Publication 505 - Tax Withholding And Estimated Tax Page 41

ADVERTISEMENT

1

1 2

2 3

3 4

4 5

5 6

6 7

7 8

8 9

9 10

10 11

11 12

12 13

13 14

14 15

15 16

16 17

17 18

18 19

19 20

20 21

21 22

22 23

23 24

24 25

25 26

26 27

27 28

28 29

29 30

30 31

31 32

32 33

33 34

34 35

35 36

36 37

37 38

38 39

39 40

40 41

41 42

42 43

43 44

44 45

45 46

46 47

47 48

48 49

494th Column — 1/1/01 to 12/31/01:

If you use Schedule A1 for any pay-

each underpayment shown on line 29. If an

$1,750 per month × 12 months . . . . . . . . $21,000

!

ment due date, you must use it for all

underpayment remained unpaid for more than

Plus: Self-employment income through

payment due dates.

one rate period, the penalty on that underpay-

CAUTION

12/31/01 . . . . . . . . . . . . . . . .

16,600

ment will be figured using more than one rate.

Less: Self-employment tax deduction

($2,346 ÷ 2) . . . . . . . . . . . . . .

Use lines 31, 33, and 35 to figure the number

(1,173)

Completing Schedule AI of Form 2210. Fol-

$36,427

of days the underpayment remained unpaid.

low your Form 2210 instructions to complete

(Also see Table 4 – 1.) Use lines 32, 34, and 36

Ben completes the rest of Schedule A1 to deter-

Schedule AI. For each period shown on Sched-

to figure the actual penalty amount by applying

mine the amounts to put on Form 2210, line 22.

ule AI, figure your income and deductions based

the rate against the underpayment for the num-

Ben then figures his underpayment in Part

on your method of accounting. If you use the

ber of days it remained unpaid.

IV, Section A. He finds that he overpaid his

cash method of accounting (used by most peo-

If an underpayment remained unpaid for the

estimated tax for the first payment period, but he

ple), include all income actually or constructively

entire period, use Table 4 – 2 to determine the

underpaid his estimated tax for the other three

received during the period and all deductions

number of days to enter for each period.

periods. Example 4.9 illustrates how Ben com-

actually paid during the period.

pletes Part IV, Section B, of his Form 2210.

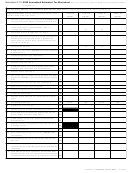

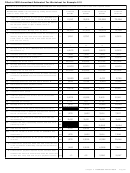

Table 4 – 2

Note. Each period includes amounts from

Chart of Total Days

the previous period(s).

Figuring Your Penalty

•

Column

Column

Column

Column

Period (a) includes items for January

(Section B of Part IV)

(a)

(b)

(c)

(d)

through March.

•

Figure the amount of your penalty in Section B,

line 31

76

15

NA

NA

Period (b) includes items for January

Part IV of Form 2210, following the instructions.

through May.

line 33

184

184

98

NA

The penalty is imposed on each underpayment

•

Period (c) includes items for January

shown on line 29, Section A, for the number of

line 35

105

105

105

90

through August.

days through April 15, 2001, that it remained

•

unpaid. (You may find it helpful to show the date

Period (d) includes items for the entire

Example 4.8. In Example 4.6, Ben Brown de-

of payment beside each amount on line 29.)

year.

termined that he had an underpayment for all

There are three rate periods to figure the

four payment periods.

penalty. Use Rate Period 1 (lines 31 and 32) to

Example 4.7. The facts are the same as in

Ben’s filled-in Form 2210 is shown at the end

apply the 8% rate in effect between April 16,

Example 4.6, except that Ben did not receive his

of this chapter. This example illustrates Part IV,

2001 and June 30, 2001. Use Rate Period 2

income evenly throughout the year. Therefore,

Section B, of that form.

(lines 33 and 34) to apply the 7% rate in effect

he decides to figure his required installment for

Ben’s 2001 tax is $7,031. His minimum re-

between July 1, 2001 and December 31, 2001.

each period (line 22 of Form 2210) using the

quired payment for each period is $1,529

Use Rate Period 3 (lines 35 and 36) to apply the

annualized income installment method.

($6,116 ÷ 4). His $3,228 withholding is consid-

6% rate in effect between January 1, 2002 and

Ben’s filled-in Schedule AI and Part IV of

ered paid in four equal installments of $807, one

April 15, 2002.

Form 2210 using this method are shown at the

on each payment due date. Therefore, he must

Aid for counting days. Table 4 – 1 provides a

end of this chapter.

make estimated tax payments of $722 each

simple method to count the number of days

Ben’s wages during 2001 were $21,000

period. Ben made estimated tax payments of

between payment dates or between a due date

($1,750 a month). His net earnings from a busi-

$1,000 on September 2, 2001, and $1,000 on

and a payment date.

ness he started during the year were $16,600,

January 12, 2002. He plans to file his return and

received as follows:

pay his $1,803 tax balance ($7,031 tax − $5,228

1) Find the number for the date the payment

withholding and estimated tax payments) on

was due.

