Form 740-Np - Kentucky Income Tax Return Nonresident Or Part-Year Resident - 2012 Page 11

ADVERTISEMENT

1

1 2

2 3

3 4

4 5

5 6

6 7

7 8

8 9

9 10

10 11

11 12

12 13

13 14

14 15

15 16

16 17

17 18

18 19

19 20

20 21

21 22

22 23

23 24

24 25

25 26

26 27

27 28

28 29

29 30

30 31

31 32

32 33

33 34

34 35

35 36

36 37

37 38

38 39

39 40

40 41

41 42

42 43

43 44

44 45

45 46

46 47

47 48

48 49

49 50

50 51

51 52

52 53

53 54

54 55

55 56

56 57

57 58

58 59

59 60

6017, Column B) to federal total income (Line 17, Column A).

Line 27, Individual Retirement Arrangements (IRAs)—The

deduction cannot exceed income earned in Kentucky. Con-

Enter in Column A, the total of any other adjustments to the

tributions made by full-year nonresidents are limited to the

total income listed on your federal return. Enter in Column B,

percentage of their Kentucky earned income to their federal

the allowable deduction with the above limitation.

earned income. Use federal worksheets and instructions with

the above limitations.

Nonresident military members filing to report nonmilitary

income to Kentucky must subtract their military income on

Line 33, Column A with a notation “nonresident military

Line 28, Student Loan Interest Deduction—Federal limita-

income.” The qualifying spouse of a military member who

tions apply. Student loan interest deduction is limited to the

has nonmilitary income should subtract their income on

percentage of Kentucky total income (Line 17, Column B) to

Line 33, Column A with a notation “military spouse income.”

federal total income (Line 17, Column A). Enter in Column

Nonresident military and qualifying military spouse income

A, the total of student loan interest from your federal return.

is not limited to the percentage of Kentucky total income to

Enter in Column B, the allowable deduction with the above

federal total income.

limitation.

INCOME/TAX

Line 29, Reserved—Pending federal legislation.

Note: These items are reported on page 1, Form 740-NP.

Line 30, Domestic Production Activities Deduction—For

taxable years beginning on or after January 1, 2010, the

Line 7—Enter the percentage from page 4, Section D, Line

amount of the domestic production activities deduction

36.

(DPAD) for Kentucky income tax returns will remain 6 percent

as allowed in Section 199(a)(2) of the Internal Revenue Code

Line 8—Enter federal Adjusted Gross Income from page 4,

(IRC) for taxable years beginning before January 1, 2010.

Section D, Column A, Line 35.

Kentucky does not recognize the 9 percent DPAD calculation

rate allowed for federal income tax returns filed for taxable

Line 9—Enter Kentucky Adjusted Gross Income from page 4,

years beginning on or after January 1, 2010.

Section D, Column B, Line 35.

Part-year resident or full-year nonresident individuals

Line 10—Nonitemizers, enter the standard deduction of

shall prorate the allowable federal DPAD based upon the

$2,290. If filing a joint return, only one $2,290 standard de-

percentage of Kentucky domestic production gross receipts

duction is allowed.

to federal domestic production gross receipts. The KDPAD

shall not exceed 50 percent of the Kentucky W-2 wages from

Line 11—Itemizers, complete Schedule A and enter itemized

the entity that generated Kentucky domestic production gross

deductions on Line 11. If one spouse itemizes deductions,

receipts. This deduction must be recomputed based on the

the other must itemize. See specific instructions for Sched-

6 percent allowed for the Kentucky DPAD as opposed to the

ule A.

9 percent allowed for the federal DPAD deduction. A pass-

through entity is required to attach information containing

Line 12—Multiply Line 11 by the percentage on Line 7. If Line

each individual par tner's, member's or shareholder's

12 does not exceed $2,290 and your filing status is 1 or 2,

distributive share of DPGR, KDPGR and Kentucky W-2 wages

you should take the standard deduction. Married couples

allocable to DPGR to each individual partner's, member's or

filing separate returns, see special rules under instructions

shareholder's Kentucky Schedule K-1 for purposes of making

for Schedule A.

this calculation.

