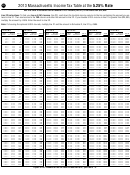

Instructions For Form 1 - Massachusetts Resident Income Tax - 2013 Page 31

ADVERTISEMENT

1

1 2

2 3

3 4

4 5

5 6

6 7

7 8

8 9

9 10

10 11

11 12

12 13

13 14

14 15

15 16

16 17

17 18

18 19

19 20

20 21

21 22

22 23

23 24

24 25

25 26

26 27

27 28

28 29

29 30

30 31

31 32

32 33

33 34

34 35

35 36

36 37

37 38

38 39

39 40

40 41

41 42

42 43

43 44

4419

2013 Form 1 — Schedule Instructions

U.S. Form 1040, line 36. Identify jury duty pay

Line 14. Claim of Right Deduction

Schedule Y, Line 11 Worksheet. College

given to your employer as “Jury pay”; reforesta-

Taxpayers who have paid Massachusetts personal

Tuition Deduction

tion amortization as “RFST”; repayment of supple -

income taxes in a prior year on income attributed

1. Enter total tuition payments paid by you, for

mental unemployment benefits under the Trade

to them under a “claim of right” may deduct the

yourself or a dependent, to a qualify-

Act of 1974 as “Sub-Pay TRA”; attorney fees and

amount of that income from their gross income if it

ing two- or four-year college in 2013

court costs involving certain unlawful discrimina-

later develops that they were not in fact entitled to

2. Enter amount of scholarships, grants or

tion claims as “UDC”; and deductible expenses re-

the income, and have repaid the amounts in ques-

financial aid received in 2013 for

lated to income reported on U.S. Form 1040, line

tion. The deduction is allowed in the year of repay -

amounts shown in line 1 . . . . . . . . .

21 and Massachusetts Schedule X, line 4 from the

ment, provided that the repayment is not otherwise

3. Enter amount of reimbursements or refunds

rental of personal property engaged in for profit

deductible in determining Massachusetts income

received in 2013 of amounts shown in line 1

as “PPR.” Fill in the appropriate oval in line 9 of

taxable under M.G.L. ch. 62. Some examples in

reported by an insurer (from US Form

Schedule Y.

which the claim of right may be applied for are:

8383, box 10) . . . . . . . . . . . . . . . . .

Business Expenses of National Guard and

4. Subtract lines 2 and 3 from line 1. If “0”

Stock under claim of ownership. Gains from

Reserve Members, Performing Artists and Fee-

or less, you do not qualify for this

sales of stock under a claim of ownership must be

deduction. . . . . . . . . . . . . . . . . . . . .

Based Government Officials: Enter the amount

included, regardless of whether the taxpayer actu-

5. Enter amount from line 7 of the

from U.S. Form 1040, line 24 and fill in the appro-

ally owned it;

Massachusetts AGI Worksheet . . . .

priate oval in line 9 of Schedule Y.

Employment contracts. Amounts in settlement

6. Multiply line 5 by .25. . . . . . . . . .

of employment contracts must be included not -

Line 10. Student Loan Interest

7. If line 4 is smaller than line 6, you are not

with standing the prospect of eventual repayment

eligible for this deduction. Enter “0.” If line 4

Deduction

to the employer of an amount equivalent to or

is larger than line 6, subtract line 6 from line 4

Enter the amount from U.S. Form 1040, line 33 or

greater than the amount received;

and enter the result here and on

1040A, line 18, not to exceed $2,500. This deduc-

Schedule Y, line 11 . . . . . . . . . . . . .

Dividends. Where a taxpayer receives a dividend

tion is only allowed if not claiming the same ex-

that must be repaid in a later year (e.g., because it

penses in line 12 of Schedule Y, Undergraduate

Line 12. Undergraduate Student

impaired corporate capital), the dividend must be

Student Loan Interest Deduction.

Loan Interest Deduction

included in the year of receipt;

Line 11. College Tuition Deduction

A deduction is allowed for interest paid on a qual-

Corporate notes. Where a taxpayer receives a

A deduction is allowed for tuition payments paid

ified undergraduate student loan. To be eligible for

distribution with respect to holding of notes, the

by you, for yourself or a dependent, to a qualifying

the deduction, the “education debt” must be a loan

income must be included regardless of whether it

two- or four-year college leading to an undergrad-

that is administered by the financial aid office of a

could be challenged by senior creditors;

uate or associate’s degree, diploma or certificate.

two-year or four-year college at which you, or a

Mistake in validity of claim. The claim of right

Tuition payments for students pursuing graduate

qualified dependent, were enrolled as an under-

doctrine applies where a taxpayer merely mistakes

degrees at such a college or university are not eli-

graduate student. Additionally, the loan must have

the validity of his claim; or

gible for the college tuition deduction. The deduc-

been secured through a state student loan pro-

tion is equal to the amount by which the tuition

gram, a federal student loan program, or a com-

Advanced insurance commissions.

payments, less any scholarships, grants or finan-

mercial lender, and must have been spent solely

If you are entitled to claim this deduction, enter the

cial aid received, exceed 25% of Massachusetts

for the purposes of paying tuition and other ex-

amount claimed in Schedule Y, line 14. For more

AGI. The amount of the college tuition deduction

penses directly related to the school enrollment.

information, see TIR 06-4.

is limited to qualified tuition expenses paid during

Enter the amount of such interest paid in Sched-

a taxable year in connection with an academic

ule Y, line 12. This deduction is only allowed if not

Line 15. Commuter Deduction

term beginning during such taxable year or dur-

claiming the same expenses in line 10 of Sched-

A deduction is allowed for certain amounts paid by

ing the first three months of the next taxable year.

ule Y, Student Loan Interest Deduction.

an individual for tolls paid for through an E-ZPass

account or for weekly or monthly transit com-

Qualified tuition expenses include only those ex-

Line 13. Deductible Amount of

muter passes for MBTA transit, bus, commuter rail

penses designated as tuition or mandatory fees

Qualified Contributory Pension

or commuter boat, not including amounts reim-

required for the enrollment or attendance of the tax-

Income from Another State or

bursed or otherwise deductible.

payer or any dependent of the taxpayer at an eligi-

Political Subdivision Included in

ble educational institution. No deduction is allowed

In the case of a single person or a married person

for any amount paid for room and board, books,

Form 1, Line 4

filing a separate return or a head of household, this

supplies, equipment, personal living expenses,

Massachusetts allows a deduction for contribu-

deduction applies only to the portion of such ex-

meals, lodging, travel or research, athletic fees, in-

tory pension income received from another state

pended amount that exceeds $150, and the total

surance expenses or other expenses unrelated to

or one of its political subdivisions which does not

amount deducted cannot exceed $750. In the case

an individual’s academic course of instruction.

tax such income from Massachusetts or its politi-

of a married couple filing a joint return, this deduc-

Also, no deduction is allowed for reimbursements

cal subdivi sions. For guidelines to determine which

tion applies only to the portion of such amount ex -

or refunds of qualified tuition and related ex-

state’s pen sions are exempt in Massachusetts, see

pended by each individual that exceeds $150, and

penses made by an insurer. Complete the Mass-

TIR 95-9. Enter any deductible amount of such in-

the total amount deducted cannot exceed $750 for

achusetts AGI Worksheet and the Schedule Y, line

come in line 13 of Schedule Y that was included in

each individual. Also, one spouse cannot transfer

11 worksheet to see if you may qualify for this

Form 1, line 4.

his or her excess deduction to the other spouse;

deduction. See TIR 97-13 for more information.

ADVERTISEMENT

0 votes

Related Articles

Related forms

Related Categories

Parent category: Financial