April through May

$4,600

April 15, 2002. Therefore, he is considered to

June through August

4,000

2) Find the number for the date the payment

have made the following payments for tax year

September through December

8,000

was made.

2001:

Before Ben can figure his adjusted gross

3) Subtract the due date “number” from the

income for each period (line 1 of Schedule AI),

April 15, 2001 . . . . . . . . . . . . . .

$ 807

payment date “number.”

he must figure his deduction for self-employ-

June 15, 2001 . . . . . . . . . . . . .

807

September 2, 2001 . . . . . . . . . .

1,000

ment tax for each period. He completes Part II of

For example, if a payment was due on June

September 15, 2001 . . . . . . . . .

807

Schedule AI first.

15 (61), but was not paid until November 4

January 12, 2002 . . . . . . . . . . .

1,000

Ben had no self-employment income for the

(203), the payment was 142 (203 − 61) days

January 15, 2002 . . . . . . . . . . .

807

first period, so he leaves the lines in that column

late.

April 15, 2002 . . . . . . . . . . . . . .

1,803

blank. His self-employment income was $4,600

Payments. Before completing Section B,

for the second period, $8,600 ($4,600 + $4,000)

Penalty for first period (April 15, 2001) —

make a list of the payments you made after the

for the third period, and $16,600 ($8,600 +

column (a). Ben’s $722 underpayment for the

due date (or the last day payments could be

$8,000) for the fourth period. He multiplies each

first payment period was paid by applying $722

made on time) for the earliest payment period an

amount by 92.35% (.9235) to find the amounts

of his $807 payment on June 15, 2001. The

underpayment occurred. For example, if you

to enter on line 26. He then fills out the rest of

$722 remained unpaid 61 days (April 16 through

had an underpayment for the first payment pe-

Part II.

June 15, 2001). Ben enters “61” on line 31 and

riod, list your payments after April 15, 2001. You

Ben figures the amounts to enter on line 1 of

figures this part of the penalty on line 32.

can use the tables in the Form 2210 instructions

Schedule AI as follows:

Penalty for second period (June 15, 2001)

to make your list. Follow those instructions for

— column (b). Ben figures his second period

1st Column — 1/1/01 to 3/31/01:

listing income tax withheld and payments made

$1,750 per month × 3 months . . . . . . . . .

$5,250

underpayment as follows.

with your return. Use the list to determine when

each underpayment was paid.

2nd Column — 1/1/01 to 5/31/01:

1) Of the $807 he paid for the second period,

$1,750 per month × 5 months . . . . . . . . .

$8,750

Underpayment paid in two or more parts. If

$722 is applied to the underpayment re-

Plus: Self-employment income through

an underpayment was paid in two or more parts

maining from the first period.

5/31/01 . . . . . . . . . . . . . . . . .

4,600

Less: Self-employment tax deduction

on different dates, you must figure the penalty

2) That leaves $85 ($807 − $722) to apply to

($1,560 ÷ 4.8) . . . . . . . . . . . . .

(325)

separately for each part. (You may find it helpful

his second period required installment of

$13,025

to show the underpayment on line 29, Section A,

3rd Column — 1/1/01 to 8/31/01:

$1,529.

broken down into the parts paid on different

$1,750 per month × 8 months

$14,000

3) The result, $1,444 ($1,529 − $85) is Ben’s

dates.)

Plus: Self-employment income through

underpayment for the second period.

8/31/01 . . . . . . . . . . . . . . . . .

8,600

Figuring the penalty. Form 2210 for 2001

Less: Self-employment tax deduction

($1,822 ÷ 3) . . . . . . . . . . . . . .

has 3 rate periods. Figure the underpayment

The $1,444 underpayment is paid in two

(607)

penalty by applying the appropriate rate against

parts by applying the $1,000 paid on September

$21,993

Chapter 4 Underpayment Penalty for 2001

Page 41

ADVERTISEMENT

0 votes

Related Articles

Related forms

Plans) For Employees Of Public Schools And Certain Tax-exempt Organizations") Publication 571 - Tax-sheltered Annuity Plans (403(b) Plans) For Employees Of Public Schools And Certain Tax-exempt Organizations

Financial

Publication 571 - Tax-sheltered Annuity Plans (403(b) Plans) For Employees Of Public Schools And Certain Tax-exempt Organizations

Financial

Publication 1045 - Tax Professionals - Program Application And Product Order Blanks - 2000

Financial

Publication 1045 - Tax Professionals - Program Application And Product Order Blanks - 2000

Financial

Related Categories

Parent category: Financial