Line 13—Subtract either Line 10 or 12 from Line 9. This is

Line 31, Long–Term Care Insurance Premiums—Long-term

your Taxable Income.

care insurance premiums deducted by full-year nonresidents

are limited to the percentage of their Kentuck y total

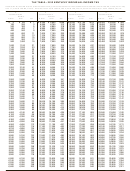

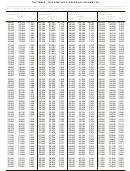

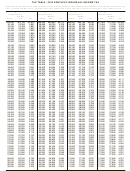

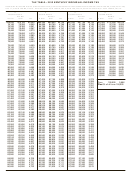

Line 14—Use the tax table provided in the instructions to

income (Line 17, Column B) to their federal total income

compute your tax. Enter this amount on Line 14.

(Line 17, Column A). Do not claim amounts as an itemized

deduction.

If you had a lump-sum distribution from a qualified retirement

plan, complete Schedule P and Form 4972-K and attach copies

Line 32, Health Insurance Premiums—Medical and dental

to Form 740-NP. The amount of tax computed on Form

insurance premiums deducted by full-year nonresidents

4972-K should be included in the amount on this line.

are limited to the percentage of their Kentucky total income

(Line 17, Column B) to their federal total income (Line 17,

Schedule J, Farm Income Averaging—If you elect Farm

Column A).

Income Averaging on your federal return, you may also use

this method for Kentucky. Complete and attach Kentucky

Note: This deduction applies to premiums paid with after-tax

Schedule J and include tax in the amount on this line.

dollars. Premiums paid with pretax income (cafeteria plans

and vouchers already excluded from wage income) are not

Line 15—Enter amount from page 3, Section A, Line 22. See

deductible again. Do not include long-term care insurance

instructions for Section A.

premiums deducted on Line 31. If you are eligible for the

Health Coverage Tax Credit, you may not deduct premiums

Line 17—Enter amount from page 3, Section B, Line 4. See

paid on your behalf (advance payments) and you must reduce

instructions for Section B.

the amount you paid by the amount of health coverage tax

credit. (See federal Form 8885.)

Line 18—Multiply the amount on Line 17 by the percentage

on Line 7 and enter result here.

Line 33, Other Deductions—List any other adjustments to total

income not listed above on lines 18 through 32. List the type of

deduction in the space provided. Other deductions, with the

exception of military and qualifying military spouse income,

are limited to the percentage of Kentucky total income (Line

5

ADVERTISEMENT

0 votes

Related Articles

Related forms

Instructions For Form 740-np - Kentucky Income Tax Return Nonresident Or Part-year Resident - 2011

Financial

Instructions For Form 740-np - Kentucky Income Tax Return Nonresident Or Part-year Resident - 2011

Financial

Form 740-np - Kentucky Individual Incometax Return Nonresident Or Part-year Resident - 2012

Financial

Form 740-np - Kentucky Individual Incometax Return Nonresident Or Part-year Resident - 2012

Financial

Form 740-np - Kentucky Individual Incometax Return Nonresident Or Part-year Resident - 2013

Financial

Form 740-np - Kentucky Individual Incometax Return Nonresident Or Part-year Resident - 2013

Financial

Form Ar1000nr - Arkansas Individual Income Tax Return Nonresident And Part Year Resident - 2012

Financial

Form Ar1000nr - Arkansas Individual Income Tax Return Nonresident And Part Year Resident - 2012

Financial

Form 740-np - Kentucky Individual Income Tax Return Nonresident Or Part-year Resident - 2007

Financial

Form 740-np - Kentucky Individual Income Tax Return Nonresident Or Part-year Resident - 2007

Financial

Form 740-np - Kentucky Individual Income Tax Return Nonresident Or Part-year Resident - 2014

Financial

Form 740-np - Kentucky Individual Income Tax Return Nonresident Or Part-year Resident - 2014

Financial

Form 740-np - Kentucky Individual Income Tax Return Nonresident Or Part-year Resident - 2016

Financial

Form 740-np - Kentucky Individual Income Tax Return Nonresident Or Part-year Resident - 2016

Financial

Related Categories

Parent category: Financial