Iowa Withholding Tax Booklet And Tax Tables - 2005 Page 15

ADVERTISEMENT

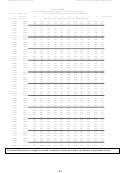

1

1 2

2 3

3 4

4 5

5 6

6 7

7 8

8 9

9 10

10 11

11 12

12 13

13 14

14 15

15 16

16 17

17 18

18 19

19 20

20 21

21 22

22 23

23 24

24 25

25 26

26 27

27 28

28Iowa Department of Revenue

Find us on the Web at

Instructions

1. Multiply the amount of bonus by the number of times during the year a bonus is

paid.

2. Determine the annual base wages or salary of the employee before bonuses

3. Add the two amounts together. Determine the withholding from the annual

withholding table.

4. Determine the annual withholding on the base amount.

5. Subtract the withholding on the base wages from the total withholding.

6. Divide the result by the number of times a year a bonus is paid. This amount is

the withholding on the bonus only.

Example

A $2,000 quarterly bonus is paid to a person with a base salary of $300 a week, who

claims zero personal allowances.

1. $2,000 bonus x 4 quarters = $8,000 annualized bonus

2. $300 salary per week x 52 weeks = $15,600 base annual salary

3. $8,000 + $15,600 = $23,600 annualized pay. Withholding from annual table =

$916.00

4. Withholding on base pay is $473.00.

5. $916.00 (withholding on gross pay) - $473.00 (withholding on base pay) =

$443.00

6. $443.00 ÷ 4 = $110.75. (Rounded = $111.00)

PAYMENTS MADE ON AN ANNUAL BASIS

Payments made only once a year include: compensation paid to entertainers performing in Iowa;

rent from real or personal property; distributive shares to a beneficiary of an estate, or trust

payments to landlords by agents, including payments by elevator operators for sale of grain or

other commodities; income derived from any business of a temporary nature such as contracts

for construction or fees paid for services; and annual bonuses paid to employees.

ANNUAL BONUSES

Instructions

1. Determine the annual withholding on the base pay.

2. Add together the annual base pay and the bonus.

3. Determine the withholding on the total income from the annual table.

4. Subtract the withholding on the base pay from total withholding.

5. Difference equals the withholding on the bonus.

Example

Person who has an annual base pay of $21,500, an annual bonus of $10,750, and claims zero

personal allowances.

1. Withholding on base pay = $803.00

2. Base pay plus bonus = $32,250 annual pay

3. Withholding from annual table equals $1,420

4. Difference is $1,420.00 - $803.00 = $617.00.

5. Withholding on bonus equals $617.00.

14

ADVERTISEMENT

0 votes

Related Articles

Related forms

Related Categories

Parent category: Financial