Form 740-Np - Kentucky Income Tax Return Nonresident Or Part-Year Resident - 2012 Page 46

ADVERTISEMENT

1

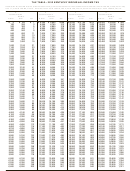

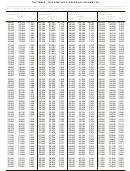

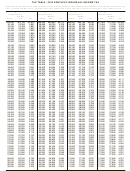

1 2

2 3

3 4

4 5

5 6

6 7

7 8

8 9

9 10

10 11

11 12

12 13

13 14

14 15

15 16

16 17

17 18

18 19

19 20

20 21

21 22

22 23

23 24

24 25

25 26

26 27

27 28

28 29

29 30

30 31

31 32

32 33

33 34

34 35

35 36

36 37

37 38

38 39

39 40

40 41

41 42

42 43

43 44

44 45

45 46

46 47

47 48

48 49

49 50

50 51

51 52

52 53

53 54

54 55

55 56

56 57

57 58

58 59

59 60

60for a clean coal facility. As provided by KRS 141.428, a clean

year if the credit cannot be taken in full in the year in which the

coal facility means an electric generation facility beginning

installation is completed.

commercial operation on or after January 1, 2005, at a cost

Line 19, Railroad Maintenance and Improvement Credit—The

greater than $150 million that is located in the Commonwealth

railroad maintenance and improvement credit provided by

of Kentucky and is certified by the Environmental and Pub-

KRS 141.385 is a nonrefundable credit that can be applied

lic Protection Cabinet as reducing emissions of pollutants

against the taxes imposed by KRS 141.020, KRS 141.040 and

released during generation of electricity through the use of

KRS 141.0401. The tax credit shall be used in the tax year of

clean coal equipment and technologies. The amount of the

the qualified expenditures which generated the tax credit and

credit shall be two dollars ($2) per ton of eligible coal pur-

cannot be carried forward to a return for any other period.

chased that is used to generate electric power at a certified

clean coal facility, except that no credit shall be allowed if the

An eligible taxpayer means the owner of a Class II or Class III

eligible coal has been used to generate a credit under KRS

railroad located in Kentucky, the transporter of property using

141.0405 for the taxpayer, parent or a subsidiary.

the rail facilities of a Class II or III railroad in Kentucky, or any

person that furnishes railroad-related property or services to

Line 16, Ethanol Tax Credit—An ethanol producer shall be

a Class II or Class III railroad located in Kentucky. A copy of

eligible for a nonrefundable tax credit against the taxes

Schedule RR-I must be attached to your return.

imposed by KRS 141.020 or 141.040 and 141.0401 in an amount

Line 20, Endow Kentucky Credit—Effective for taxable years

certified by the department. The credit rate shall be one dollar

($1) per ethanol gallon produced, unless the total amount of

beginning on or after Jan. 1, 2011, the Endow Kentucky Tax

approved credit for all ethanol producers exceeds the annual

Credit was created to encourage donations to community

ethanol tax credit cap. If the total amount of approved credit

foundations across the Commonwealth. KRS 141.438 was

for all ethanol producers exceeds the annual ethanol tax credit

created to allow a nonrefundable income tax and limited

cap, the department shall determine the amount of credit

liability entity tax credit of 20 percent of the value of the

each ethanol producer receives by multiplying the annual

endowment gift, not to exceed $10,000.

ethanol tax credit cap by a fraction, the numerator of which

A taxpayer shall attach a copy of the approved Schedule

is the amount of approved credit for the ethanol producer and

ENDOW to the tax return each year to claim the tax credit

the denominator of which is the total approved credit for all

against the taxes imposed by KRS 141.020 or 141.040 and

ethanol producers. The credit allowed shall be applied both

141.0401.

to the income tax imposed under KRS 141.020 or 141.040 and

to the limited liability entity tax imposed under KRS 141.0401,

A partner, member or shareholder of a pass–through entity

with the ordering of credits as provided in KRS 141.0205.

shall attach a copy of Schedule K–1, Form 720S; Schedule

Any remaining ethanol credit shall be disallowed and shall

K–1, Form 765; or Schedule K–1, Form 765–GP to the partner’s,

not be carried forward to the next year. “Ethanol producer”

member’s or shareholder’s tax return each year to claim the

is defined as an entity that uses corn, soybeans, or wheat to

tax credit.

manufacture ethanol at a location in this Commonwealth.

