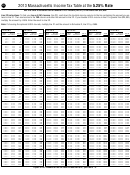

Instructions For Form 1 - Massachusetts Resident Income Tax - 2013 Page 32

ADVERTISEMENT

1

1 2

2 3

3 4

4 5

5 6

6 7

7 8

8 9

9 10

10 11

11 12

12 13

13 14

14 15

15 16

16 17

17 18

18 19

19 20

20 21

21 22

22 23

23 24

24 25

25 26

26 27

27 28

28 29

29 30

30 31

31 32

32 33

33 34

34 35

35 36

36 37

37 38

38 39

39 40

40 41

41 42

42 43

43 44

4420

2013 Form 1 — Schedule Instructions

separate worksheets must be completed to calcu-

Schedule Z

The EACC may also, in consultation with the DOR,

limit (but not expand) the credit to a specific dollar

late the deduction. See TIR 06-14 for additional

information.

amount or time duration or in any other manner

Other Credits

deemed appropriate by the EACC, St. 2009, c. 166,

The deduction is allowed where an individual pur-

Be sure to enclose with Form 1.

§18. For example, the EACC may limit the credit

chases an MBTA pass for a dependent who is

available with respect to a particular project to a

claimed on that individual’s tax return, provided

Part 1 Credits

specific dollar maximum, even if the actual dollar

the dependent does not also claim the deduction.

Line 1. Lead Paint

amount of the qualifying purchases would other-

However, the total amount deducted cannot ex-

wise generate a higher credit amount. Similarly,

If you incurred expenses for covering or remov-

ceed $750 for each individual taxpayer who is fil-

the EACC may limit the otherwise applicable credit

ing lead paint on residential premises in Mass-

ing a return. In the case of married taxpayers filing

carry forward period provided by G.L. c. 62, sec.

achusetts, you may claim a credit for expenses up

a joint return, the total amount deducted cannot

6(g) and G.L. c. 63, sec. 38N (d). See TIRs 10-15

to $1,500 for each residential unit. The basic rules

exceed $750 per taxpayer; thus, the maximum

and 10-1 for more information. If you qualify for

are explained on Massachusetts Sched ule LP,

deduction for a joint return is $1,500.

the credit, fill in the appropriate oval, complete

Credit for Removing or Covering Lead Paint on

Complete the Schedule Y, Line 15 Worksheet to

Schedule EDIP and enter the amount of the credit

Residential Premises. If you qualify for the credit,

calculate the commuter deduction.

in line 2. Also, be sure to enter the EACC-issued

complete Schedule LP and enter the amount of

certificate number in line 2. Note: You must enter

credit in line 1. Be sure to enter in line 1a the total

Schedule Y, Line 15 Worksheet.

the certificate number on Schedule Z. Failure to do

number of units indicated in Schedule LP, line(s)

Commuter Deduction

so will result in this credit being disallowed on your

1a and 3a.

1. Enter amount paid in 2013 for tolls

tax return and an adjustment of your reported tax.

Note: You must enclose Schedule LP with your

through an E-ZPass account . . . . . .

Enter the number from left to right.

return. Failure to do so will result in this credit

2. Enter amount paid in 2013 for weekly or

being disallowed on your tax return and an adjust-

Line 3. Septic

monthly transit commuter passes for MBTA

ment of your reported tax.

transit or commuter rail. (Do not include

An owner of residential property located in Mass-

amounts reimbursed or otherwise

achusetts who occupies the property as his or her

Line 2. Economic Opportunity Area/

deductible). . . . . . . . . . . . . . . . . . . .

principal residence is allowed a credit of a maxi-

Economic Development Incentive

3. Add lines 1 and 2. If $150 or less, you do not

mum of $1,500 per taxable year for expenses in-

qualify for this deduction. Omit remainder of

Program

curred to comply with the sewer system require-

this worksheet. Otherwise, complete

Massachusetts allows a credit equal to 5% of the

ments of Title V as promulgated by the Department

lines 4 through 6 . . . . . . . . . . . . . . .

cost of qualifying property purchased for business

of Environmental Protection or to connect to a mu -

4. Enter $150. . . . . . . . . . . . . . . . . .

use within an Economic Opportunity Area (EOA).

nicipal sewer system pursuant to a federal court

5. Subtract line 4 from line 3. . . . . .

If you qualify for the credit, fill in the appropriate

order, administrative consent order, state court

6. Enter the lesser of line 5 or $750

oval, complete Schedule EOAC and enter the

order, consent decree or similar mandate. The

here and on Schedule Y, line 15 . . .

amount of credit in line 2. Note: You must enclose

amount of the credit is 40% of the cost, up to

Schedule EOAC with your return. Failure to do so

$15,000, for design and construction expenses for

Line 16. Deduction for Expenses of

will result in this credit being disallowed on your

repair or replacement of a failed cesspool or sep-

Human Organ Transplant

tax return and an adjust ment of your reported tax.

tic system. The maximum aggregate amount of

An individual may deduct certain expenses and

the credit is $6,000. A five-year carryover of any

The Economic Development Incentive Program

other costs incurred in the process of donating an

unused credit is allowed. See TIRs 97-12, 98-8,

Credit (EDIPC) is a tax credit under G.L. c. 62, sec.

organ for a human organ transplant to another in-

99-5, 99-20 and DOR Directive 01-6 for more in-

6(g) and G.L. c. 63, sec. 38N equal to a percent-

dividual. For purposes of this deduction, “human

formation. If you qualify for this credit, complete

age of the cost of property purchased for business

organ” shall mean all or part of human bone mar-

Massachusetts Schedule SC, Septic Credit, and

use within a certified project as defined in G.L. c.

row, liver, pancreas, kidney, intestine or lung. In

enter the amount of credit in line 3. Note: You

23A, sec. 3A.

the case of an individual who donates an organ to

must enclose Schedule SC with your return. Failure

To be eligible for the EDIP credit, the project must

another person for human organ transplantation,

to do so will result in this credit being disallowed

have certified on or after January 1, 2010. As part

the individual may deduct the following expenses

on your tax return and an adjustment of your re-

of the project certification, the Economic Assist-

that are incurred by the individual and related to

ported tax.

ance Coordinating Council (EACC) may (but is not

the individual’s organ donation: (i) travel expenses;

Note: Betterment assessments do not qualify for

required to) award a credit under the program and,

(ii) lodging expenses; and (iii) lost wages not to

this credit.

when a credit is awarded, the EACC will determine

exceed $10,000. An individual who is a nonresi-

the percentage of the cost of property to be used

dent of Massachusetts for all or part of the taxable

Line 4. Brownfields

in determining the credit.

year is not eligible to claim this deduction. If you are

Recent legislation extends the Brownfields credit

entitled to claim this deduction, enter the amount

Taxpayers with ongoing projects that were certi-

to nonprofit organizations, extends the time frame

claimed in Schedule Y, line 16. See TIR 11-6 for

fied prior to January 1, 2010 may be eligible for

for eligibility for the credit, and permits the credit to

further information.

credits under the prior version of the Economic De -

be transferred, sold, or assigned. Under prior law,

velopment Incentive Program; such taxpayers do

net response and removal costs incurred by a tax-

not file schedule EDIP (see TIR 10-01 and Sched-

payer between August 1, 1998 and August 5,

ule EOAC).

2005, were eligible for the credit provided that the

en vironmental response action before August 5,

ADVERTISEMENT

0 votes

Related Articles

Related forms

Related Categories

Parent category: Financial