Form 740-Np - Kentucky Income Tax Return Nonresident Or Part-Year Resident - 2012 Page 54

ADVERTISEMENT

1

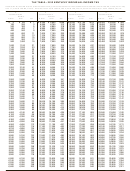

1 2

2 3

3 4

4 5

5 6

6 7

7 8

8 9

9 10

10 11

11 12

12 13

13 14

14 15

15 16

16 17

17 18

18 19

19 20

20 21

21 22

22 23

23 24

24 25

25 26

26 27

27 28

28 29

29 30

30 31

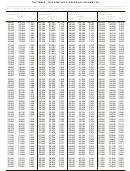

31 32

32 33

33 34

34 35

35 36

36 37

37 38

38 39

39 40

40 41

41 42

42 43

43 44

44 45

45 46

46 47

47 48

48 49

49 50

50 51

51 52

52 53

53 54

54 55

55 56

56 57

57 58

58 59

59 60

60Instructions for Form 8863-K

Purpose of Form—Use Form 8863-K to calculate and claim your

Line 1, Column E—Add Column C and Column D.

education credits. The education credits are: the Hope Credit

Line 1, Column F—Enter one-half of the amount in Column E.

and the Lifetime Learning Credit. These credits are based on

Line 2—Add all amounts in Column F for all students to com-

qualified education expenses paid to an eligible postsecond-

pute your tentative Hope credit. If you have expenses for more

ary educational institution located in Kentucky. If you elected

than two students, attach a list to Form 8863-K and list the total

to claim the education credit for federal purposes rather than

for all students on Line 2. If you are taking the Lifetime Learn-

the tuition and fees deduction, you must make that same elec-

ing Credit for another student, go to Part III; otherwise go to

tion for Kentucky purposes.

Part IV.

Caution: Requirements for the 2012 Kentucky Education Tu-

Part III—Lifetime Learning Credit—You may be able to take

ition Tax Credit are different from the federal education re-

25% of the Lifetime Learning Credit that equals 20% of quali-

quirements due to Kentucky not adopting the American Re-

fied expenses paid, up to a maximum of $10,000 of qualified

covery and Reinvestment Act of 2009.

expenses per return. The maximum amount of Lifetime Learn-

Qualified Education Expenses—Generally, qualified educa-

ing Credit you can claim on your tax return for the tax year

tion expenses are amounts paid in 2012 for tuition and fees

is $2,000. For Kentucky, the Lifetime Learning Credit is then

required for the student’s enrollment or attendance at an eli-

limited to 25% of the $2,000 for a maximum allowed of $500

gible educational institution. It does not matter whether the

per return.

expenses were paid in cash, by check, by credit card, or with

borrowed funds.

Line 3, Column A–D—Enter student’s name, Social security

number, name and address of qualified Kentucky institution

Eligible Educational Institution located in Kentucky—An eli-

and amount of qualified expenses.

gible educational institution is generally any accredited public,

nonprofit, or private college, university, vocational school, or

Line 4—Add all amounts in Column D for all students.

other postsecondary institution. Also, the institution must be

Line 5—Enter the smaller of Line 4 or $10,000.

eligible to participate in a student aid program administered

Line 6—Multiply Line 5 by 20%. Do not enter more than $2,000.

by the Department of Education. The institution must also be

This is your tentative Lifetime Learning Credit.

physically located in Kentucky to qualify.

Part I, Qualifications—All questions in Part I must be answered

Line 7—Add Line 2 (tentative Hope Credit) and Line 6 (tenta-

yes to be eligible for the Kentucky Education Tuition Tax

tive Lifetime Learning Credit) to get your tentative Kentucky

Credit.

Education Credits. Enter the amount on Line 7 and on page 2,

Line 8.