Unused credit may be carried forward for use in a subsequent

Line 17, Cellulosic Ethanol Tax Credit—A cellulosic ethanol

taxable year, for a period not to exceed five years.

producer shall be eligible for a nonrefundable tax credit against

Line 21, New Markets Development Tax Credit—A taxpayer

the taxes imposed by KRS 141.020 or 141.040 and 141.0401 in

that makes a qualified equity investment in a qualified

an amount certified by the department. The credit rate shall be

community development entity may be eligible for a credit that

one dollar ($1) per cellulosic ethanol gallon produced, unless

may be taken against the corporation income tax, individual

the total amount of approved credit for all cellulosic ethanol

income tax, insurance premiums taxes and limited liability

producers exceeds the annual cellulosic ethanol tax credit cap.

If the total amount of approved credit for all cellulosic ethanol

entity tax. The qualified community development entity must

producers exceeds the annual cellulosic ethanol tax credit

first submit an application to the Department of Revenue for

approval. The person or entity actually making the loan or

cap, the department shall determine the amount of credit each

making the equity investment will be able to claim a credit,

cellulosic ethanol producer receives by multiplying the annual

subject to a $5 million credit cap each fiscal year, by completing

cellulosic ethanol tax credit cap by a fraction, the numerator

Form 8874(K)-A.

of which is the amount of approved credit for the cellulosic

ethanol producer and the denominator of which is the total

approved credit for all cellulosic ethanol producers. The credit

allowed shall be applied both to the income tax imposed under

KRS 141.020 or 141.040 and to the limited liability entity tax

SECTION B—PERSONAL TAX CREDITS

imposed under KRS 141.0401, with the ordering of credits as

Line 1(a), Yourself—You are always allowed to claim a tax credit

provided in KRS 141.0205. Any remaining cellulosic ethanol

for yourself (even if your parent(s) can claim a credit for you

credit shall be disallowed and shall not be carried forward to

on their return). On Line 1(a), there are five boxes under three

the next year. “Cellulosic ethanol producer” is defined as an

separate headings. Always check the box under “Check Regu-

entity that uses cellulosic biomass materials to manufacture

lar” to claim a tax credit for yourself. If 65 or older, also check

cellulosic ethanol at a location in this Commonwealth.

the next two boxes on the line. If legally blind, also check the

last two boxes on the line.

Line 18, Energy Efficiency Products Tax Credits—This

nonrefundable credit is available to taxpayers who install

energy efficiency products for residential and commercial

Line 1(b), Your Spouse—Do not fill in Line 1(b) if (1) you are

single; (2) you are married and you and your spouse are filing

property located in the Commonwealth as provided by KRS

two separate returns; or (3) your spouse received more than

141.436 for taxable years beginning after December 31, 2008,

half of his or her support from another taxpayer.

and before January 1, 2016.

Fill in Line 1(b) if you are married and (1) you and your spouse

Complete Form 5695-K, Kentucky Energy Efficiency Products Tax

Credit, to see if you meet the qualifications for this credit.

are filing a joint or combined return, or (2) if your spouse had

no income or is not required to file a return. If you meet these

Individuals or businesses can apply the credit against their

criteria, check the first box on Line 1(b) for your spouse. If your

spouse is 65 or older, also check the next two boxes. If your

state income tax liability and carry the credit forward for one (1)

12

ADVERTISEMENT

0 votes

Related Articles

Related forms

Instructions For Form 740-np - Kentucky Income Tax Return Nonresident Or Part-year Resident - 2011

Financial

Instructions For Form 740-np - Kentucky Income Tax Return Nonresident Or Part-year Resident - 2011

Financial

Form 740-np - Kentucky Individual Incometax Return Nonresident Or Part-year Resident - 2012

Financial

Form 740-np - Kentucky Individual Incometax Return Nonresident Or Part-year Resident - 2012

Financial

Form 740-np - Kentucky Individual Incometax Return Nonresident Or Part-year Resident - 2013

Financial

Form 740-np - Kentucky Individual Incometax Return Nonresident Or Part-year Resident - 2013

Financial

Form Ar1000nr - Arkansas Individual Income Tax Return Nonresident And Part Year Resident - 2012

Financial

Form Ar1000nr - Arkansas Individual Income Tax Return Nonresident And Part Year Resident - 2012

Financial

Form 740-np - Kentucky Individual Income Tax Return Nonresident Or Part-year Resident - 2007

Financial

Form 740-np - Kentucky Individual Income Tax Return Nonresident Or Part-year Resident - 2007

Financial

Form 740-np - Kentucky Individual Income Tax Return Nonresident Or Part-year Resident - 2014

Financial

Form 740-np - Kentucky Individual Income Tax Return Nonresident Or Part-year Resident - 2014

Financial

Form 740-np - Kentucky Individual Income Tax Return Nonresident Or Part-year Resident - 2016

Financial

Form 740-np - Kentucky Individual Income Tax Return Nonresident Or Part-year Resident - 2016

Financial

Related Categories

Parent category: Financial