Form 706 - United States Estate (And Generation-Skipping Transfer) Tax Return Page 28

ADVERTISEMENT

Tax Return Printable pdf") 1

1 2

2 3

3 4

4 5

5 6

6 7

7 8

8 9

9 10

10 11

11 12

12 13

13 14

14 15

15 16

16 17

17 18

18 19

19 20

20 21

21 22

22 23

23 24

24 25

25 26

26 27

27 28

28 29

29 30

30 31

31 32

32 33

33 34

34 35

35 36

36 37

37 38

38 39

39 40

40 41

41Form 706 (Rev. 8-93)

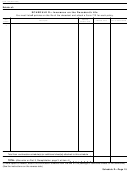

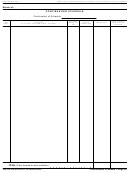

Examples of Listing of Property Interests on Schedule M

Item

Description of property interests passing to surviving spouse

Amount

number

1

One-half the value of a house and lot, 256 South West Street, held by decedent and surviving spouse as joint tenants

with right of survivorship under deed dated July 15, 1957 (Schedule E, Part I, item 1)

$ 32,500

2

Proceeds of Gibraltar Life Insurance Company policy No. 104729, payable in one sum to surviving spouse (Schedule

D, item 3)

20,000

3

Cash bequest under Paragraph Six of will

100,000

Instructions for Schedule

4. As a beneficiary of insurance on the

1. Another interest in the same

decedent’s life;

property passed from the decedent to

M.—Bequests, etc., to

some other person for less than

5. As the surviving spouse taking

Surviving Spouse (Marital

adequate and full consideration in

under dower or curtesy (or similar

Deduction)

money or money’s worth; and

statutory interest); and

2. By reason of its passing, the other

6. As a transferee of a transfer made

General

person or that person’s heirs may enjoy

by the decedent at any time.

You must complete Schedule M and file

part of the property after the termination

it with the return if you claim a

Property Interests That You May

of the surviving spouse’s interest.

deduction on item 18 of Part 5,

Not List on Schedule M

This rule applies even though the

Recapitulation.

interest that passes from the decedent

You should not list on Schedule M:

The marital deduction is authorized by

to a person other than the surviving

1. The value of any property that does

section 2056 for certain property

spouse is not included in the gross

not pass from the decedent to the

interests that pass from the decedent to

estate, and regardless of when the

surviving spouse.

the surviving spouse. You may claim the

interest passes. The rule also applies

2. Property interests that are not

deduction only for property interests that

regardless of whether the surviving

included in the decedent’s gross estate.

are included in the decedent’s gross

spouse’s interest and the other person’s

estate (Schedules A through I ).

3. The full value of a property interest

interest pass from the decedent at the

for which a deduction was claimed on

same time. Property interests that are

Note: The marital deduction is generally

Schedules J through L. The value of the

not allowed if the surviving spouse is not

considered to pass to a person other

property interest should be reduced by

a U.S. citizen. The marital deduction is

than the surviving spouse are any

the deductions claimed with respect to

property interest that: (a) passes under a

allowed for property passing to such a

it.

surviving spouse in a “qualified domestic

decedent’s will or intestacy; (b) was

transferred by a decedent during life; or

trust” or if such property is transferred or

4. The full value of a property interest

irrevocably assigned to such a trust

that passes to the surviving spouse

(c) is held by or passed on to any

before the estate tax return is filed. The

subject to a mortgage or other

person as a decedent’s joint tenant, as

appointee under a decedent’s exercise

executor must elect qualified domestic

encumbrance or an obligation of the

trust status on this return. See the

surviving spouse. Include on Schedule

of a power, as taker in default at a

instructions on pages 27, 29, and 30 for

decedent’s release or nonexercise of a

M only the net value of the interest after

power, or as a beneficiary of insurance

details on the election.

reducing it by the amount of the

mortgage or other debt.

in the decedent’s life.

Property Interests That You May

5. Nondeductible terminable interests

For example, a decedent devised real

List on Schedule M

property to his wife for life, with

(described below).

Generally, you may list on Schedule M

remainder to his children. The life

6. Any property interest disclaimed by

all property interests that pass from the

interest that passed to the wife does not

the surviving spouse.

decedent to the surviving spouse and

qualify for the marital deduction because

Terminable Interests

are included in the gross estate.

it will terminate at her death and the

However, you should not list any

children will thereafter possess or enjoy

Certain interests in property passing

“Nondeductible terminable interests”

the property.

from a decedent to a surviving spouse

(described below) on Schedule M unless

are referred to as terminable interests.

However, if the decedent purchased a

you are making a QTIP election. The

These are interests that will terminate or

joint and survivor annuity for himself and

property for which you make this

fail after the passage of time, or on the

his wife who survived him, the value of

election must be included on Schedule

occurrence or nonoccurrence of some

the survivor’s annuity, to the extent that

M. See “Qualified Terminable Interest

contingency. Examples are: life estates,

it is included in the gross estate,

Property” on the following page.

annuities, estates for terms of years,

qualifies for the marital deduction

For the rules on common disaster and

and patents.

because even though the interest will

survival for a limited period, see section

terminate on the wife’s death, no one

The ownership of a bond, note, or

2056(b)(3).

else will possess or enjoy any part of the

other contractual obligation, which when

property.

You may list on Schedule M only

discharged would not have the effect of

those interests that the surviving spouse

The marital deduction is not allowed

an annuity for life or for a term, is not

takes:

considered a terminable interest.

for an interest that the decedent

directed the executor or a trustee to

1. As the decedent’s legatee, devisee,

Nondeductible terminable interests.—

convert, after death, into a terminable

heir, or donee;

A terminable interest is nondeductible,

interest for the surviving spouse. The

and should not be entered on Schedule

2. As the decedent’s surviving tenant

marital deduction is not allowed for such

M (unless you are making a QTIP

by the entirety or joint tenant;

an interest even if there was no interest

election) if:

3. As an appointee under the

decedent’s exercise of a power or as a

taker in default at the decedent’s

nonexercise of a power;

Page 28

ADVERTISEMENT

0 votes

Related Articles

Related forms

Tax Return")

Tax Return")

Tax Return")

Tax Return")

Tax Return")

Tax Return")

Tax Return - 2011") Instructions For Form 706 - United States Estate (and Generation-skipping Transfer) Tax Return - 2011

Financial

Instructions For Form 706 - United States Estate (and Generation-skipping Transfer) Tax Return - 2011

Financial

Tax Return - 2008") Instructions For Form 706 - United States Estate (and Generation-skipping Transfer) Tax Return - 2008

Financial

Instructions For Form 706 - United States Estate (and Generation-skipping Transfer) Tax Return - 2008

Financial

Tax Return - 2005")

Tax Return")

Related Categories

Parent category: Financial