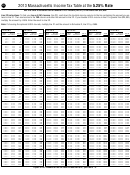

Instructions For Form 1 - Massachusetts Resident Income Tax - 2013 Page 40

ADVERTISEMENT

1

1 2

2 3

3 4

4 5

5 6

6 7

7 8

8 9

9 10

10 11

11 12

12 13

13 14

14 15

15 16

16 17

17 18

18 19

19 20

20 21

21 22

22 23

23 24

24 25

25 26

26 27

27 28

28 29

29 30

30 31

31 32

32 33

33 34

34 35

35 36

36 37

37 38

38 39

39 40

40 41

41 42

42 43

43 44

4428

2013 Form 1 — Schedule Instructions

home on business. However, you may fully deduct

less you answered “no” to the question on mater-

No credit is allowed if the taxpayer claims the

ial participation on the front of Schedule C. In this

“married filing separate” status, receives a federal

meals and entertainment furnished or reim bursed

to an employee if you properly treat the ex pense

case, your loss is further limited. Use the amounts

or state rent subsidy, rents from a tax-exempt en-

as wages subject to withholding. You may also

calculated on your pro forma U.S. Form 6198 to

tity, or is the dependent of another taxpayer.

fully deduct meals and entertainment provided to

complete a pro forma U.S. Form 8582. If your at-

Is the Tax Credit Considered Income?

a nonemployee to the extent the expenses are in-

risk amount is “0” or less, enter “0” in line 31.

Tax credits received by eligible taxpayers are not

cludible in the gross income of that person and re-

considered income for the purpose of obtaining

ported on Form 1099-MISC. Figure how much of

Senior Circuit

eligibility or benefits under other means-tested as-

the amount on line 23a is subject to the 50% limit.

sistance programs including food, medical, hous-

Then, enter 50% of that amount on line 23b. This

Breaker Tax Credit

ing, energy and educational assistance programs.

amount should be subtracted from the amount in

line 23a. Enter the result in line 23 of Massachu-

How Does a Taxpayer Claim

What Is It?

setts Schedule C.

the Credit?

For tax years beginning on or after January 1,

Line 30. Abandoned Building

2001, senior citizens in Massachusetts may be el-

Taxpayers who are eligible for the tax credit in the

Renovation Deduction

igible to claim a refundable credit on their state

2013 tax year can claim the credit by submitting a

income taxes for the real estate taxes they paid on

completed Schedule CB, Circuit Breaker Credit,

Massachusetts allows businesses to deduct 10%

the Massachusetts residential property they own

with their 2013 state income tax return. Eligible

of the costs incurred in renovating certain build-

or rent and which they occupy as their principal

taxpayers who do not normally file a state income

ings located in an Economic Opportunity Area

residence. The maximum credit allowed is $1,030

tax return may obtain a refund by filing a return

(EOA). The buildings must be designated as aban-

for the tax year beginning January 1, 2013. See

with Schedule CB. As with all claimed tax credits

doned by the Economic Assistance Coordinating

TIR 13-16 for more information.

and deductions, the taxpayer must keep all perti-

Council. The renovation deduction may be taken

nent records, receipts and other documentation

in addition to any other deduction for which the

Eligible taxpayers who own their property may

supporting his or her claim for the credit.

renovation costs may qualify. For more informa-

claim a credit equal to the amount by which their

tion, contact the Massachusetts Office of Business

property tax payments in tax year 2013 (exclud-

Line 1. Living Quarters Status

Development.

ing any exemptions and/or abatements), includ-

During 2013

ing water and sewer debt charges, exceed 10% of

In line 30 enter 10% of the costs of renovating a

Be sure to fill in the appropriate oval. If you were a

their “total income” for the same current tax year.

qualifying abandoned building.

renter in 2013 and you received any federal and/or

Taxpayers residing in communities that do not in-

state subsidy, or you rent from a tax-exempt entity,

Line 32. Interest (other than from

clude water and sewer debt service in their prop-

you do not qualify for the Circuit Breaker Credit.

erty tax assessments may claim, in addition to

Massachusetts banks) and Dividend

their property tax payments, 50% of the water

Homeowners, fill in the appropriate “Yes” or “No”

Income

and sewer use charges actually paid during the

oval to indicate if you owned a multi-use or multi-

If you have interest (other than from Massachu-

tax year when figuring their credit.

family property. A taxpayer who owns a principal

setts banks) and dividend income reported on

residence with a land area in excess of one acre or

Renters may claim a credit in the amount by which

U.S. Schedule C, lines 1 and/or 6 or Schedule

a multi-use building or land area, for example, a

25% of their annual rental payment is more than

C-EZ, line 1, enter that amount in line 32 and in

storefront with an apartment up above, may only

10% of their total income.

Massachusetts Schedule B, line 3. If you are not

claim the taxpayer's proportional share of the real

required to file Schedule B (see Schedule B in-

For purposes of the tax credit, a taxpayer’s “total

estate tax payments (Schedule CB, line 10), in-

structions), enter that amount on Form 1, line 20.

income” includes taxable income as well as ex-

cluding water and sewer use charges (Schedule

Do not include such amounts on Massachusetts

empt income such as Social Security, Treasury

CB, line 13), which corresponds to the portion of

Schedule C, lines 1 and/or 4.

bills and public pensions. For a complete list of

the residence used and occupied as principal res-

what constitutes “total income,” see TIR 01-19.

Line 33. If You Have a Loss

idence. A taxpayer who owns a multiple family

dwelling (a multi-family residence that includes

Fill in the oval in line 33a if all of your investment

Who Is Eligible for the Credit?

the taxpayer's personal residence), may only

is at risk. Enter your loss from line 31 on Form 1,

To be eligible for the credit for the 2013 tax year, a

claim the taxpayer's proportional share of the

line 6 unless you answered “no” to the question

taxpayer must be 65 years of age or older before

taxes (Schedule CB, line 10) or sewer and water

on material participation on the front of Schedule

January 1, 2014 (for joint filers, it is sufficient if

use charges (Schedule CB, line13) paid. For ex-

C. If you answered “no” to this question, complete

one taxpayer is 65 years of age or older), must

ample, where a condominium association pays

a pro forma copy of U.S. Form 8582 that reflects

own or rent residential property in Massachusetts

one sewer and water bill for multiple owners, each

only income being reported on your Massachusetts

and occupy the property as his or her principal res-

owner may only claim the proportional share of

return. Enter in Massachusetts Schedule C, line 31

idence, and must not be the dependent of another

the use charges attributable to the taxpayer's

your allowable loss calculated on Form 8582.

taxpayer. The taxpayer’s total income cannot ex-

condominium (for example, the condominium

ceed $55,000 for a single filer who is not the head

Fill in the oval in line 33b if only some of your in-

owner's percentage interest in the undivided in-

of a household, $69,000 for a head of household,

vestment is at risk. To determine the amount of

terest of common areas and facilities).

or $82,000 for taxpayers filing jointly. No credit is

your allowable loss, complete a pro forma copy of

allowed for a married taxpayer unless a joint re-

U.S. Form 6198 that reflects only income being

turn is filed. Moreover, the assessed valuation of

reported on your Massachusetts return. Enter the

the real estate cannot exceed $700,000.

amount calculated on U.S. Form 6198 in line 31 un-

ADVERTISEMENT

0 votes

Related Articles

Related forms

Related Categories

Parent category: Financial