Form 740-Np - Kentucky Income Tax Return Nonresident Or Part-Year Resident - 2012 Page 47

ADVERTISEMENT

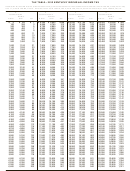

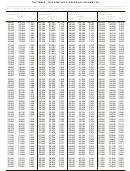

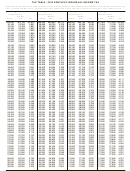

1

1 2

2 3

3 4

4 5

5 6

6 7

7 8

8 9

9 10

10 11

11 12

12 13

13 14

14 15

15 16

16 17

17 18

18 19

19 20

20 21

21 22

22 23

23 24

24 25

25 26

26 27

27 28

28 29

29 30

30 31

31 32

32 33

33 34

34 35

35 36

36 37

37 38

38 39

39 40

40 41

41 42

42 43

43 44

44 45

45 46

46 47

47 48

48 49

49 50

50 51

51 52

52 53

53 54

54 55

55 56

56 57

57 58

58 59

59 60

60spouse was legally blind at the end of the taxable year, also

INSTRUCTIONS FOR SCHEDULE A

check the last two boxes on Line 1(b).

FORM 740-NP

Dependents—You are allowed to claim a tax credit for each

person defined as a dependent in the Internal Revenue Code.

You may itemize your deductions for Kentucky even if you

Generally, dependents who qualify for federal purposes also

do not itemize for federal purposes. Amounts entered on

qualify for Kentucky.

Schedule A should be total deductions for the taxable period.

These amounts are prorated on Form 740-NP, page 1. If you

Line 2, Dependents Who Live With You

do not itemize, a standard deduction of $2,290 is allowed and

does not have to be prorated.

Use to claim tax credits for your dependent children, including

stepchildren and legally adopted children, who lived with you

Special Rules for Married Couples—If one spouse itemizes

during the taxable year. If the dependent meets the require-

deductions, the other must itemize. Married couples filing

ments for a qualifying child under the provisions of IRC 152(c),

a joint federal return and who wish to file separate returns

check the box; this child qualifies to be counted to determine

for Kentucky may: (a) file separate Schedules A showing the

the family size.

specific deductions claimed by each; (b) file a joint Schedule

A, divide the total deductions between them based on the

Dependents Who Did Not Live With You

percentage of each spouse's income to total income, and

attach a copy to each return; or (c) each spouse may claim

Also use Line 2 to claim tax credits for your dependent children

the standard deduction of $2,290.

who did not live with you and to claim tax credits for other

persons who qualify as dependents. These dependents do not

MEDICAL AND DENTAL EXPENSES

qualify to be counted to determine the family size.

Federal rules apply. You may deduct only your medical and

Children of Divorced or Separated Parents—Attach a copy of

dental expenses that exceed 7.5 percent of Form 740-NP, Line

federal Form 8332 filed with your federal return. Children may

8. Do not include any expenses deducted on Form 740-NP,

only be counted for family size by the custodial parent.

page 4, Section D, Column B, Line 31 or Line 32. Married

taxpayers filing separate Forms 740-NP who choose to file

Tax Credits for Individuals Supported by More Than One

one Schedule A and prorate the total must combine the Line

Taxpayer—Attach a copy of federal Form 2120 filed with your

8 amounts from both returns.

federal return.

TAXES

Kentucky National Guard Members—Persons who were mem-

bers of the Kentucky National Guard on December 31, 2012,

You may not deduct new motor vehicle taxes, sales tax, state

may claim an additional credit on Line 2. Designate this credit

or federal income taxes paid or withheld, otherwise federal

with the initials “N.G.” Kentucky law specifically restricts this

rules apply.

credit to Kentucky National Guard members; military reserve

members are not eligible.

INTEREST

You may deduct interest that you have paid during the taxable

year on a home mortgage. You may not deduct interest paid

on credit or charge card accounts, a life insurance loan, an

automobile or other consumer loan, delinquent taxes or on

SECTION C—FAMILY SIZE TAX CREDIT

a personal note held by a bank or individual.

Children may only be counted for family size by the custodial

parent. Even if you have signed federal Form 8332 and may

Interest paid on business debts should be deducted as

not claim the child as a dependent, you may count children

a business expense on the appropriate business income

who otherwise meet the requirements for the Family Size Tax

schedule.

Credit.

You may not deduct interest on an indebtedness of another

You must include in Section C the names and Social Security

person when you are not legally liable for payment of the

numbers of the qualifying children that are not claimed as

interest. Nor may you deduct interest paid on a gambling

dependents in Section B in order to count them in your total

debt or any other nonenforceable obligation. Interest paid

family size.

on money borrowed to buy tax-exempt securities or single

premium life insurance is not deductible.

Line 10—List the interest and points (including "seller-paid

points") paid on your home mortgage to financial institutions

and reported to you on federal Form 1098.

SIGN RETURN—Be sure to sign on page 3 after completion of

pages 1, 2, 3 and 4 of your return. Each return must be signed

Line 11—List other interest paid on your home mortgage and

by the taxpayer. Joint and combined returns must be signed

not reported to you on federal Form 1098. Show name and

by both husband and wife. Returns that are not signed may

address.

be returned to you for signature.

Line 12—List points (including "seller-paid points") not

Please enter a telephone number where you can be reached

reported to you on federal Form 1098. Points (including loan

during regular working hours. You may be contacted for

origination fees) charged only for the use of money and paid

additional information needed to complete processing of

with funds other than those obtained from the lender are

your tax return.

deductible over the life of the mortgage. However, points

may be deducted in the year paid if all three of the following

13

ADVERTISEMENT

0 votes

Related Articles

Related forms

Instructions For Form 740-np - Kentucky Income Tax Return Nonresident Or Part-year Resident - 2011

Financial

Instructions For Form 740-np - Kentucky Income Tax Return Nonresident Or Part-year Resident - 2011

Financial

Form 740-np - Kentucky Individual Incometax Return Nonresident Or Part-year Resident - 2012

Financial

Form 740-np - Kentucky Individual Incometax Return Nonresident Or Part-year Resident - 2012

Financial

Form 740-np - Kentucky Individual Incometax Return Nonresident Or Part-year Resident - 2013

Financial

Form 740-np - Kentucky Individual Incometax Return Nonresident Or Part-year Resident - 2013

Financial

Form Ar1000nr - Arkansas Individual Income Tax Return Nonresident And Part Year Resident - 2012

Financial

Form Ar1000nr - Arkansas Individual Income Tax Return Nonresident And Part Year Resident - 2012

Financial

Form 740-np - Kentucky Individual Income Tax Return Nonresident Or Part-year Resident - 2007

Financial

Form 740-np - Kentucky Individual Income Tax Return Nonresident Or Part-year Resident - 2007

Financial

Form 740-np - Kentucky Individual Income Tax Return Nonresident Or Part-year Resident - 2014

Financial

Form 740-np - Kentucky Individual Income Tax Return Nonresident Or Part-year Resident - 2014

Financial

Form 740-np - Kentucky Individual Income Tax Return Nonresident Or Part-year Resident - 2016

Financial

Form 740-np - Kentucky Individual Income Tax Return Nonresident Or Part-year Resident - 2016

Financial

Related Categories

Parent category: Financial