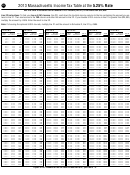

Instructions For Form 1 - Massachusetts Resident Income Tax - 2013 Page 39

ADVERTISEMENT

1

1 2

2 3

3 4

4 5

5 6

6 7

7 8

8 9

9 10

10 11

11 12

12 13

13 14

14 15

15 16

16 17

17 18

18 19

19 20

20 21

21 22

22 23

23 24

24 25

25 26

26 27

27 28

28 29

29 30

30 31

31 32

32 33

33 34

34 35

35 36

36 37

37 38

38 39

39 40

40 41

41 42

42 43

43 44

4427

2013 Form 1 — Schedule Instructions

Line 23. Available Losses for

Accounting Method

certain agent or commission drivers and traveling

salespersons and certain homeworkers. If you had

Carryover

If you filed a return on the accrual basis last year,

both self-employment income and statutory em-

your return for this year must be on the same basis.

Enter the amount from Schedule D, line 17, only if

ployee income, do not combine these amounts

If a taxpayer requesting permission to change an

it is a loss.

on a single Sched ule C. In this case, you must file

accounting method for Massachusetts purposes is

separate Schedule Cs.

eligible for an automatic change of accounting

Schedule C

method federally, and has correctly followed the

Line 4. Other Income

most recently issued federal revenue procedure for

Note: If showing a loss, be sure to mark over the

If you received bartering income, you must report

requesting an automatic change, then the taxpayer

“X” in the box to the left. Also, be sure to enclose

the fair market value of goods or services received

should file his/her annual return using the new

with Form 1.

in payment for your goods and services in line 4. Do

method and write at the top, “Automatic Change

not include interest income (other than from Mass -

Substituting U.S. Schedules C

of Accounting Method — filed in compliance with

achusetts banks) and dividends here (see line 32).

DOR Directive 02-13.” The taxpayer should en-

or C-EZ

close a copy of federal Form 3115, together with

U.S. Schedules C or C-EZ are no longer allowed

Line 7. Bad Debts From Sales or

any required statements. See DOR Directive 02-13

as a substitute for Massachusetts Schedule C.

Services

for further information.

Include debts and partial debts from sales or serv-

Profit or Loss from Business or

Material Participation

ices that were included in income and are definitely

Profession

known to be worthless. If you later collect a debt

Indicate if you materially participated in the oper-

Massachusetts Schedule C is provided to report in -

that you deducted as a bad debt, include it as in-

ation of this business during 2013. If you did not

come and deductions from each business or pro -

come in the year collected.

materially participate and have a loss from this

fession operated as a sole proprietorship.

business, see line 33 for further instructions.

Note: Cash method taxpayers cannot take a bad

If your business deductions, excluding the Aban-

debt deduction unless the amount was previously

Line 1a. Gross Receipts or Sales

doned Building Renovation Deduction, exceed

included in income.

In the boxes provided, enter gross receipts or sales

Schedule C income and any other income taxable

from your business. Be sure to include on this line

at the 5.25% rate, such excess deductions may be

Line 11. Depreciation and

amounts you received in your trade or business

subtracted from the other income that is effec-

Section 179 Deduction

as shown on Form 1099-MISC, Miscellaneous In-

tively connected with the active conduct of your

Massachusetts adopts the current federal rules at

come. If the nature of your business is such that

trade or business and any other income allowed

section 179 for expensing certain depreciable

you have gross or other income that is interest

under IRC Section 469(d)(1)(B) to offset losses

business assets. For property placed in service in

(other than from Massachusetts banks) and divi-

from passive activities. To compute the excess

tax years beginning on or after January 1, 2012,

trade or business deductions use Massachusetts

dend income, exclude this income from lines 1 and

the maximum section 179 expensing allowance

4 on Massachusetts Schedule C and include it in

Schedule C-2. This form is available by visiting

is $500,000.

line 32 and in Schedule B, line 3. Note: If not

, or you may have one mailed

required to file Schedule B (see Schedule B in-

to you by calling (617) 887-MDOR.

Line 17. Pension and Profit-Sharing

structions), enter this income on Form 1, line 20.

Plans

Registration Information

Examples of interest (other than from Massa -

Enter your deduction for contributions to a pen-

In the space provided, describe the business or pro-

chusetts banks) and dividend income are interest

sion, profit-sharing or annuity plan, or plans for the

fessional activity that provided your principal source

received on loans, notes receivable or charge ac-

benefit of your employees. If the plan includes you

of income reported on line 1. If you owned more

counts that you accept in the ordinary course of

as a self-employed person, do not include contri-

than one business, you must complete a separate

business, and dividends on stocks received in

butions made as an employer on your behalf. See

Schedule C for each business. Give the general field

payment for goods and services. Capital gains

DOR Directive 08-3 for more information.

or activity and the type of product or service.

from the sale or exchange of assets used in your

business are not reported on Schedule C. Use U.S.

Line 23. Meals and Entertainment

Employer Identification Number

Form 4797 and report the amount in Form 1,

Line 23a. Enter your total business meal and en-

You need an Employer Identification number (EIN)

Schedule B and/or Schedule D. You must also ex-

tertainment expenses. Include meals while travel-

only if you had a Keogh plan, were required to file

clude from Schedule C any income and expenses

ing away from home for business. Instead of the

an employment, excise, estate, trust, or alcohol, to-

that pertain to activities for yourself as distin-

actual cost of your meals while traveling away from

bacco and firearms tax return or employ contract

guished from those performed for your cus-

home, you may use the standard meal allowance.

labor. If you do not have an EIN, leave the line

tomers. Such income must be reported by class of

Business meal expenses are deductible only if they

blank. Do not enter your Social Security number.

income in Schedules B and D. Personal expenses

are (a) directly related to or associated with the

are not deductible.

conduct of your trade or business, (b) not lavish or

Small Business Energy Exemption

If you received Form W-2 and the “Statutory em-

extravagant and (c) incurred while you or your em -

If you are claiming the small business energy ex-

ployee” box in item 13 of that form was checked,

ployee is present at the meal. Club dues are not

emption from the sales tax on purchases of tax-

report your income and expenses related to that

allowed as a business deduction.

able energy or heating fuel during 2013, you must

income on Schedule C. Enter your statutory em-

have five or fewer employees. You must enter the

Line 23b. Generally, you may deduct only 50% of

ployee income from box 1 of Form W-2 on line 1

number of your employees in the space provided.

your business meal and entertainment expenses,

of Schedule C and fill in the oval. Statutory em-

including meals incurred while traveling away from

ployees include full-time life insurance agents,

ADVERTISEMENT

0 votes

Related Articles

Related forms

Related Categories

Parent category: Financial