Part II, Hope Credit—You may be able to take a credit of up to

25% of $1,800 for qualified education expenses paid for each

Part IV—Allowable Education Credits—

student who qualifies for the Hope Credit. The Hope Credit

Line 9 – Line 13—You cannot take any Kentucky Education

equals 100% of the first $1,200 and 50% of the next $1,200 of

Credits if your federal adjusted gross income (federal Form

qualified expenses paid for each eligible student. For Ken-

1040, Line 37 or 1040A, Line 21) exceeds $124,000 if married,

tucky, the credit is then limited to 25% for a maximum amount

filing jointly or married, filing separately on a combined re-

allowed of $450 for each student who qualified. You can take

turn ($62,000 if single). If you are filing a separate return, you

the Hope Credit for a student if all of the following apply.

do not qualify for this credit. If your income is greater than

•

As of the beginning of 2012, the student had not com-

$100,000, you may only be entitled to a portion of the credits, if

pleted the first 2 years of postsecondary education (gen-

any. Proceed to Line 14 if your income is less than $100,000.

erally, the freshman and sophomore years of college), as

Line 14—Enter the amount from Line 8 if your credit was not

determined by the eligible educational institution. For this

limited based on income. If the credit was limited based on

purpose, do not include academic credit awarded solely

income, multiply the amount on Line 8 by the decimal amount

because of the student’s performance on proficiency ex-

on Line 13.

ams.

Line 15—Multiply Line 14 by 25% (.25). This is your tentative

•

The student was enrolled in 2012 in a program that leads

Kentucky allowable credit.

to a degree, certificate, or other recognized educational

credential.

Line 16—Enter the tentative tax from Form 740 or Form 740-

•

The student was taking at least one-half the normal full-

NP, page 1, Line 22.

time workload for his or her course of study for at least

Line 17—Enter the amount from page 2, Part V, Line 37. This

one academic period beginning in 2012.

is the allowable credit carryforward from prior year(s). If there

•

The Hope Credit was not claimed for that student’s ex-

is no carryforward, enter zero.

penses in more than one prior tax year.

Line 18—Subtract Line 17 from Line 16.

•

The student has not been convicted of a felony for pos-

Line 19—Enter the smaller of Line 18 or Line 15.

sessing or distributing a controlled substance.

Line 20—Add Lines 17 and 19. Enter here and on Form 740 or

Note: If a student does not meet all of the above qualifica-

Form 740-NP, Line 23. This is your allowable 2012 education

tions, you may be able to take the Lifetime Learning

credit.

Credit for part or all of the student’s qualified education

expenses.

Line 21—If Line 18 is smaller than Line 15, subtract Line 18

from Line 15. This is the amount of unused credit carryforward

Line 1, Columns A and B—Enter student’s name, Social Secu-

from 2012 to 2013. Maintain records for following years.

rity number and the name and address of qualified Kentucky

institution.

Part V, Credit Carryforward from Prior Years—The Kentucky

Line 1, Column C—Enter qualified expenses; do not enter more

Education Tuition Tax credit can be carried forward for up to

than $2,400 for each student.

5 years if unused during the preceding tax year(s). You must

Line 1, Column D—Enter the amount from Column C or $1,200,

have completed Form 8863-K for any prior year in which you

whichever is smaller.

are claiming a credit carryforward.

20

ADVERTISEMENT

0 votes

Related Articles

Related forms

Instructions For Form 740-np - Kentucky Income Tax Return Nonresident Or Part-year Resident - 2011

Financial

Instructions For Form 740-np - Kentucky Income Tax Return Nonresident Or Part-year Resident - 2011

Financial

Form 740-np - Kentucky Individual Incometax Return Nonresident Or Part-year Resident - 2012

Financial

Form 740-np - Kentucky Individual Incometax Return Nonresident Or Part-year Resident - 2012

Financial

Form 740-np - Kentucky Individual Incometax Return Nonresident Or Part-year Resident - 2013

Financial

Form 740-np - Kentucky Individual Incometax Return Nonresident Or Part-year Resident - 2013

Financial

Form Ar1000nr - Arkansas Individual Income Tax Return Nonresident And Part Year Resident - 2012

Financial

Form Ar1000nr - Arkansas Individual Income Tax Return Nonresident And Part Year Resident - 2012

Financial

Form 740-np - Kentucky Individual Income Tax Return Nonresident Or Part-year Resident - 2007

Financial

Form 740-np - Kentucky Individual Income Tax Return Nonresident Or Part-year Resident - 2007

Financial

Form 740-np - Kentucky Individual Income Tax Return Nonresident Or Part-year Resident - 2014

Financial

Form 740-np - Kentucky Individual Income Tax Return Nonresident Or Part-year Resident - 2014

Financial

Form 740-np - Kentucky Individual Income Tax Return Nonresident Or Part-year Resident - 2016

Financial

Form 740-np - Kentucky Individual Income Tax Return Nonresident Or Part-year Resident - 2016

Financial

Related Categories

Parent category: Financial