Form 706 - United States Estate (And Generation-Skipping Transfer) Tax Return Page 37

ADVERTISEMENT

Tax Return Printable pdf") 1

1 2

2 3

3 4

4 5

5 6

6 7

7 8

8 9

9 10

10 11

11 12

12 13

13 14

14 15

15 16

16 17

17 18

18 19

19 20

20 21

21 22

22 23

23 24

24 25

25 26

26 27

27 28

28 29

29 30

30 31

31 32

32 33

33 34

34 35

35 36

36 37

37 38

38 39

39 40

40 41

41Form 706 (Rev. 8-93)

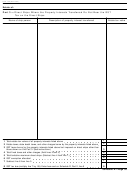

When To Pay the GST Tax

Instructions for Fiduciary

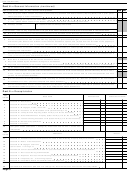

The GST tax is due and payable 9 months after the

Purpose of Schedule R-1

decedent’s date of death (entered by the executor on

Code section 2603(a)(2) provides that the Generation-

Schedule R-1). Interest will be charged on any GST

Skipping Transfer (GST) tax imposed on a direct skip

taxes unpaid as of that date. However, you have an

from a trust is to be paid by the trustee. Schedule R-1

automatic extension of time to file Schedule R-1 and

(Form 706) serves as a payment voucher for the

pay the GST tax due until 2 months after the due date

trustee to remit the GST tax to the IRS. See the

(with extensions) for filing the decedent’s Schedule R,

instructions for Form 706 as to when a direct skip is

Form 706. This Schedule R, Form 706 due date is

from a trust.

entered by the executor on Schedule R-1. Thus, while

interest will be due on unpaid GST taxes, no penalties

How To Pay the GST Tax

will be charged if you file Schedule R-1 by this

The executor will compute the GST tax, complete

extended due date.

Schedule R-1, and give you two copies. You should

Signature

pay the GST tax using one copy and keep the other

copy for your records.

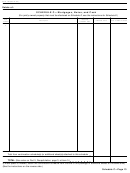

You, as fiduciary, must sign the Schedule R-1 in the

space provided.

The GST tax due is the amount shown on line 6.

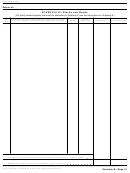

Make your check or money order for this amount

payable to “Internal Revenue Service,” write “GST tax”

and the trust’s EIN on it, and send it and one copy of

the completed Schedule R-1 to the IRS Service Center

where the Form 706 was filed, as shown on the front

of the Schedule R-1.

Schedule R-1 (Form 706)—Page 37

ADVERTISEMENT

0 votes

Related Articles

Related forms

Tax Return")

Tax Return")

Tax Return")

Tax Return")

Tax Return")

Tax Return")

Tax Return - 2011") Instructions For Form 706 - United States Estate (and Generation-skipping Transfer) Tax Return - 2011

Financial

Instructions For Form 706 - United States Estate (and Generation-skipping Transfer) Tax Return - 2011

Financial

Tax Return - 2008") Instructions For Form 706 - United States Estate (and Generation-skipping Transfer) Tax Return - 2008

Financial

Instructions For Form 706 - United States Estate (and Generation-skipping Transfer) Tax Return - 2008

Financial

Tax Return - 2005")

Tax Return")

Related Categories

Parent category: Financial