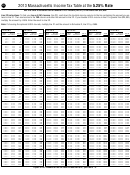

Instructions For Form 1 - Massachusetts Resident Income Tax - 2013 Page 20

ADVERTISEMENT

1

1 2

2 3

3 4

4 5

5 6

6 7

7 8

8 9

9 10

10 11

11 12

12 13

13 14

14 15

15 16

16 17

17 18

18 19

19 20

20 21

21 22

22 23

23 24

24 25

25 26

26 27

27 28

28 29

29 30

30 31

31 32

32 33

33 34

34 35

35 36

36 37

37 38

38 39

39 40

40 41

41 42

42 43

43 44

448

2013 Form 1 — Line by Line Instructions

failure to disclose was attributable to reasonable

Custodial Parent

of the Code. For purposes of sec. 151(c), the def-

inition of dependent in sec. 152 is adopted. Under

cause and not willful neglect.

Fill in the Custodial parent who has released claim

federal law, there are additional restrictions on the

to exemption for child(ren) oval if you are claiming

Note: Lines without specific instructions are con-

dependent exemption beyond the rules of sec.

the head of household filing status and you have

sidered to be self-explanatory.

152 that are not adopted by Massachusetts. For

released your claim to one or more dependent ex-

Massachusetts tax purposes, if an individual qual-

Line 1. Filing Status

emptions on IRS Form 8332, or participated in a

ifies as a dependent under the rules of sec. 152,

decree or agreement to allow the noncustodial

Note: More than one filing status may apply to you.

you can claim a dependent exemption for such a

parent to claim a dependency exemption.

If so, you may wish to figure your taxes based

person. If you claim such a dependent in Mass-

upon more than one filing status to see which sta-

Whole Dollar Method Required

achusetts, increase the number reported in item b

tus is to your benefit.

The Department of Revenue requires that the

from your U.S. return by the number of such ad-

Single

whole dollar method be used for entries made on

ditional dependents.

Fill in the “Single” oval if you were single as of

forms or schedules. For example, amounts be-

Line 2c: Age 65 or Over Before 2014

December 31, 2013. This status applies to you if

tween $1.00 and $1.49 should be entered as $1.00

You are allowed an additional $700 exemption if

at the close of the taxable year you fit into any of

and amounts between $1.50 and $2.00 should be

you were age 65 or over before January 1, 2014.

the following categories:

entered as $2.00. However, calculations on work-

If your spouse was age 65 or over and you are fil-

sheets used to reach amounts shown on the re-

you were unmarried;

ing a joint return, you may also claim a $700 ex-

turn may be made in one of two ways: (1) round

you were a widow or widower whose spouse

emption for your spouse. Fill in the appropriate

amounts before adding them up and enter the re-

died before 2013; or

oval(s) and enter the total number of persons age

sulting total on the form, or (2) add amounts to

65 or over in the small box. Multiply that total by

you were legally separated under a final judg-

the penny, and then round to the whole dollar for

$700 and enter the total in line 2c.

ment of the probate court.

entry on the form. Either method is acceptable as

long as one method is used consistently through-

Line 2d: Blindness Exemption

Please note that you are not single if: (1) you have

out the return.

You are allowed an additional $2,200 exemption if

obtained a judgment of divorce which has not yet

you are legally blind. If your spouse is also legally

become final; (2) you have a temporary support

Line 2. Exemptions

blind and you are filing a joint return, you may also

order; or (3) you and your spouse simply choose

Line 2a: Personal Exemptions

claim a $2,200 exemption for your spouse. Fill in

to live apart.

Each taxpayer is entitled to claim a personal ex-

the appropriate oval(s) and enter the total number

Married Filing Joint Return

emption. The amount of your personal exemption

of blindness exemptions in the small box. Multiply

Fill in the “Married filing joint return” oval if you

depends on your filing status in line 1.

that total by $2,200 and enter the total in line 2d.

were legally married as of December 31, 2013.

If you are single or married filing a separate re-

Legal Definition of Blindness

Both spouses are responsible for the accuracy of

turn, enter $4,400 in line 2a.

You are legally blind and qualify for the blindness

all information entered on a joint return and both

exemption if your visual acuity with correction is

If filing as head of household, enter $6,800 in

must sign. A joint return is allowed even if only one

20/200 or less in the better eye, or if your peripheral

line 2a.

spouse had income or if one spouse died during

field of vision has been contracted to a 10-degree

2013. For further information, refer to the section

If married filing a joint return, enter $8,800 in

radius or less, regardless of visual acuity.

“What Are the Rules for Filing a Joint Return?”

line 2a.

Line 2e: Other: Medical/Dental Expenses

Married Filing Separate Return

Line 2b: Number of Dependents

and Adoption Agency Fee

Fill in the “Married filing separate return” oval if

You may claim a $1,000 exemption for each of

You may claim an exemption for medical and den-

you were legally married as of December 31, 2013,

your dependents if you claimed them on your U.S.

tal expenses paid during 2013 only if you itemized

and if you and your spouse are not filing a joint

return. Enter in the box in item b the number of

these expenses on your U.S. Form 1040, Sched-

return. Be sure to enter your spouse’s Social Se-

dependents you listed on U.S. Form 1040, line 6c

ule A. If you are married filing a joint U.S. Form

curity number in the space provided.

or U.S. Form 1040A, line 6c. Do not include your-

1040, you must file a joint Massachusetts Form 1

self or your spouse. Then, multiply that total by

Head of Household

to claim this exemption. Enter in line 2e, item 1 the

$1,000 and enter the total amount in line 2b. Be

Fill in the “Head of household” oval if you qualify

amount reported on your U.S. Form 1040, Sched -

sure to fill out Schedule DI, Dependent Informa-

to file this status federally. This status is for un-

ule A, line 4.

tion, if you are claiming a dependent exemp-

married people who paid over half the cost of

tion(s). Failure to do so will delay the processing

If you paid adoption fees to a licensed adoption

keeping up a home for a qualifying person, such

of your return.

agency during 2013, you are eligible for an ex-

as a child who lived with you or your dependent

emption of the total amount of the fees paid dur-

parent. Be sure to include such qualifying person

Note: Only one person (or married couple filing

ing the year. Fees paid during 2013 to an agency

on Schedule DI, Dependent Information. Certain

jointly) may claim the dependent exemption for

licensed to place children for adoption on account

married people who lived apart from their spouse

any one child or other dependent.

of the adoption process of a minor child regard-

for the last six months of 2013 and who meet all of

In a few cases, the number of dependents claimed

less of whether an adoption actually took place

the other federal requirements may also be able to

for Massachusetts purposes and for U.S. pur-

during 2013 should also be included for this ex-

use this status. See IRS Publication 501, Exemp-

poses may differ. Massachusetts allows a depen-

emption. Enter this amount in line 2e, item 2.

tions, Standard Deduction, and Fil ing Information,

dent exemption for each individual who qualifies

for more information.

Add items 1 and 2 and enter the total in line 2e.

for exemption as a dependent under sec. 151(c)

ADVERTISEMENT

0 votes

Related Articles

Related forms

Related Categories

Parent category: Financial