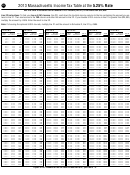

Instructions For Form 1 - Massachusetts Resident Income Tax - 2013 Page 38

ADVERTISEMENT

1

1 2

2 3

3 4

4 5

5 6

6 7

7 8

8 9

9 10

10 11

11 12

12 13

13 14

14 15

15 16

16 17

17 18

18 19

19 20

20 21

21 22

22 23

23 24

24 25

25 26

26 27

27 28

28 29

29 30

30 31

31 32

32 33

33 34

34 35

35 36

36 37

37 38

38 39

39 40

40 41

41 42

42 43

43 44

4426

2013 Form 1 — Schedule Instructions

If you did file a U.S. Schedule D, enter the capital

Line 12. Long-Term Gains on

If Schedule D, line 15 is a loss and Schedule B,

gain distributions reported to you by a mutual fund

line 24 is “0” or greater and Schedule B, line 31 is

Collectibles and Pre-1996

or real estate investment trust included in U.S.

a positive amount, go to Schedule D, line 16.

Installment Sales

Schedule D, line 13, column h.

If Schedule D, line 15 is a loss, and Schedule B, line

Enter in line 12 the amount of long-term gains on

21 is “0” or less, omit Schedule D, line 16, enter the

collectibles and pre-1996 installment sales classi-

Line 7. Massachusetts Long-Term

amount from Schedule D, line 15 in Schedule D, line

fied as capital gain income for Massachusetts

Capital Gains and Losses Included

17, omit Schedule D, lines 18 through 22 and enter

purposes that are included in line 11.

in U.S. Form 4797, Part II

the amount from Schedule D, line 17 in Schedule

Long-term gains on collectibles and pre-1996 in-

Enter amounts included in U.S. Form 4797, Part II

D, line 23, and enter “0” on Form 1, line 24.

stallment sales classified as capital gain income

treated as capital gains or losses for Massachu-

for Massachusetts purposes are taxed at the 12%

Line 16. Long-Term Capital Losses

setts purposes (not included in lines 1 through 6).

rate and should be entered on Schedule B, line 11.

Applied Against Interest and

These include ordinary gains from the sale of Sec-

tion 1231 property, recapture amounts under Sec-

Collectibles are defined as any capital asset that is

Dividends

tions 1245, 1250 and 1255, Section 1244 losses

a collectible within the meaning of Internal Rev-

If Schedule D, line 15 is a loss, and Schedule B,

and the loss on the sale, exchange or involuntary

enue Code section 408(m), as amended and in

line 24 is “0” or greater and Schedule B, line 31 is

conversion of property used in a trade or business.

effect for the taxable year, including works of art,

a positive amount, complete the Long-Term Capi-

rugs, antiques, metals, gems, stamps, alcoholic

tal Losses Applied Against Interest and Dividends

Line 8. Carryover Losses from

beverages, certain coins, and any other items

Worksheet for Schedule B, Line 32 and Schedule

Previous Years

treated as collectibles for federal tax purposes.

D, Line 16.

If you have a carryover loss from a prior year, enter

Line 13. Subtotal

in line 8 the total amount of carryover losses from

Line 17. Subtotal

Subtract line 12 from line 11 and enter the result

your 2012 Massachusetts Schedule D, line 23.

Combine line 15 and line 16. If Schedule D, line 17

in line 13.

is “0,” enter “0” in lines 18 through 21 and omit

Line 10. Differences

lines 22 and 23. If Schedule D, line 17 is a loss,

If Schedule D, line 13 is a loss and Schedule B,

Enter any differences between the gains or losses

omit lines 18 through 22 and enter the amount

line 21 is less than “0,” omit Schedule D, lines 14

reportable for Massachusetts tax purposes and the

through 16, enter the amount from Schedule D,

from line 17 in line 23.

U.S. gains or losses reported in Massachusetts

line 13 in Schedule D, line 17, omit Schedule D,

Schedule D, lines 1 through 8. Differences include:

Line 18. Allowable Deductions

lines 18 through 22 and enter the amount from

From Your Trade or Business

Schedule D, line 17 in Schedule D, line 23, and

Pre-1996 installment sales classified as ordi-

enter “0” on Form 1, line 24.

nary income for Massachusetts purposes;

Enter the appropriate amount from Massachu-

setts Schedule C-2 if you qualify for an excess

If Schedule D, line 13 is a gain and Schedule B,

Long-term capital gains or losses from transac-

trade or business deduction. Generally, taxpayers

line 21 is a loss, go to Schedule D, line 14.

tions reported as installment sales for U.S. income

may not use excess 5.25% deductions to offset

tax purposes but not for Massachusetts; and

If Schedule D, line 13 is a loss and Schedule B,

other income. However, where the taxpayer files a

line 24 is “0” or greater, go to Schedule D, line 14.

Massachusetts has adopted basis adjustment

Massachusetts Schedule C or Schedule E, Mass-

rules to take into account differences between

If Schedule D, line 13 is a gain, and Schedule B,

achusetts law allows such offsets if the following

Massachusetts and federal tax laws.

requirements are met: the excess 5.25% deduc-

line 24 is “0” or greater, omit Schedule D, lines 14

tions must be adjusted gross income deductions

through 16 and enter the amount from Schedule

Line 11. Adjusted Capital Gains and

D, line 13 in Schedule D, line 17.

allowed under MGL Ch. 62, sec. 2(d); and these

Losses

excess deductions may only be used to offset

Line 14. Capital Losses Applied

Exclude/subtract line 10 from line 9 and enter the

other income which is effectively connected with

result in line 11.

Against Capital Gains

the active conduct of a trade or business or any

other income allowed under IRC, sec. 469(d)(1)(B)

If Schedule D, line 13 is a positive amount and

If line 10 is a loss, add loss as a positive number

to offset losses from passive activities.

Schedule B, line 22 is a loss, enter the smaller of

to the amount recorded in line 9. See the follow-

Schedule D, line 13 or Schedule B, line 21 (con-

ing examples:

Line 20. Excess Exemptions

sidered as a positive amount) in Schedule D, line

Schedule D

Enter in line 20 the amount from line 8 of the

14 and in Schedule B, line 22.

Line

ex. A

ex. B

ex. C

ex. D

Schedule B, Line 36 and Schedule D, Line 20

If Schedule D, line 13 is a loss and Schedule B, line

19

$1,000 $1,000 *$0,700**$700*

Worksheet (only if single, head of household or

24 is a positive amount, enter the smaller of Sched-

110

$1,500 *$1,300* $0,500 *$500*

married filing joint return).

ule D, line 13 (considered as a positive amount) or

11

$1,500 $1,300 *$1,200**$200*

Schedule B, line 24 in Schedule D, line 14 and in

Line 22. Tax On Long-Term Capital

*denotes loss

Schedule B, line 25.

Gains

If in line 10 you entered amounts which in-

Multiply line 21 by .0525 and enter the result here

Line 15. Subtotal

crease the amounts reported from U.S. to Mass-

and in Form 1, line 24.

If line 13 is greater than “0,” subtract line 14 from

achusetts, for example, a long-term gain reported

line 13. If line 13 is less than “0,” combine lines 13

Note: If choosing the optional 5.85% tax rate,

as install ment sales for U.S. tax purposes but not

and 14.

multiply line 21 by .0585 and enter the result here

for Massachusetts, add the amount in line 10 to

and in Form 1, line 24.

the amount in line 9.

ADVERTISEMENT

0 votes

Related Articles

Related forms

Related Categories

Parent category: Financial