210), and then enter the amounts from line 25

uted evenly throughout the year. Therefore, she

of that schedule on line 22 of Form 2210.

2) You paid estimated tax in four equal

figures her penalty in Part III of Form 2210 and

amounts on the due dates.

leaves Part IV (not shown) blank.

Payments. On line 23, enter in each column

Ivy figures her $1,500 total underpayment for

the total of:

Note. If any payment was made earlier than

the year (line 18) by subtracting the total of her

1) Your estimated tax paid after the due date

the due date, you can use the short method, but

withholding and estimated tax payments

for the previous column and by the due

using it may cause you to pay a larger penalty

($8,400) from her $9,900 required annual pay-

date shown, and

than using the regular method. If the payment

ment (Part II, line 14). The maximum penalty on

her underpayment (line 19) is $66 ($1,500 ×

was only a few days early, the difference is likely

2) One-fourth of your withholding.

to be small.

.04397).

For special rules for figuring your payments, see

If you do not meet either requirement, figure

Ivy plans to file her return and pay her $2,600

the instructions for Form 2210.

your penalty using the regular method in Part IV,

tax balance on March 16, 2002, 30 days before

If you file Form 1040, your withholding is the

Form 2210.

April 15. Therefore, she does not owe part of the

amount on line 59, plus any excess social secur-

You cannot use the short method if any of

maximum penalty amount. The part she does

ity or railroad retirement tax withholding on line

the following applies.

not owe (line 20) is figured as follows.

62. If you file Form 1040A, your withholding is

$1,500 × 30 × .00016 = $7

the amount on line 37, plus any excess social

1) You made any estimated tax payments

security or railroad retirement tax withholding

late.

Ivy subtracts the $7 from the $66 maximum

included in the total on line 41.

2) You checked the box on line 1b or 1c in

penalty and enters the result, $59, on line 21 and

Actual withholding method. Instead of us-

Part I of Form 2210.

on line 71 of her Form 1040. She adds $59 to her

ing one-fourth of your withholding to figure your

3) You are filing Form 1040NR or

$2,600 tax balance and enters the result, $2,659

payments, you can choose to establish how

1040NR – EZ and you did not receive

on line 70 of her Form 1040. Ivy files her return

much was actually withheld by the due dates

wages as an employee subject to U.S. in-

on March 16 and attaches a check for $2,659.

and use those amounts. You can make this

come tax withholding.

Because Ivy did not check any of the boxes in

choice separately for the tax withheld from your

Part I, she does not attach Form 2210 to her tax

wages and for all other withholding.

return.

Note. If you use the short method, you can-

Using your actual withholding may result in a

Ivy’s filled-in Form 2210, Part III is shown at

not use the annualized income installment

smaller penalty if most of your withholding oc-

method to figure your underpayment for each

the end of this chapter.

curred early in the year.

Chapter 4 Underpayment Penalty for 2001

Page 39

ADVERTISEMENT

0 votes

Related Articles

Related forms

Plans) For Employees Of Public Schools And Certain Tax-exempt Organizations") Publication 571 - Tax-sheltered Annuity Plans (403(b) Plans) For Employees Of Public Schools And Certain Tax-exempt Organizations

Financial

Publication 571 - Tax-sheltered Annuity Plans (403(b) Plans) For Employees Of Public Schools And Certain Tax-exempt Organizations

Financial

Publication 1045 - Tax Professionals - Program Application And Product Order Blanks - 2000

Financial

Publication 1045 - Tax Professionals - Program Application And Product Order Blanks - 2000

Financial

Related Categories

Parent category: Financial