Form 740-Np - Kentucky Income Tax Return Nonresident Or Part-Year Resident - 2012 Page 5

ADVERTISEMENT

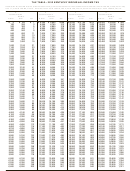

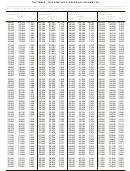

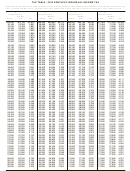

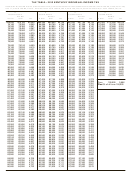

1

1 2

2 3

3 4

4 5

5 6

6 7

7 8

8 9

9 10

10 11

11 12

12 13

13 14

14 15

15 16

16 17

17 18

18 19

19 20

20 21

21 22

22 23

23 24

24 25

25 26

26 27

27 28

28 29

29 30

30 31

31 32

32 33

33 34

34 35

35 36

36 37

37 38

38 39

39 40

40 41

41 42

42 43

43 44

44 45

45 46

46 47

47 48

48 49

49 50

50 51

51 52

52 53

53 54

54 55

55 56

56 57

57 58

58 59

59 60

60YOUR RIGHTS AS A KENTUCKY TAXPAYER

•

As a Kentucky taxpayer, you have the right to expect the DOR

extension of time for filing reports or returns; and

to honor its mission and uphold your rights every time you

•

payment of charges incurred resulting from an erroneous

contact or are contacted by the DOR.

filing of a lien or levy by the DOR.

Guarantee—You have the right to a guarantee that DOR

RIGHTS OF TAXPAYER

employees are not paid, evaluated or promoted based on

taxes assessed or collected, or a tax assessment or collection

Privacy—You have the right to privacy of information provided

quota or goal imposed or suggested.

to the DOR.

Damages—You have the right to file a claim for actual and

Assistance—You have the right to advice and assistance from

direct monetary damages with the Kentucky Board of Claims

the DOR in complying with state tax laws.

if a DOR employee willfully, recklessly and intentionally

Explanation—You have the right to a clear and concise

disregards your rights as a Kentucky taxpayer.

explanation of:

Interest—You may have the right to receive interest on an

•

basis of assessment of additional taxes, interest and

overpayment of tax.

penalties, or the denial or reduction of any refund or credit

claim;

DEPARTMENT OF REVENUE RESPONSIBILITIES

•

procedure for protest and appeal of a determination of the

DOR; and

The DOR has the responsibility to:

•

tax laws and changes in tax laws so that you can comply

•

perform audits, conduct conferences and hearings with

with the law.

you at reasonable times and places;

•

Protest and Appeal—You have the right to protest and

authorize, require or conduct an investigation or surveillance

appeal a determination of the DOR if you disagree with an

of you only if it relates to a tax matter;

assessment of tax or penalty, reduction or a denial of a refund,

•

make a written request for payment of delinquent taxes

a revocation of a license or permit, or other determination

which are due and payable at least 30 days prior to seizure

made by the DOR.

and sale of your assets;

•

conduct educational and informational programs to help

Conference—You have the right to request a conference to

you understand and comply with the laws;

discuss the issue.

•

publish clear and simple statements to explain tax

Representation—You have the right to representation by your

procedures, remedies, your rights and obligations, and

authorized agent (attorney, accountant or other person) in any

the rights and obligations of the DOR;

hearing or conference with the DOR. You have the right to be

•

notify you in writing when an erroneous lien or levy is

informed of this right prior to the conference or hearing. If

released and, if requested, notify major credit reporting

you intend for your representative to attend the conference

companies in counties where lien was filed;

or hearing in your place, you may be required to give your

•

advise you of procedures, remedies and your rights and

representative a power of attorney before the DOR can discuss

obligations with an original notice of audit or when an

tax matters with your authorized agent.

original notice of tax due is issued, a refund or credit is

denied or reduced, or whenever a license or permit is

Recordings—You have the right to make an audio recording of

denied, revoked or canceled;

any meeting, conference, or hearing with the DOR. The DOR

•

has the right to make an audio recording, if you are notified

notify you in writing prior to termination or modification

in writing in advance or if you make a recording. You have

of a payment agreement;

the right to receive a copy of the recording.

•

furnish copies of the agent’s audit workpapers and a written

narrative explaining the reason(s) for the assessment;

Consideration—You have the right to consideration of:

•

resolve tax controversies on a fair and equitable basis at

•

waiver of penalties or collection fees if “reasonable cause”

the administrative level whenever possible; and

for reduction or waiver is given (“reasonable cause” is

•

notify you in writing at your last known address at least 60

defined in KRS 131.010(9) as: “an event, happening, or

days prior to publishing your name on a list of delinquent

circumstance entirely beyond the knowledge or control of

taxpayers for which a tax or judgment lien has been

a taxpayer who has exercised due care and prudence in

filed.

the filing of a return or report or the payment of monies

* * * * * * * * * * * * * *

due the department pursuant to law or administrative

regulation”);

This information merely summarizes your rights as a

•

installment payments of delinquent taxes, interest and

Kentucky taxpayer and the responsibilities of the Department

penalties;

of Revenue. The Kentucky Taxpayers’ Bill of Rights may be

•

waiver of interest and penalties, but not taxes, resulting

found in the Kentucky Revised Statutes (KRS) at Chapter

from incorrect written advice from the DOR if all facts were

131.041—131.081. Additional rights and responsibilities are

given and the law did not change or the courts did not issue

provided for in KRS 131.020, 131.110, 131.170, 131.183, 131.500,

a ruling to the contrary;

131.654, 133.120, 133.130, 134.580 and 134.590.

ADVERTISEMENT

0 votes

Related Articles

Related forms

Instructions For Form 740-np - Kentucky Income Tax Return Nonresident Or Part-year Resident - 2011

Financial

Instructions For Form 740-np - Kentucky Income Tax Return Nonresident Or Part-year Resident - 2011

Financial

Form 740-np - Kentucky Individual Incometax Return Nonresident Or Part-year Resident - 2012

Financial

Form 740-np - Kentucky Individual Incometax Return Nonresident Or Part-year Resident - 2012

Financial

Form 740-np - Kentucky Individual Incometax Return Nonresident Or Part-year Resident - 2013

Financial

Form 740-np - Kentucky Individual Incometax Return Nonresident Or Part-year Resident - 2013

Financial

Form Ar1000nr - Arkansas Individual Income Tax Return Nonresident And Part Year Resident - 2012

Financial

Form Ar1000nr - Arkansas Individual Income Tax Return Nonresident And Part Year Resident - 2012

Financial

Form 740-np - Kentucky Individual Income Tax Return Nonresident Or Part-year Resident - 2007

Financial

Form 740-np - Kentucky Individual Income Tax Return Nonresident Or Part-year Resident - 2007

Financial

Form 740-np - Kentucky Individual Income Tax Return Nonresident Or Part-year Resident - 2014

Financial

Form 740-np - Kentucky Individual Income Tax Return Nonresident Or Part-year Resident - 2014

Financial

Form 740-np - Kentucky Individual Income Tax Return Nonresident Or Part-year Resident - 2016

Financial

Form 740-np - Kentucky Individual Income Tax Return Nonresident Or Part-year Resident - 2016

Financial

Related Categories

Parent category: Financial