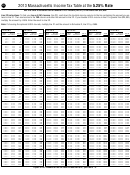

Instructions For Form 1 - Massachusetts Resident Income Tax - 2013 Page 18

ADVERTISEMENT

1

1 2

2 3

3 4

4 5

5 6

6 7

7 8

8 9

9 10

10 11

11 12

12 13

13 14

14 15

15 16

16 17

17 18

18 19

19 20

20 21

21 22

22 23

23 24

24 25

25 26

26 27

27 28

28 29

29 30

30 31

31 32

32 33

33 34

34 35

35 36

36 37

37 38

38 39

39 40

40 41

41 42

42 43

43 44

446

2013 Form 1 — Before You Begin

tax jurisdiction solely to be with the servicemem-

excess unused exemptions against interest in-

Form 1-ES. See line 38 instructions and TIR 04-25

come (other than interest from Massachusetts

for more information.

ber in compliance with the servicemember’s mili-

tary orders. In general, for Massachusetts tax

banks), dividends or capital gain income; and

purposes, the new law will affect only service-

When to File

a senior circuit breaker tax credit which allows

members and their spouses who are domiciled in

senior citizens meeting certain eligibility criteria

a state other than Massachusetts. For more infor-

Your Return

to claim a refundable credit on their state income

mation see TIR 09-23.

taxes for the real estate taxes paid on the Mass-

Your 2013 Massachusetts Form 1 is due on or be-

The following example illustrates circumstances

achusetts residential property they own or rent, and

fore April 15, 2014.

under which military pay is or is not taxable in

which they occupy as their principal residence. The

Massachusetts. No guidance is intended on the

credit is the amount by which the real estate tax

Automatic Extension Granted if

tax treatment of such pay under the laws of other

payment or 25% of the rent constituting real es-

100% of the Tax Due is Paid by

states. Generally, when income is taxable in two

tate tax payments exceeds 10% of their total in-

jurisdictions, a credit for taxes paid to the other

come, but not more than $1,030. The credit is

the Tax Return Due Date

jurisdiction is allowed on the taxpayer’s return in

refundable to the extent the credit exceeds the

If line 3 of the following Form 1 Extension Work-

the state of his/her residence.

taxpayer’s tax liability.

sheet is “0” and 100% of the tax due for 2013 has

been paid through:

Example: Betsy enlisted in the Navy in Massachu-

How Do I File a Decedent’s Return?

setts, but moved with her husband, Eric, from

withholding;

A final income tax return must be filed for a tax-

Massachusetts to Delaware when she was sta-

payer who died during the taxable year. This re-

timely estimated payments of tax;

tioned there. They did not change their domicile to

turn should include income received until date of

credits from your 2013 return; and

Delaware. She received military income while her

death. It must be signed and filed by his/her ex-

husband received income working as a reporter for

an overpayment from the prior tax year applied

ecutor, administrator or surviving spouse for the

a local newspaper.

to the next year’s estimated tax,

portion of the year before the taxpayer’s death. Be

Betsy’s income from the Navy, as well as her hus-

sure to fill in oval 1 if the taxpayer who was listed

you are no longer required to file Form M-4868,

band’s income from the newspaper, are both sub-

first on last year’s income tax return is deceased,

Application for Automatic Extension of Time to File

ject to Massachusetts income tax since she

or oval 2 if the taxpayer who was listed second on

Massachusetts Income Tax Return. However, if you

enlisted in the Navy in Massachusetts and they

last year’s income tax return is deceased. Also,

do choose to file Form M-4868 in this instance,

did not become legal residents of Delaware. Betsy

enclose Form M-1310, Statement of Claimant to

you must do so electronically, via DOR’s website.

and her husband are, therefore, Massachusetts

Refund Due on Behalf of Deceased Taxpayer, with

See TIR 06-21 for more information.

residents, and any income they receive, whether

the refund claimant’s name and Social Security

Also, if you owe no tax or you are making a pay-

derived in Massachusetts or not, is included in

number clearly printed.

ment of $5,000 or more, you are required to file

their Massachusetts gross income.

A joint return may be filed by a surviving spouse.

your extension electronically, either through E-File

In the case of the death of both spouses, a final re-

or via the web. Failure to do so will result in a

What Are the Rules for Filing

turn must be filed by their legal representative.

penalty. If you are making a payment of less than

a Joint Return?

$5,000, you also have the option of filing your ex-

Any income of $100 or more received for the dece-

A joint Form 1 is not allowed if both spouses were

tension electronically. If there is a tax due with your

dent for the taxable year after the decedent’s death,

not Massachusetts residents for the same portion

extension, payment can be made through Elec-

and for succeeding taxable years until the estate

of 2013.

tronic Funds Withdrawal.

is completed, must be reported each year on

If your spouse died during 2013, you may still

Massachusetts Form 2, Massachusetts Fiduciary

Visit www. mass. gov/dor to file via the Web.

choose to file a joint return.

Income Tax Return. Form 2 is available online at

If you are legally married, you have the option of

Form 1 Extension Worksheet

filing either a joint return or a married filing sepa-

If the decedent’s return shows a refund due, and if

1. Enter amount from Form 1, line 31

rate return. Married taxpayers who file a joint re-

2. Enter the total of Form 1, lines 36

the Probate Court has not appointed a legal repre-

turn are allowed to claim the following exemptions,

through 38 and 40 through 42 . . . . . .

sentative and none is contemplated, a Massachu-

deductions and credits which married taxpayers

3. Amount due. Subtract line 2 from

setts Form M-1310 must be enclosed with the

filing separate returns may not claim:

line 1, not less than “0” . . . . . . . . . . .

return so the refund check may be made payable

a deduction of $3,600 ($7,200 for two or more

to the proper person.

Note: Your extension will not be valid if you fail to

dependents) for a dependent member of house-

pay 80% of your total tax liability through with-

Should I Make Estimated Tax

hold under age 12, or dependent age 65 or over as

holding, estimated tax payments or with your ex-

Payments in 2014?

of December 31, 2013 (not you or your spouse)

tension. Form M-4868 is available at

or a disabled dependent;

Every resident or nonresident who expects to pay

gov/ dor or by calling (617) 887-MDOR or toll-free

more than $400 in Massachusetts income tax on

No Tax Status if joint Massachusetts AGI was

in Massachusetts 1-800-392-6089.

in come which is not covered by Massachusetts

$16,400 or less plus $1,000 for each dependent;

with holding must pay Massachusetts estimated

Must I File on a Calendar Year Basis?

Limited Income Credit if joint Massachusetts

taxes. Estimated tax payments can be made on-

No. You may file on a fiscal year basis if you keep

AGI is between $16,400 and $28,700 plus $1,750

line by using WebFile for Income by visiting

your books and records on that fiscal year basis

for each dependent;

gov/dor or by filing Massachusetts

and if you receive permission from the Commis-

ADVERTISEMENT

0 votes

Related Articles

Related forms

Related Categories

Parent category: Financial